Bank Stress Test

Examination executed by regulatory authorities to identify weaknesses, evaluate capital reserves, and improve risk management in the banking sector.

What Is A Bank Stress Test?

Bank stress tests are rigorous examinations executed by regulatory agencies to examine the ability of banks to endure poor economic situations and preserve stability.

By subjecting banks to rigorous evaluations under challenging economic scenarios, stress tests provide valuable insights into their resilience and capacity to manage risks.

By subjecting banks to hypothetical stress scenarios, regulators evaluate their ability to withstand severe economic shocks, such as economic recessions, market downturns, or liquidity constraints.

Bank stress tests identify potential weaknesses, evaluate the sufficiency of capital reserves, and improve risk management practices within the banking sector.

These tests are designed to uncover the vulnerabilities that could threaten financial stability. By conducting stress tests, regulatory authorities can assess the adequacy of banks' capital buffers and ensure they have effective risk management strategies.

The ultimate goal is to enhance the overall resilience and stability of the banking sector.

The results of stress tests inform regulatory actions, such as capital requirements or risk mitigation measures, and contribute to maintaining financial stability and market confidence.

- A bank stress test is an analysis conducted to determine how a bank can handle economic and financial stress.

- It evaluates the impact of hypothetical adverse scenarios on a bank’s financial health, including its capital adequacy, liquidity, and overall stability.

- The primary purpose of bank stress tests is to ensure that banks have enough capital to withstand economic downturns and financial crises by identifying potential vulnerabilities and ensuring that banks can continue to operate under severe conditions.

- Stress tests are often mandated by regulatory authorities such as the Federal Reserve in the United States, the European Central Bank (ECB), and other national regulators.

Understanding Bank Stress Test

A bank stress test is a comprehensive assessment conducted by regulatory authorities to evaluate the resilience and stability of banks in adverse economic scenarios.

It involves subjecting banks to simulated stress conditions, such as economic downturns or market shocks, to assess their ability to withstand and recover from severe financial strains.

Regulatory authorities use this information to project the potential impact of adverse scenarios on the banks' financial health. The tests typically evaluate metrics such as:

- Capital adequacy

- Liquidity positions

- Asset quality under stress conditions

The scenarios used in stress tests are carefully designed to reflect realistic and severe conditions that banks may face. They incorporate factors such as:

- Economic indicators

- Interest rate changes

- Market shocks

By subjecting banks to these hypothetical stress scenarios, regulators can identify potential vulnerabilities, assess the banking system's resilience, and make informed policy decisions.

The test results provide valuable insights into the banks' ability to absorb losses, maintain solvency, and continue providing critical financial services.

Based on the findings, regulatory authorities can take appropriate actions to address any identified weaknesses or risks within the banking system. These actions may include:

- Requiring banks to maintain higher capital reserves

- Implementing risk mitigation measures

- Enhancing Supervision and Regulation

Bank stress tests play a crucial role in promoting financial stability by identifying and addressing potential weaknesses in the banking system. They help enhance risk management practices, ensure capital adequacy, and maintain investor confidence.

Note

By conducting these tests regularly, regulatory authorities aim to prevent future financial crises and maintain a healthy and resilient banking sector.

The purpose of bank stress test

The purpose of bank stress tests is multi-fold and serves several important objectives:

1. Assessing Capital Adequacy

Stress tests are conducted to evaluate the capital adequacy of banks. They assess whether banks have sufficient capital reserves to withstand severe economic and financial shocks.

Adequate capital cushions ensure that banks can absorb losses and continue to fulfill their financial obligations, safeguarding the interests of depositors and creditors.

2. Identifying Risks and Vulnerabilities

Stress tests help identify potential risks and vulnerabilities within the banking system. By subjecting banks to adverse scenarios, regulators can evaluate their performance under stress conditions and identify areas of weakness.

3. Enhancing Risk Management Practices

Stress tests are crucial in promoting sound risk management practices within banks. The findings from stress tests enable regulators to identify gaps or deficiencies in banks' risk identification, measurement, and mitigation strategies.

This allows for implementing measures to enhance risk management frameworks, ensuring banks are better prepared to navigate challenging situations.

4. Informing Regulatory Actions

The results of stress tests inform regulatory actions and decision-making. For example, if stress test results reveal capital deficiencies or weaknesses, regulators may require banks to take corrective actions, such as raising additional capital or adjusting risk management practices.

5. Promoting Investor and Market Confidence

The transparency and disclosure of stress test results contribute to increasing investor and market confidence. In addition, stress tests provide stakeholders with insights into the resilience and ability of banks to withstand adverse economic conditions.

This transparency reduces uncertainties and promotes trust, which is vital for maintaining a healthy financial system.

They provide regulators with a comprehensive assessment of banks' resilience, help identify potential risks and vulnerabilities, and drive actions to enhance risk management practices.

By conducting stress tests, regulators aim to prevent future financial crises, protect stakeholders' interests, and maintain the overall integrity of the financial system.

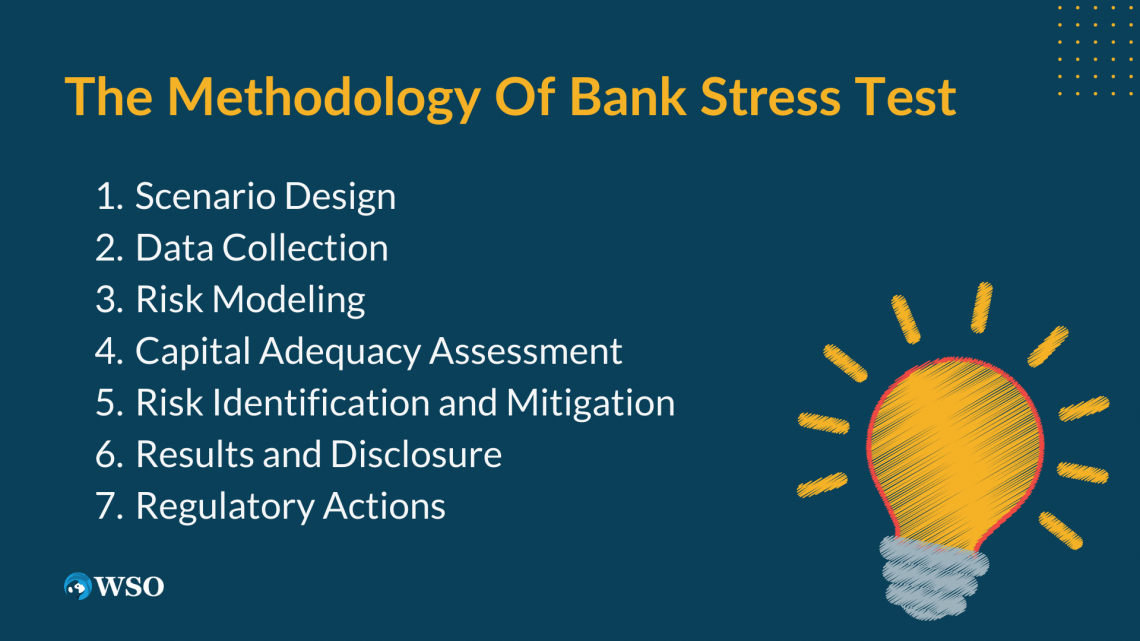

The Methodology of Bank Stress Test

Bank stress tests employ a specific methodology to assess the resilience of banks and measure their ability to withstand adverse economic conditions. While specific methodologies may vary among regulatory authorities, the following key elements are typically involved in the process:

Scenario Design

Regulatory authorities develop a set of stress scenarios that encompass a range of severe economic and financial conditions.

These scenarios are carefully constructed to reflect realistic and plausible stress events, such as economic recessions, interest rate fluctuations, housing market crashes, or geopolitical shocks. In addition, the scenarios consider systemic and idiosyncratic risks that could impact individual banks.

Data Collection

Banks must provide extensive data to regulators, including information on their balance sheets, risk exposures, capital positions, and liquidity profiles. This data forms the basis for projecting banks' financial performance under stress scenarios.

Risk Modeling

Regulatory authorities use sophisticated risk models to estimate the potential impact of stress scenarios on banks' financial health. These models consider factors such as

- Credit defaults

- Market value declines

- Interest rate changes

- Liquidity pressures

The models incorporate historical data, statistical analysis, and assumptions to simulate the behavior of banks' portfolios and measure their resilience.

Capital Adequacy Assessment

Stress tests evaluate banks' capital adequacy under stress conditions. This involves calculating regulatory capital ratios under stress scenarios like the Common Equity Tier 1 (CET1) ratio.

Note

The results help determine whether banks have sufficient capital buffers to absorb losses and maintain solvency.

Risk Identification and Mitigation

Stress tests aim to identify risks and vulnerabilities within banks' operations. They assess credit risk, market risk, liquidity risk, and other potential sources of risk.

The tests highlight areas where banks may need to strengthen risk management practices, improve asset quality, or enhance liquidity management strategies.

Results and Disclosure

Once the stress tests are completed, regulators communicate the results to the participating banks. The outcomes regarding capital adequacy ratios, risk exposures, and other relevant metrics are typically reported.

Stress test results are often disclosed to the public, promoting transparency and market discipline.

Regulatory Actions

The results of stress tests inform regulatory actions and decisions. For example, if vulnerabilities or capital deficiencies are identified, regulators may require banks to take corrective measures, such as raising additional capital, adjusting risk models, or enhancing capital planning processes.

By following a consistent and rigorous methodology, tests provide regulators with a comprehensive understanding of banks' potential risks and help shape appropriate measures to maintain financial stability.

The continuous refinement of stress testing methodologies ensures their effectiveness in assessing and addressing systemic risks within the banking sector.

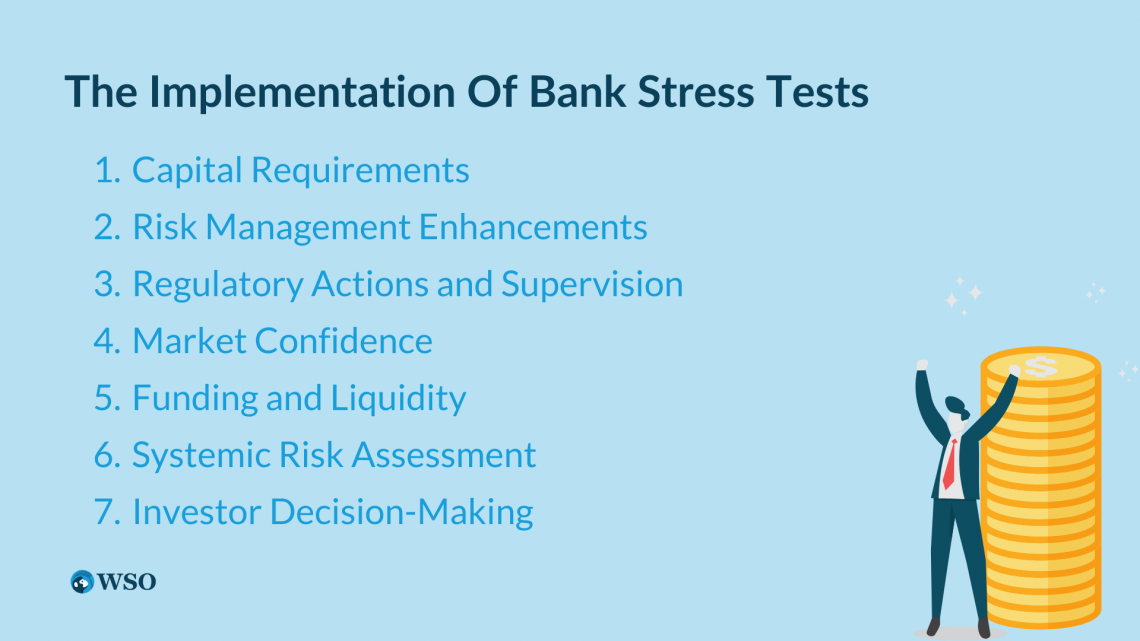

The implementation of bank stress tests

Bank stress tests have significant implications for both banks and regulatory authorities. Here are some key implications of bank stress tests:

Capital Requirements

Stress test results may lead to bank capital requirements changes. For example, if a stress test reveals capital deficiencies or vulnerabilities, regulatory authorities may require banks to increase their capital buffers to ensure sufficient reserves to absorb potential losses.

This can impact banks' profitability and ability to distribute dividends or engage in certain activities.

Risk Management Enhancements

Stress tests highlight areas where banks may need to improve their risk management practices. Regulatory authorities may issue recommendations or requirements for banks to enhance risk identification, measurement, and mitigation strategies.

This can involve improving credit risk assessments, liquidity management frameworks, stress testing models, and overall risk governance.

Regulatory Actions and Supervision

Stress test results inform regulatory actions and supervision. For example, if significant weaknesses or vulnerabilities are identified, regulators may implement specific measures or bank restrictions to mitigate risks.

This can include additional reporting requirements, enhanced supervisory oversight, or limitations on certain activities until the identified risks are adequately addressed.

Market Confidence

The transparency and disclosure of stress test results can directly impact market confidence. When stress test outcomes are made public, investors, depositors, and other market participants gain insights into the resilience and stability of banks.

Funding and Liquidity

Stress test results may affect banks' access to funding and liquidity. For example, if stress test outcomes reveal weaknesses in liquidity management or funding sources, it may become more challenging for banks to raise funds or access certain types of financing.

This can impact their ability to meet obligations and maintain liquidity in stressed market conditions.

Systemic Risk Assessment

Tests contribute to the assessment of systemic risks within the financial system. By evaluating the collective resilience of banks, regulators gain insights into potential vulnerabilities and risks that could have systemic implications.

This information can guide macroprudential policies and systemic risk mitigations to safeguard the overall stability of the financial system.

Investor Decision-Making

Stress test results can influence investor decision-making. Investors consider stress test outcomes as part of their risk assessment process and may adjust their investment strategies or portfolios based on the perceived resilience of banks.

Positive stress test results can attract investor interest, while negative results may lead to reduced investor confidence and potential divestments.

Tests have broad implications for capital requirements, risk management practices, regulatory actions, market confidence, funding, systemic risk assessment, and investor decision-making.

By identifying weaknesses, mitigating risks, and enhancing the overall stability of banks, stress tests contribute to a resilient and sound banking system better equipped to withstand adverse economic conditions.

Bank Stress Test FAQs

A bank stress test is a comprehensive evaluation conducted by regulatory authorities to assess the resilience and stability of banks in adverse economic conditions. It involves subjecting banks to simulated stress scenarios to evaluate their ability to withstand severe financial shocks.

Tests are conducted to prevent future financial crises, ensure the soundness of the banking system, and protect the interests of depositors and stakeholders. They identify potential vulnerabilities, assess capital adequacy, enhance risk management practices, and inform regulatory actions.

Regulatory authorities carefully designed stress scenarios to reflect realistic and severe economic and financial conditions.

They include economic recessions, interest rate fluctuations, housing market crashes, or geopolitical shocks and aim to capture systemic and idiosyncratic risks.

Banks must provide extensive data on their balance sheets, risk exposures, capital positions, and liquidity profiles. This data is used to project banks' financial performance under stress scenarios and evaluate their resilience.

Stress test results inform regulatory actions and decision-making.

Yes, stress test results can have implications for banks' operations. For example, they can lead to changes in capital requirements, requirements to enhance risk management practices, increased regulatory scrutiny, and potential limitations on certain activities.

Stress test results are often disclosed to the public to promote transparency and market discipline. In addition, the public disclosure of results helps to increase investor and market confidence by providing insights into the resilience of banks.

Stress tests are crucial in promoting financial stability by identifying and addressing potential weaknesses in the banking system. They help ensure capital adequacy, enhance risk management practices, and maintain the overall resilience of the banking sector.

The frequency of tests varies across jurisdictions. However, they are often conducted annually or regularly to ensure ongoing monitoring and assessment of banks' resilience to changing economic conditions.

While stress tests cannot predict future financial crises with certainty, they provide valuable insights into the ability of banks to withstand adverse conditions. Moreover, by identifying vulnerabilities and weaknesses, stress tests contribute to the early detection and prevention of potential risks that could lead to financial instability.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?