Notice of Default

A legal document that acts as a formal notification, alerting the borrower to their default and setting consequential events in motion.

What Is A Notice Of Default?

In finance, the term "Notice of Default" is a legal document that acts as a formal notification, alerting the borrower to their default and setting consequential events in motion. It carries a substantial weight and significance for borrowers and lenders alike.

Understanding the far-reaching implications and intricate processes associated with a Notice of Default is paramount for both parties involved.

For borrowers, it serves as a sobering wake-up call, indicating a breach of their contractual obligations and triggering a cascade of potential repercussions.

For lenders, a Notice of Default is not simply a formality but a critical turning point that necessitates swift and deliberate action.

Upon issuing the Notice, lenders are compelled to evaluate the borrower's default and assess the available avenues for recovering the outstanding debt.

This may involve engaging in legal proceedings, such as foreclosure, to protect their interests and seek recourse for the financial loss incurred.

The impact of a Notice extends beyond the immediate parties involved. Widespread defaults can create a ripple effect, leading to decreased property values and a general sense of instability in the financial landscape.

Throughout this article, we will delve into the multifaceted aspects of a Notice of Default, shedding light on its consequences and the subsequent processes that unfold.

- A Notice of Default (NOD) is a formal notification filed by a lender indicating that a borrower has failed to meet the terms of their loan agreement. It is the first step in the foreclosure process.

- A Notice of Default informs the borrower that they are in default on their loan and provides a timeline for curing the default before further legal action, such as foreclosure, is taken.

- The Notice of Default is filed with the appropriate public office, usually, a county recorder or clerk, and a copy is sent to the borrower. This public filing informs interested parties, including other creditors, that the property is in default.

- The filing of a Notice of Default has a significant negative impact on the borrower’s credit score. It signals severe delinquency and the risk of foreclosure, making it more difficult for the borrower to obtain future credit.

Notice of Default Significance

It holds immense importance in finance, representing formal communication from a lender to a borrower.

Its issuance marks a critical juncture in the foreclosure process, conveying the lender's intent to pursue legal action to recover the outstanding debt.

Impact on Credit Score

Credit reporting agencies note such defaults, and this negative information can remain on the borrower's credit report for several years.

A damaged credit score can severely impact a borrower's ability to secure future loans or obtain favorable interest rates, so it is essential to address the default promptly.

It meticulously records instances of default, and this adverse information can linger on the borrower's credit report for several years, significantly impairing their ability to secure future loans or obtain favorable interest rates.

Note

It becomes imperative to promptly address the default and take appropriate actions to mitigate its long-term consequences.

Opportunities for Resolution

While a Notice may appear daunting, it also presents an opportunity for borrowers to rectify their financial situation. They can use this Notice as a catalyst for proactive measures, such as contacting their lender to discuss possible alternatives to foreclosure.

Although it may initially evoke feelings of apprehension, it can also serve as a potential turning point for borrowers who want to rectify their financial situation.

Note

By leveraging the Notice as a catalyst for proactive measures, such as initiating communication with their lender to explore viable alternatives to foreclosure, borrowers can actively pursue resolutions that safeguard their financial well-being and prospects.

Communication with the Lender

Upon receiving a Notice, open lines of communication with the lender become vital.

Promptly responding to the Notice, engaging in honest and transparent discussions, and providing necessary financial documentation can demonstrate the borrower's commitment to resolving the default.

It is crucial to maintain a constructive dialogue and explore feasible solutions that align the borrower's repayment capabilities with the lender's expectations.

A Notice is a significant milestone in the borrower-lender relationship, serving as a formal notification of a borrower's failure to meet financial obligations. Borrowers must recognize the legal implications, impact on their credit scores, and available resolution options.

Note

By engaging in open communication and proactive measures, borrowers can navigate the Notice of Default process and work towards resolving their financial challenges.

Consequences Of Receiving A Notice Of Default

Receiving a Notice is a substantial occurrence that can bring about extensive implications for borrowers. It acts as a clear signal, emphasizing the need for prompt attention and decisive measures to prevent exacerbating financial difficulties.

Understanding the potential ramifications and taking proactive steps is crucial for borrowers to navigate through this challenging situation successfully.

Timeline and Deadlines Associated

Including information on the timeline and deadlines associated with a Notice of Default can help borrowers understand the situation's urgency and the importance of taking prompt action.

The timeline for responding to the Notice and rectifying the default is critical to prevent further consequences. Borrowers must be aware of the timeframe within which they should address the default and take necessary steps to resolve the financial issues.

Failure to address the default within the specified period can have severe consequences. The lender can initiate foreclosure proceedings, putting the borrower's property at risk of being seized.

A notice of default can also negatively impact the borrower's credit scores. Credit reporting agencies track instances of default, and this information can remain on the borrower's credit report for an extended period.

Note

Promptly addressing the default can help mitigate the long-term damage to creditworthiness.

Borrowers must understand the need for prompt action upon receiving it. Ignoring or delaying the response can worsen the situation and limit the available options for resolution.

Risk of Foreclosure and Legal Action

It is a precursor to the foreclosure process, signaling the lender's intent to recover the outstanding debt through legal means.

If borrowers fail to address the default and rectify the financial issues promptly, they run the risk of losing their property through foreclosure. This can be an emotionally and financially devastating outcome, making it essential for borrowers to take swift action.

As an example, when homeowners receive a Notice of Default, it serves as a severe warning that their property is at risk of foreclosure. Ignoring the default and failing to take immediate action can lead to the lender initiating legal proceedings to recover the outstanding debt.

Note

If the notice is unaddressed, the consequences can be devastating, potentially resulting in the loss of their home. The emotional toll of losing property and the financial burden can be overwhelming.

To avoid a dire outcome, borrowers must act swiftly to rectify the default, explore available options, and seek professional assistance to navigate through this challenging situation and protect their property.

Negative Impact on Credit Scores

The credit reporting agencies closely monitor default instances, and a Notice is no exception. This negative information can tarnish a borrower's credit report for an extended period, typically lasting several years.

A damaged credit score can severely impact the borrower's ability to secure future loans or obtain favorable interest rates, making it essential to address the default promptly.

Note

By proactively rectifying the default, borrowers can mitigate the long-term consequences on their creditworthiness.

Need for Prompt Action

Upon receiving a Notice, borrowers must recognize the situation's urgency. Ignoring or delaying the response can exacerbate the problem and limit the available options for resolution.

Borrowers must assess their financial situation objectively, explore available alternatives, and seek professional advice. Acting promptly can open doors to potential solutions and help minimize the negative repercussions.

In navigating the consequences of a Notice, borrowers should approach the situation with a level-headed mindset.

Seeking guidance from reputable financial advisors, credit counselors, or foreclosure prevention specialists can provide valuable insights and strategies tailored to their specific circumstances.

Note

By taking a proactive stance and addressing the default head-on, borrowers can regain control of their financial future and work towards a favorable resolution.

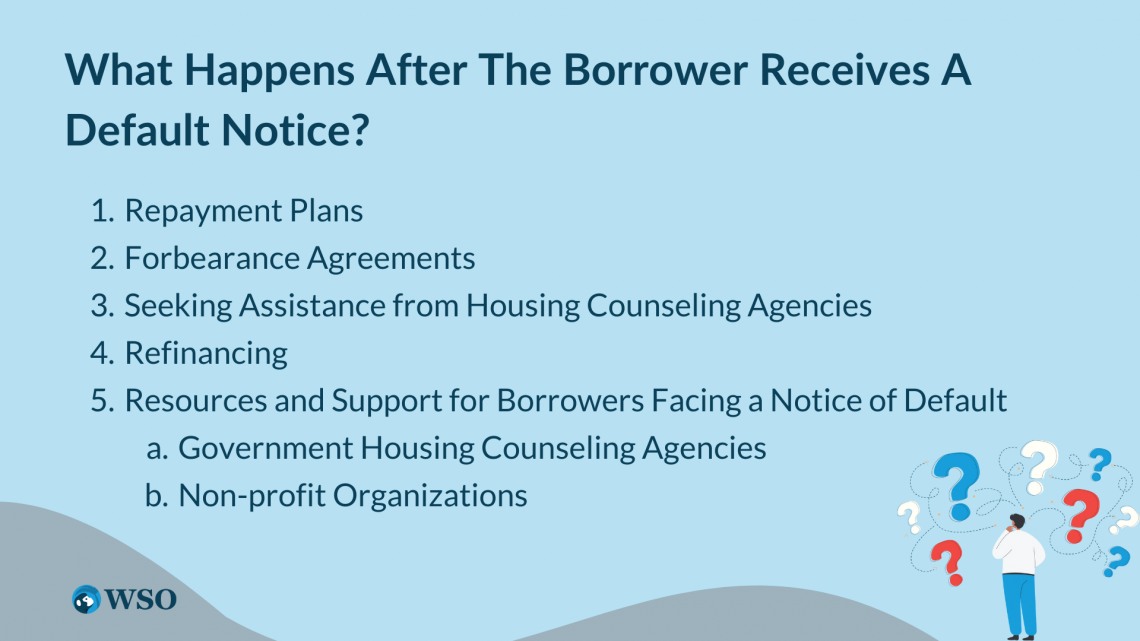

What Happens After the Borrower Receives a Default Notice?

By exploring these alternatives and taking proactive measures, borrowers can increase their chances of resolving the default and avoiding the devastating consequences of foreclosure.

Here are several options borrowers can consider:

1. Repayment Plans

Borrowers can work with their lenders to establish repayment plans that enable them to catch up on lagging payments.

This arrangement enables borrowers to spread out the past-due amount over an agreed-upon period, making it easier to bring the loan back into good standing.

By adhering to the repayment plan, borrowers can demonstrate their commitment to meeting their financial obligations and avoid the dire consequences of foreclosure.

2. Forbearance Agreements

It temporarily relieves borrowers by allowing them to suspend or reduce their mortgage payments.

Note

During the forbearance period, borrowers have some breathing room to stabilize their finances and regain their financial footing.

3. Seeking Assistance from Housing Counseling Agencies

Borrowers can benefit from seeking assistance from housing counseling agencies. These agencies specialize in providing expert guidance, financial education, and personalized advice to individuals facing housing-related challenges.

Housing counselors can help borrowers understand their rights, explore options, and communicate effectively with lenders. They can also negotiate on the borrower's behalf, mediating discussions with lenders to find viable solutions.

With their support, borrowers can make informed decisions and navigate through the complexities of the foreclosure process.

4. Refinancing

In some cases, refinancing may be a viable option for borrowers facing a Notice. This can help lower monthly payments, reduce the interest rate, or even consolidate debt.

Note

When exploring these options, borrowers must act promptly and proactively communicate with their lenders.

Consulting with an experienced attorney specializing in foreclosure and real estate law is crucial for borrowers facing a Notice of Default.

These legal professionals can provide invaluable guidance, ensuring borrowers understand the legal intricacies of the foreclosure process and make informed decisions to protect their rights and interests.

Note

Borrowers who receive a Notice of Default should not lose hope.

Borrowers can take proactive steps toward resolving their default and securing their financial future by considering and pursuing available alternatives such as loan modification, repayment plans, and forbearance agreements.

5. Resources and Support for Borrowers Facing a Notice of Default

During the challenging time of facing a Notice of Default, borrowers can benefit from the resources and support available to help them navigate through the process.

Several organizations and agencies offer assistance and guidance to borrowers in need. These resources include:

a. Government Housing Counseling Agencies

Government housing counseling agencies provide expert advice, financial education, and personalized assistance to individuals facing housing-related challenges.

They can help borrowers understand their rights, explore available options, and communicate effectively with lenders.

Note

These agencies also have the expertise to negotiate on behalf of borrowers, facilitating discussions with lenders to find viable solutions.

b. Non-profit Organizations

Non-profit organizations dedicated to housing assistance can also provide valuable support to borrowers facing a Notice of Default. These organizations offer guidance, financial counseling, and resources tailored to borrowers' specific circumstances.

Seeking professional guidance and support from these resources can empower borrowers to navigate through the complexities of the foreclosure process, understand their options, and take proactive measures to resolve their default.

By leveraging these resources, borrowers can increase their chances of reaching a favorable resolution and securing their financial future.

Note

It is essential to act swiftly, remain diligent, and seek appropriate guidance to increase the likelihood of reaching a favorable resolution and avoiding the long-term consequences of foreclosure.

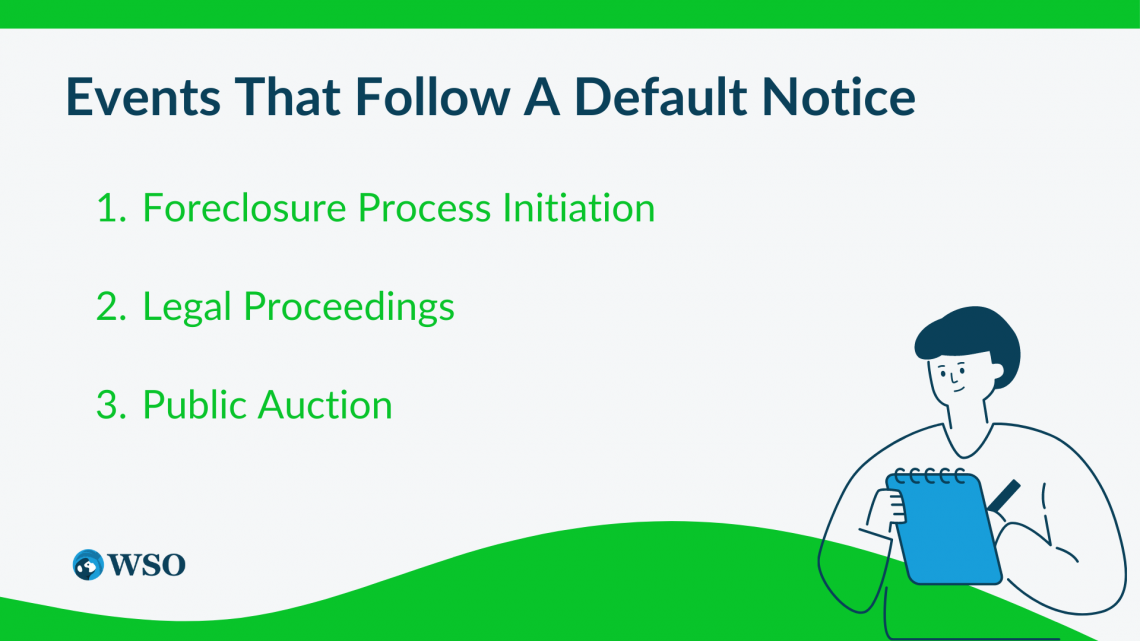

Events That Follow A Default Notice

Lenders' receipt of a Notice of Default signals a violation of the loan agreement by the borrower, leading lenders to take necessary legal action to safeguard their interests and pursue repayment.

It is essential for borrowers facing a Notice to grasp the lender's standpoint and the potential legal actions that might be taken.

For borrowers facing a Notice, comprehending the lenders' perspective and being aware of the potential legal actions they may initiate becomes of utmost importance. Below are several critical considerations to consider:

Foreclosure Process Initiation

Lenders often initiate the foreclosure process upon receiving a Notice of Default. This process involves a series of legal steps designed to enforce the lender's right to recover the outstanding debt by selling the property and securing the loan.

Note

The foreclosure process may vary depending on the jurisdiction and the specific terms outlined in the loan agreement.

Legal Proceedings

Lenders typically initiate legal proceedings against the borrower as part of the foreclosure process. The legal proceedings provide lenders with a legal framework to assert their rights, present evidence of the borrower's default, and seek approval to proceed with the foreclosure.

To reiterate, the issuance of a Notice of Default is triggered by specific legal requirements outlined in the loan agreement. These requirements typically include conditions or events such as missed payments, violation of loan covenants, or failure to maintain adequate insurance.

Note

Once the conditions are met, the lender can initiate foreclosure by issuing the Notice of Default.

Public Auction

Once the court grants permission for foreclosure, lenders may proceed with a public auction of the property. The proceeds from the auction are then used to recover the outstanding loan amount, including any associated fees and expenses.

Borrowers must communicate openly and transparently with their lenders to explore potential alternatives and negotiate feasible solutions.

By taking proactive measures and addressing the default promptly, borrowers can potentially mitigate the impact of legal actions and work towards a satisfactory resolution.

Lenders view a Notice of Default as a serious breach of the loan agreement, which can prompt them to initiate legal actions, including the foreclosure process, to recover the outstanding debt.

Borrowers should be aware of the potential legal consequences, take appropriate steps to address the default and seek viable solutions.

Note

Seeking professional advice and maintaining open communication with lenders are essential in navigating the lender's perspective and legal actions, ultimately aiming to achieve a satisfactory resolution for all parties involved.

Conclusion

Both borrowers and lenders must grasp the significance of a Notice of Default and its impact on their financial journey. For borrowers, it is essential to tackle defaults head-on and take proactive steps to improve their financial situation.

This involves considering various options like modifying their loan, setting up repayment plans, seeking forbearance agreements, or contacting housing counseling agencies for guidance.

By promptly addressing defaults and maintaining open communication with their lenders, borrowers increase their chances of minimizing the unfavorable outcomes typically associated with a Notice.

On the other hand, lenders have their own set of responsibilities when faced with a Notice of Default. They must adhere to legal procedures and evaluate the most appropriate course of action to recover the outstanding debt.

This may involve initiating the foreclosure process, which entails legal proceedings, public auction, and ultimately the sale of the property to recoup the loan amount.

Lenders need to exercise due diligence and make informed decisions to safeguard their interests while also considering potential alternatives to foreclosure that could be mutually beneficial for both parties.

By staying well-informed about the implications and processes of a Notice, borrowers, and lenders can navigate this challenging situation more effectively.

Likewise, lenders must approach the situation with a thorough understanding of their legal rights and obligations while exploring alternatives that may provide a resolution without foreclosure.

Note

A Notice is a significant event that demands attention and action from borrowers and lenders.

By taking proactive steps, seeking professional assistance, and maintaining open lines of communication, borrowers, and lenders can work towards resolving defaults and mitigating the associated consequences.

With a well-informed and collaborative approach, the complexities of a Notice of Default can be navigated with greater efficiency and the potential for mutually beneficial outcomes.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?