Vendor Financing

A financial arrangement for a vendor seeking supplier credit extension to a buyer to help acquire goods and services.

What Is Vendor Financing?

Vendor financing is a financial arrangement for a vendor to seek supplier credit extension to a buyer or customer to aid in acquiring goods and services.

When a buyer enters into a purchase agreement with a seller, there is an exchange of goods or services against an asset that takes the form of money. To finance this purchase, a buyer has several options. He may use his money or borrow from a third party.

These options are the basics of finance. Vendor financing is a form of borrowing money. The main difference is that you don't borrow directly from a third party but from a seller. It can also be called trade credit.

Companies very often use this type of financing. Accounts receivable and accounts payable are the best examples. Accounts receivable means that a company has been delivered goods or services by its suppliers without paying them.

Accounts payable is when a company has yet to be paid for servicing its clients. In both instances, those who owe money are financed by vendors because they are granted a certain period to make a payment.

In M&A (mergers and acquisitions), vendor financing or seller's loan is also one of the solutions to facilitate deal funding. It is often up to 20% of the purchase price and stands at the same level as the buyer's contribution, bank, and institutional debt.

- Vendor financing, also known as supplier financing or trade credit, refers to a financial arrangement where a vendor or supplier extends credit to a customer or buyer to facilitate purchases of goods or services.

- It involves three parties: the vendor/supplier offering goods or services, the customer/buyer receiving the goods or services, and often a financial institution facilitating the credit extension.

- Vendor financing helps businesses manage cash flow by allowing them to defer payment for purchases, typically under agreed-upon terms such as net 30, net 60, or longer periods, thereby easing immediate financial burdens.

- Both parties must carefully manage risks associated with vendor financing, such as credit risk (default by the buyer), interest rate risk, and potential strain on supplier liquidity if credit terms are too favorable.

Understanding Vendor Financing

It is a form of debt used in acquisitions allowing buyers to reduce the purchase price. Likewise, sellers receive the purchase price diminished by the amount of the debt they accord to buyers.

For instance, assume a purchase price of $100M and a 10% seller financing loan. The buyer must pay only $90M since the seller loans another $10M (10%). Of course, it is only ideal for a seller to sell its assets if they are not fully paid, but there are many upsides for both participants.

One of the most undeniable advantages is flexibility. It reduces the time for closing and eventually speeds up the deal execution. In addition, since a buyer needs to find less cash for the acquisition, he will rely less on other capital providers.

Vendor financing is perfect for intangible capital-intensive companies. Traditional loans are often reserved for companies with a solid tangible asset base to use as collateral.

Note

Collateralized loans are called secured loans.

The seller's willingness to participate in financing is usually perceived as a good sign. If you sell on credit, you believe that your counterparty has the potential to repay and will do it. This confidence can entice banks and convince them of the safety of an operation.

Also, under this financing, sellers have two additional power leverages. If a buyer can't easily fund the operation, the vendor's participation becomes instrumental in closing. If a seller doesn't consider a buyer the most suitable, he can withdraw from a deal and make it invalid.

Additionally, as the seller still has interests in his company after putting vendor financing in place, he can express his opinion and advice on the better management of a business. It reinforced the bond between seller and buyer.

Lending money is always dangerous. But the vendor has a list of safeguards allowing him to feel his money secured.

- First, it is an obligation or a legally binding agreement forcing the buyer to repay the seller.

- Second, if the borrower defaults, the seller can sell a company's assets or even repossess them.

- Third, having the means to share opinions on the best practices to manage a company can help to avoid the worst scenario.

Note

If you envision this type of financing, start the negotiation process as soon as possible.

It is a debt financing, so its conditions, terms, and constraints should be understood and approved by everyone as if it was a bank loan.

The main items to agree on are:

- Maturity

- Amount

- Deferred period

- Interests

Seller's loans can be deferred, and their eventual reimbursement sometimes starts after some time. Typically this loan has a maturity of three years but can be extended to five.

You may wonder how a vendor's loan is ranked among other types of debt in a transaction. Often, it works as a junior debt. It means that it is a subordinated debt and can be paid back after a senior debt has been fully repaid to creditors.

It is not prohibited to start paying back the vendor's loan even if there is still some outstanding senior debt. Robust financial performance can allow the buyer to use dividends to make step-by-step payments to the seller.

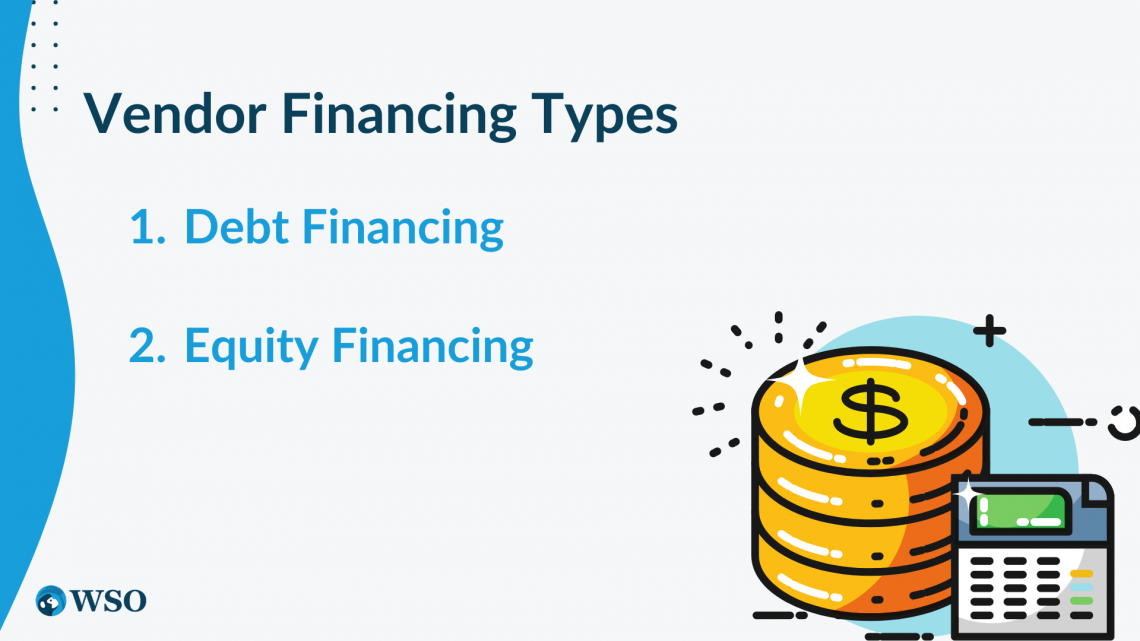

Vendor Financing Types

There are generally two types of vendor financing:

Debt Financing

The borrower agrees to a sales price and a fixed interest rate. The lender earns the interest when the borrower pays back the installments. If the borrower can't service this debt, he defaults on it. Such a loan will be marked as bad debt.

Nevertheless, the lender can take legal action to recover the outstanding amount before writing off the debt.

Equity Financing

It allows a buyer to purchase an asset without paying money upfront. Instead, the seller is paid with stocks in the borrower company.

This operation makes the seller a shareholder, and they can get paid dividends. As a shareholder, the seller also gets to have a say in important decisions made by the borrower company.

In an M&A transaction, debt financing could be associated with a full or partial cash deal. Conversely, equity financing is used in a shares deal.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?