Export Credit Agency (ECA)

A private or semi-legislative institution that acts as an intermediary between national governments and exporters

What Is an Export Credit Agency (ECA)?

An export credit agency is a private or semi-legislative institution that acts as an intermediary between national governments and exporters to provide export insurance solutions and guarantees subsidies and funding. It is also known as an investment insurance agency.

It offers loans, trade finance, and other different administrations to domestic companies and international exports. The main aim of ECAs is to provide support to the domestic economy and employment by assisting companies with tracking down abroad business sectors for their products.

ECAs were previously a bank after all other options had run out, stepping in only when private-sector financing was inaccessible but ECAs have taken on a noteworthy job since the global financial crisis, providing essential help as increasingly risk-wary private lenders pulled back from export finance.

Presently, there are scores of national ECAs around the world, collectively assisting hundreds of billions of dollars a year towards industries' efforts to sell goods and services abroad.

ECAs are progressively critical to national industrial strategies. They can arrange government-upheld loans, assurances, and protection in some of the world’s riskiest and most unpredictable markets.

In the majority of cases, development projects like major infrastructure might never get built without their assistance.

After commercial banks withdrew, followed by the global financial crisis, ECAs became lending players in international project financing and exports.

- ECAs facilitate international trade, offering insurance, subsidies, and funding post the global financial crisis.

- Originating to support local businesses, ECAs now collaborate internationally, involving banks in their operations.

- ECAs ensure low-risk lending, vital for global project financing, providing loans, trade finance, and insurance services.

- ECAs offer market expansion and increased sales but come with added costs, risks, and complex rules.

Origin of Export Credit Agency

Export credit agencies initially came to function through the government attempting to support local companies and rise their product/service export business.

Their particular services were proposed to limit the risk of participating in international markets and reduce the barriers to entry for domestic businesses.

Export credit agencies typically assist businesses and banks within their own nation. Nevertheless, it is now becoming common for ECAs to collaborate with international organizations or subsidiary organizations on the other side of trade agreements.

Banks can also become an integral factor during such deals. For example, a bank assisting a domestic company’s export and an export credit agency supporting the worldwide association on the receiving end.

Understanding export credit agency

ECAs play a major role in world trade. The export credit ensures that they provide a low risk of private lending. Hence, ECAs are becoming leading players in international project financing and exports.

ECAs like Exim Bank assist with filling the subsidizing gap that private-area lenders make with their failure or reluctance to provide financial support. They assist all goods and services with contending on a worldwide scale.

ECAs charge expenses when they offer financial services. Interest from clients at times can be an option in contrast to the premium, or the ECA could accuse it of being related to the premium.

Most ECAs offer protection like insurance, as well as different administrations, for both medium terms, somewhere in the range of two to five years-and long terms, which are five to 10 years.

ECA support of worldwide trade is an increasingly important aspect in individual transactions and for projects being attempted in developing countries or non-industrial nations.

The accessibility of the financing that ECAs give is essential to project fruition and the full acknowledgment of the subsequent commodities in these nations. As per EXIM, one of its essential jobs is "making everything fair".

Right when U.S exporters face new competition upheld by various councils'. To do as such, it will "match or counter the funding by around 85 ECAs all around the planet".

Importance of Export Credit Agency

As previously stated, governments often create or support export trade agencies because of their beneficial effects on the economy.

- Creating an export plan can boost business sales and overall growth for small and large firms.

- It can also associate them with possibly undiscovered specialty markets without the need to move tasks abroad.

- The advances most frequently increment the supporting or protection needs for organizations, where commodity credit offices become effective.

- They offer administrations that different banks have decided not to supply for hazard and instability purposes. Their specialization in abroad business sectors is additionally an engaging perspective to most organizations hoping to get into global exchange.

- ECAs are also considered responsible by the World Trade Organization (WTO) orders and guidelines. The guidelines were executed intently after ECAs' fast development towards turning into a key part of the worldwide exchange.

Benefits and Drawbacks of ECA

There are so many benefits of ECA that not only help exporters grow their international sales but also enable them to better manage their business. Some of the benefits are:

- Expand into new markets: Realizing that a foreign consumer defaults, your business will be compensated up to 95% of your foreign invoice.

- Boost sales with existing clients: Many exporters have existing clients that would buy more with an extension of credit terms or an increment in the credit line provided.

- Unlock more attractive financing: Banks are hesitant to lend money against export-associated assets; with credit insurance, your bank will more desirably lend against foreign receivables.

- Transfer the burden of credit management: It helps by easing the burden of credit risk management and allows you to focus on what you do best.

- Confidence to explore new markets: It is more than a backstop to protect your business from the risk of unpaid invoices.

Some of the drawbacks or limitations of export credit agencies are explained below:

- It adds more cost to doing business as banks charge fees for providing services.

- ECAs also carry the risk with them.

- Commercial things have complex rules and policies.

- It can be misused.

Exports credits group

The OECD (Officially Supported Export Credits) provides a forum for transferring the data on members' export credit systems for various business activities/deals and for discussing and coordinating national export credit regulations.

These strategies are connected with great administration issues, the expected social level of effort, and manageable lending. These conversations happen under the sponsorship of the functioning party on sending out credits and credit ensures (the "Export Credits Group" or ECG).

All OECD individuals are ECG individuals, aside from Chile, Costa Rica, and Iceland. The OECD has a long custom of rule production in the space of formally upheld trade credits.

The pattern of OECD: The OECD is likewise a gathering for keeping up with, creating, and observing the monetary disciplines for sending out credits, which are held inside the plan of authoritatively upheld trade credits.

These disciplines specify the most liberal monetary agreements that individuals might offer while giving authoritatively upheld trade credits.

The subsequent product credits disciplines apply above all else to OECD individuals; notwithstanding, a few key non-individuals routinely notice gatherings of the ECG and the members.

Industry-wise involvement of Export Credit Agency

For the most part, three techniques are used by export credit agencies to disburse money to an importing firm. They include Direct Lending, Financial Intermediary loans, and Interest Rate equalization.

- Direct lending: the simplest structure where the loan is conditioned on the purchase of goods or services from businesses in the organizing nation.

- Financial intermediary loans or advances: the EXIM bank provides funds to a financial intermediary, like a commercial bank, which in turn provides the funds to the importing entity.

- Interest rate equalization: here, a commercial lender offers a loan to the importing entity with low-market interest rates, which in turn receives compensation from the EXIM bank for the difference between the low-market rate and the commercial rate.

Export Credit Agencies usually limit financing from nations that are deemed to be unsafe in terms of creditworthiness in an attempt to control the risk efficiently.

Additionally, committees of government or administrative officials and the export credit agency officials will review the large and more complex financing endeavors as these transactions are prone to a significant amount of risk related to normal transactions.

Authoritatively supported export credit is directly connected to official development assistance (ODA), which makes the agency subject to the policies set by the Organization of Economic Cooperation and Development (OECD).

Contribution of ECA to different industries

Most export credit agencies are structured to provide finance for the medium, i.e., more than 2 to 5 years to a long term of more than 5 to 10 years. However, some can specialize in the short term, like less than 2 years.

It is important to take note that credit, insurance, and assurance risks are quite often under the obligation of the supporting borrower.

The contribution of ECAs to different industry sectors is explained below:

- Construction industry: The involvement of ECA in this sector is major, as it contributes 45.5% to the construction industry.

- Wholesale trade: ECA, in total, contributes 17.7% to the wholesale trading industries.

- Shipbuilding: Similar to the wholesale trade industry, ECA contributes 17.7% to the shipbuilding industry.

- Professional services: To this sector, it contributes 9.6%, which is in quite the minority as compared to others.

- Mining industry: A total of 7.9% is contributed to the mining industry, and this is a minor contribution compared to others.

- Other industries: Apart from the above-mentioned, ECA contributes a total of 8.3% to the other sectors.

The financing process of the Export Credit Agency

ECA finance is frequently viewed as difficult, regulatory, and tedious.

Most large projects require finance from various ECAs, and subsequently, project sponsors frequently need to manage applications, negotiations, and communications with different ECAs, having their own processes and necessities.

A variety of cooperation agreements have been placed into different ECAs, which consider the coordination of activities in different areas between specific ECAs.

Furthermore, the ECAs are invariably working alongside commercial banks and other potential lenders. The administration of this cycle can be requested and requires cautious preparation and an intensive comprehension of the ECA prerequisites preceding beginning to engage.

Export credit agencies use the different forms of financing made accessible to them by their governments to motivate exports of goods and services and also to achieve their mission by providing political or business risk and a mixture of insurance and lending activities.

These can also offer financial support by means of interest rates and equalization to commercial banks by offering direct loans or subsidized interest rates.

Financing the deal

ECAs empower exporters to be competitive in worldwide procurement processes or to participate in projects in which the component of risk would somehow not be reasonable or sustainable. ECA also ensures equity investments against political risks.

1. Financing Activity: This method is mainly utilized by countries such as the United States, Canada, and Japan, and loans are provided at a fixed subsidized interest rate.

The agency lends funds to a financial intermediary, which, in turn, lends to the SPV importer at a low fixed interest rate. This method is used by the Italian (ISACE), French (COFACE), and British (ECGD) ECAs.

The whole financing activity of ECA is governed by a document signed by OECD members and is known as the OECD consensus. The main objective of this document is to ensure an orderly export credit market, avoiding competitive wars between countries.

2. Insurance Activity: Although all ECAs adopt the common policies dictated by the OECD Consensus, their activities may differ from various standpoints.

Insurance activity includes risk coverage during the construction phase, business & political risk, direct agreements with most governments, level of insurance premiums payable by insured parties, and environmental risk coverage.

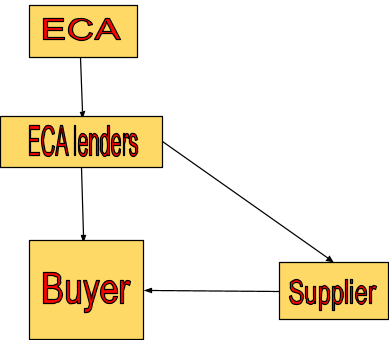

The structure of Export Credit Agency financing

The above chart describes a typical structure of “buyer credit” financing. A commercial bank offers a loan to the buyer, which is utilized to subsidize payments under the agreement between the buyer and the supplier.

The loan will be organized on either a disbursement or reimbursement premises. For instance, the lenders would either pay the supplier directly for each drawdown of the loan or they will pay the buyer once the supplier has been paid in accordance with the arrangement.

Each drawdown notice under the loan should be joined by passing an eligible declaration which will affirm that the loan is being drawn to pay for the agreed amount of goods/services provided under the agreement between the buyer and supplier.

Where an ECA takes part in a project financing close by commercial banks or other funders, the financing documents will generally be organized based on an umbrella common terms contract and then separate facility contracts, interest rates & disbursement mechanics.

ECA ensures/supports agreement:

The commercial loan is upheld by an assurance contract from the ECA, where the ECA is offering a confirmation that it will reimburse the business banks assuming the purchaser fails to make the reimbursement of the credit.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?