THE NEXT CATASTROPHE

So here is the gist of why I am extremely worried. Don't look at this until you have fifteen minutes to digest it all -

According to a July 2007 report by AMP Capital Investors, the total value of all sub prime loans was approximately $1.4 trillion, of which only about one-third of outstanding loans could reasonably be expected to default. Even if a loan defaults, it isn't a total loss as the bank can sell the home.

If we assume that in the event of a default, a home can still be sold off, on average, for two-thirds of its original value, the total losses on sub prime loans shouldn't have gone much higher than $150 billion.

Much - Most - of the current crisis stemmed from the defaulting of sub prime loans that were disguised as "super-senior" triple A risk loans inside billions of dollars of CDOs. There were other things, but the crisis could have been abated if not for this. So, with those billions of dollars spread throughout CDOs, added to the fear factor, the financial sector was hit by an earthquake of 9.0 on the Richter scale.Thankfully, the financial system was sound at the time and the banks were hit hard, but most of them absorbed the hit, with the help of nearly a trillion from the fed. Point: it butchered the market in everywhere but the major arteries. We are left with a system that is barely intact, but still exists. It would appear that housing has hit a bottom, right? Or somewhere close to it. Here is the problem:

Option-ARMS and ALT-A

Payment option ARMs are popular negative amortization mortgages with recast features. Most payment option ARM’s have a scheduled recast in month 61. Additionally, they have triggers that might cause an unscheduled recast to occur if a negative amortization limit is reached. For example, if the principal balance of the loan reaches a set limit through negative amortization, a recasting of the mortgage is triggered.

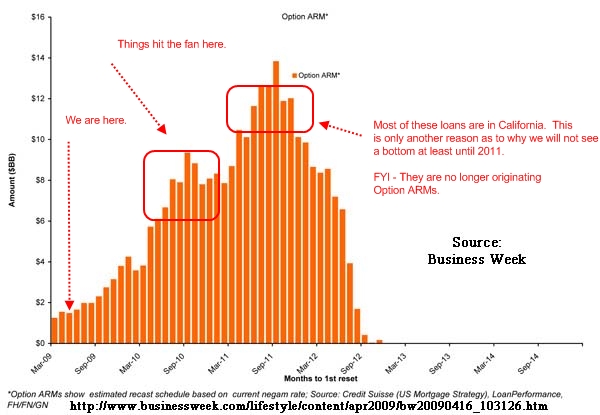

Here are some numbers -

California At the end of March 2009 Sub prime loans active: $119 billion Alt-A loans active: $288 billion U.S. Alt-A active: $469 billion When we talk about the $500 billion in Alt-A mortgages this is what we are talking about. Last time I checked $469 billion does not mean the problem has gone away.

Link to Image

http://www.doctorhousingbubble.com/wp-content/upl…

We are going to start seeing $8 to $10 billion per month recast, nearly 5 times the current rate. The chart states “months to 1st reset” but they are referring to recasts brought on by negative amortization. And as you will see, since the majority of these loans are in California the bulk are underwater Jacque Cousteau style. Wachovia in their infinite wisdom swallowed up Golden West at the height of the lending insanity. This cratered the bank which was taken over by Wells Fargo. Just because you eat a bank doesn’t mean the toxic waste suddenly disappears. In fact, there is still well over $100 billion in Pick-A-Pay mortgages in their portfolio. Wells Fargo has written off a portion of the portfolio but there is still a significant amount remaining: About 1 million option ARMs are estimated to reset higher in the next four years, according to real estate data firm First American CoreLogic of Santa Ana, California. About three quarters of those loans will adjust next year and in 2011, with the peak coming in August 2011 when about 54,000 loans recast, the data show. Option ARM borrowers hit with unaffordable monthly payments are another threat to the housing recovery and the economy, said Susan Wachter, a professor of real estate finance at the University of Pennsylvania’s Wharton School in Philadelphia. Owners who surrender properties to the bank rather than make higher payments for homes that have plummeted in value will further depress real estate prices and add to the inventory of properties on the market, she said. “The option ARM recasts will drive up the foreclosure supply, undermining the recovery in the housing market,” Wachter said in an interview. “The option ARMs will be part of the reason that the path to recovery will be long and slow.” Option ARM recasts will mean more pain for California, the state with the most foreclosures in the U.S. It's $750 Billion Problem More than $750 billion of option ARMs were originated in the U.S. between 2004 and 2007, according to data from First American and Inside Mortgage Finance of Bethesda, Maryland. California accounted for 58 percent of option ARMs, according to a report by T2 Partners LLC, citing data from Amherst Securities and Loan Performance. If it takes month 61 to recast, that means they will recast between late 2009 and 2012 Here is an example: Shirley Breitmaier took out a $315,000 option ARM to refinance a previous loan on her house. Her payments started at 3/8 of 1 percent, or less than $100 a month, according to Cameron Pannabecker, the owner of Cal-Pro Mortgage and the Mortgage Modification Center in Stockton, California, who is working with Breitmaier. The loan allowed her to forgo higher payments by adding the unpaid balance to the principal. She’ll be required to start paying principal and interest to amortize the debt when the loan reaches 145 percent of the original amount borrowed. When that happens, she won't be able to afford it! Imagine paying 100 dollars a month on a mortgage (just interest) and then jumping to 7000 dollars a month (more interest plus backed payments plus you're already underwater because of current crisis)

What we do know as of today is that 40 percent of option ARM borrowers are now at least 60 days late. Fitch in their September release stated that 70 percent of the securitizedARMs would hit recast dates by 2011. So the next two years will see billions of these loans transform into more trouble for banks. In order to understand how we got here, let us look at Q2 of 2007 data I gathered on the top option ARM lenders at that time:

Image

http://financemymoney.com/wp-content/uploads/2009…

The top 10 option ARM lenders held onto 66 percent of the market in 2007. 2006 and 2007 saw the biggest amount of these loans made. From 2004 to 2007 some $750 billion in option ARMs were made. If you look at the list, only two of the institutions still stand. Washington Mutual is now part of JP Morgan, Countrywide is now part of Bank of America, and Wachovia is now part of Wells Fargo. The names are different but many of the loans are still out there. These above banks dominated the entire option ARM market:

http://financemymoney.com/wp-content/uploads/2009…

These loans are highly toxic because many had a massively low teaser rate that negatively amortized the loan. That is, the initial balance actually grew if you decided to make the minimum payment option. According to recent data 93 percent of option ARM borrowers elected to go with this minimum payment option. Many of these loans were cast with a five year time frame before rates hit major recast points. One of the more recent charts shows this wave: There have been many charts like the ones above and much of the confusion is around a few key points: -1. Banks have been circumspect given the actual number of option ARMs -2. Many option ARMs are in California (roughly 60 percent of the market) -3. Many of those behind on payments are now simply not paying their mortgage but banks are not moving Now, there are two possibilities

1 - Fed Bought All of these behind closed doors Outcome: FNM FRE collapse entirely, markets sink like a rock 2- Banks are still holding on to these Outcome: US Banking Sector collapses entirely

Knowing what we know, assuming you agree, we have to do the hard thing. Figure out where and when to put our money so that A, we are not blown out of the water and B, we can make more money off of it...as cruel as that may sound

Also, do not forget that these loans do not default necessarily immediately after recast. AND, BEFORE the initial collapse, these loans had a default rate upward of 25%, AFTER the meltdown, you can only imagine how bad it will be. Look what 200 bil in sub prime did! Wait until this nuke goes off. We're only in the eye of the storm, this is when we plan.

Tell me your thoughts, I figured you would be the guys to bring this to.

{kind=link}

{kind=link}

{kind=link}

Are you from zerohedge? Cause those guys have been talking about this for like the last year. Also, loans for commercial properties are gonna be even bigger than this... Basically, 2012 is the meltdown year.

No, actually, I am a high school senior who is looking to go into the industry. This is something that I have known for a looong time, I placed in a state-wide stock market trading competition in 6th grade and I have loved trading stocks ever since. I have been accepted with full scholarship to Babson College and, unless I get into MIT (find out april 1st), I will be entering there with concentrations in quantitive methods and computational finance in the honors program. This site is exactly what I have been looking for, wish i found it ealrier in my "career".

to be honest -- this is exactly why I have had a bearish view on the market and continue to be skeptical of this "recovery."

When I was at my last PE fund we invested in a "mortgage foreclosure processor" so I studied the wave of Alt-As, and subprime in particular. (in NY state and nationally) The really scary thought is the fact that this wave is only when the rates change. It can take over a year for a bank to actually foreclose on a property and can cost several thousand $s in legal fees, etc...especially since you often have to evict, serve, etc.

I guess it really comes down to what is happening behind close doors...are there any economists / politicians / feds specifically addressing this or do they feel the current programs (TARP, etc.) are sufficient to get us through the next wave?

My thoughts are that no matter what, this wave is going to hit, where it hits hardest, like you said, wil be up to what is happening behind closed doors. Obviously, the fed is not going to publicly exclaim this data to the world, a lot of people haveno idea any of this stuff exists! For all we know the fed could be preparing a plan to buy all of these much more than toxic assets. FNM or FRE could go bust, BBs could go bust (it all depends on where this stuff ends up), but with the response to the subprime crisis, i could only imagine this being much worse.

In my opinion, people have also largely overlooked the fact that Second-Lien mortgages have not really been written down by banks.

Wow. Not up to speed on this but thanks for the read.

You'll find out sooner than that bro. MIT decisions come out on March 14th at 1:59 PM, not April first like the Ivies. I have to say, that is extremly creative of them. Ha, how did you not know that ? :P

http://www.mitadmissions.org/topics/apply/the_selection_process_applica…

In all seriousness though, great post. You're way ahead of your peers, me included. Good luck with the whole college thing.

were a lot of these alt-A and ARM stuff securitized?

if so, we should look at how they are trading in the market right now... the guys trading this stuff (ABS groups @ BBs) should know their shit...market should be pricing in this probability of catastrophe.

I'm not sure, but subprime mortgages were securitized and it took a very, very small percentage of a CDO to be subprime for it to go belly up. Furthermore, bankers didn't realize their errs (or at least it wasn't priced in) until knowledge of subprime junk mixed in, even though it was "super-senior" risk, was made widespread, now, in terms of when this stuff takes effect, we could not notice it for a few quarters.

I do know that this is legit.

In addition, once the gov ended the new home buyer tax credit, home sales tanked this past fall, immediately after, the gov reinstated the tax credit, which will run out at the end of spring, which is why i think a lot of our home optimism is backed up by short-run data samples!

Whether or not this stuff is securitized, like i said, i dont know, but here are a few articles that show the tip of the tip of the tip of the iceberg.

http://www.washingtonpost.com/wp-dyn/content/article/2010/01/08/AR20100…

http://www.dailyfinance.com/story/jumbo-mortgage-delinquencies-soar-as-…

I feel that we are on a sugar high. It will wear off eventually, I see problems arising as early as 3Q '10 as late as 2Q '11, but we'll feel the tremors within a year, I think.

BTW, another forum was created in regards to cali default risks, if this is as bad as it looks to be, cali is in for a rude awakening, once these homes go in to recast that is....

Yeah a lot of it is securitized. Commercial loans were of particular concern.

I'll be buying a home in Cali come 2013.

haha amen to that

Why not just have these loans refinanced to fixed now while mortgage rates are low? If they can't because the property is underwater or they just have bad credit, I thought a bunch of banks had special programs subsidized by the GSEs to make adjustments to mortgages (even securitized ones without provoking litigation from CMO/MBS investors) ...

Also do u know what types of growth factors are baked into these estimates in terms of GDP, employment, inflation? Looks like the chart you're citing was made right after the stock market hit bottom in '09 and many people harbored overly pessimistic outlooks.

despite the many ads for refinancing, refinancing is becoming extremely hard with the lack of available credit, plus, if it were set to fixed rate, the payments would still be extremely high! Once a mortgage like this has been set up, it is a matter of time before it recasts and, like i said, even if it were to recast to normal rates, the underwater aspect of the loan + the fact that these people thought they could get by with a 100$/month payment for the first few years and are not yet ready to pay the full payment is bad....as for the "pessimistic outlooks", that chart was not made with opinion, that chart was made with factual data on the number of mortgage made like this, and that chart is recasts, not delinquincies.... keep in mind that BEFORE the crisis, delinquincy rates on these loans were around 33%, let alone now.

it is in the nature of these loans to be highly risky, much more risky than subprime, especially after recast and especially during a time like this, i again refer you to the articles, expect more of this AFTER the home tax credit goes away and house market data gets some truth to it

Outstanding post. You are way ahead of the curve for a high school senior. God damn. Nicely done. If you don't already read zerohedge.com, I suggest you check it out.

part of the problem with refinancing was that people, before the recession would gain 20,000 in equity on their home loans, refinance it all, take their equity and renovate, or spend = very easily drowning mortgages come home value drop

Before I continue I agree this was a very great post for someone in the industry, never mind a kid in HS.

That being said, what I was getting at above is that the situation isn't as catastrophic as doomsayers like to believe. I think something similar to the Home Affordable Modification Program (put in place after this study was conducted) could help forgo the death spiral we saw in the nascent months of the 1st housing crisis (defaults on loans spur foreclosures, excess supply drives down prices, homeowners go underwater and eventually default...) by keeping people in their homes at affordable fixed rates. It's likely the GSEs would bear a large portion of those losses, but with the explicit backing of the government I can't see them collapsing entirely.

Second, with regards to the "pessimistic outlook", while it remains obvious that the number of option ARMs created is a matter of fact, there are still assumptions/opinions that need to be baked into the forecast you cited; Namely, employment figures, GDP, inflation and the like. The chart assumes that borrowers will continue to opt for minimum payments, which may not be true if employment rebounds or the economy continues to improve. One could also argue that all the idiots/liars who got into these option ARMs without the means/inclination to pay are being weeded out and the more fiscally responsible homeowners (those who will do what it takes to make payments) are left. I say this only because there are a lot of qualitative considerations and assumptions that are being made, which may or may not be an accurate representation of what's really going on.... just something to think about

this little guy has been floating around our office:

http://www.scribd.com/doc/27742328/UBS-RE-Research

i actually have a ton of re mkt research...all sad news.

cre is bad news too. i have some notes form ULI SF conference back in Nov. a lady who was hi up the ladder from the fed was there, and what she said was FAWKIN OUTRAGEOUS. basically, treasury and the fed's stance on the commercial re finance issue is:

its is now official fed/treasury policy to 'pretend and extend' troubled loans. in other words, if you banks can make an analysis (ie spreadsheet) that says the loan on a 'troubled asset' can be amortized, or the rate can be reduced AND the economy will be growing in 3-5 yrs (fairy tales), the loan does not have to be written down (impairment) EVEN IF if the loan is more than the building's value. loans may be modified through rate reductions, deffered pmts, whatever whatever, etc etc ....BUT NOT PRINICPAL REDUCTION. basically, this is kind of what is happening in residential re....suspension of free mkt economics.

her justification: administartion's policy (Obama's policy) is to focus on unemployment. employment should boost the economy, which in turn will stabilize demand for re. guys, some of the most senior people in cre in CA were there in the room. they ripped her to pieces and politely expressed, in no uncertain terms, that this was TERRIBLE policy.

her response: what do you want us to do? bankrupt the financial system? that is the alternative.

you can infer a couple of things from this convo:

*the re problem is going to take a lot longer to solve, meaning the recession is going to last for a while and any 'green shoots' are really just artificial (cash for clunkers, first time homebuyer subsidy).

*banks are weak and wont be lending like normal anytime soon.

*a MASSIVE refi problem is just being deferred, with no solution to address it (this is killer).

*the govt is playing politics, with little regard to the consequences (maybe they are expecting the next administration to take the blame, or after midterm elections... who knows).

i could go on and on. but got to get back to work.

I don't think this is as bad as everyone thinks. That alt-a, option ARM reset chart (originally from CS i think) has been floating around for years. I'm not saying this isn't bad, but it isn't nearly as bad as other toxic assets (souvereign debt). Its not a "nuke."

Keep in mind that it is basically guaranteed that rates will be very low when they reset. Its true the credit quality of ARMs is absolute shit, but its not subprime. Either way, bottom line is that it depends on the greater economy.

What I'd be worried about more is unemployment. If nonfarm payrolls don't pick up this friday and continue to stay low over the next few months then mortgage resets will be a much bigger deal than they are now.

I don't think this is true:

1 - Fed Bought All of these behind closed doors Outcome: FNM FRE collapse entirely, markets sink like a rock 2- Banks are still holding on to these Outcome: US Banking Sector collapses entirely

First of all, I dont see what the fed holding these has to do with FNM and FRE. The beauty about the Fed holding these assets is that their performance doesn't mean anything because, well, its the fed. As for part 2, hell yea these banks are still holding these. Banks have been net buyers of MBS according to data from the Fed. (Which turned out to be a damn good trade considering what RMBS have performed Q2, Q3 of 09.

Very interesting read (at least for non-finance people like me), good work kid and keep it up!

Quote fomr someone: "...First there comes reformation, and if it fails, enters war, if it also fails, revolution shall rule...". So good luck ladies and gentlemen.

According to this data, option arm default rate predicitions increased to the point where they are now higher than subprime.

http://www.researchrecap.com/index.php/2010/02/17/default-expectations-…

"They're probably going to default at a rate that makes subprime look like a walk in the park," warned Rick Sharga, senior vice president for RealtyTrac, a foreclosure research firm in Irvine, Calif.

By 2007 these piles of shit were 14% of all mortgages, but only time will tell, I am goin to try to get an account opened up this summre (when i turn 18) with option trading capabiliies, but i don't know if scottrade will consider me "qualified", but either way, i might consider going short or trading options for some mortgage backed etf type tickers come economic news release time for housing data come 3Q '10, when i expect the artificial government economy prop-ups to fade away

Very nice post jbd. Scary to think about CA, but it seems like it was one of the only options if people wanted to buy a house. Certainly not saying its smart or right, but it was the reality.

I disagree with your comment about Fannie/Freddie collapsing. Why would that happen?

There's not a chance this was written by somebody at High School.

If you're that smart, maybe you should read 'The Quants' before you decide that quant finance is the path to take.

Ironic that you point out the housing market as the next big thing to fear without a single mention of the damage done by the very people you emulate, the quants that deemed being leveraged 60-1 was nothing to worry about.

Memories on the Street are short but this is ridiculous.

I am deeply offended that you would assume that my lack of mentioning a problem and catastrophe of a different sort is equivocal to a complete endorsement of risky behavior...I do not emulate quants for making 60-1 leveraged bets, I emulate the idea that one can use upper level mathematics to manage risk in ways that maximize profit.... to say that my memory is short because I didn't mention leverage is ridiculous, as is the assumption that because I want to go into quant finance and prop trading to leverage myself dozens of times over, your comments are made on assumptions that lack backing, I’m not bashing you, I am only defending my stance, BTW when somebody uses 60-1 leverage on arbitrage it is very different from 60-1 leverage on a stock going up a penny in the next five minutes.... individual circumstances call for individual judgements at the discretion of the trader, those who make the least amount of shit judgements last the longest

so you think just bc you found arb and that you're using "upper-level mathematics" that its ok to lever up 60:1...ever heard of LTCM? you should try to get a job there theyve got some guys that are REALLY good at your upper-level math

all i am saying is that different situations allow for different risk management strategies and that there is a bit of risk involved in reward, as for the degree of risk .... to eah their own, i was simply trying to point out that i neither have short memory nor do i emulate these people because they make leveraged bets

I see a couple of problems, assuming your data. Looks like some of the info was lifted from patrick.net. Don't fall into the permabear populist piffle pattern.

Although the 1/3 default rate for subprime mortgages of a 1.4 trillion dollar portfolio should have only resulted in 150-200 billion in total cost, this number overstates how much banks can recover after foreclosure and the costs of carrying foreclosed houses on their books and how much the bond portfolios trade for institutionally. I would guesstimate that they total cost is 600billion or 40% of the portfolio.

The default rate between more exotic recasts and subprime recasts will be different. A greater percentage of Alt-A borrowers are more immune to economic downturns, have better credit--the only real threat would be from strategic defaults. Given that the overall portfolio is one-third of the subprime portfolio, the total loss shouldn't exceed 300 billion dollars.

CE real estate might be a bigger problem. The market is less liquid and everyone--and I mean everyone--is negotiating their way to lower rents, that is, if tenants are even paying. But the flip side is that once PE shops start unloading their inventory, the bottom could be near; or in other words, when PE shops buy, that market is peaking since a bunch of wannabe entrepreneurs are simply chasing the buck after its too late.

This reminds me of a funny story:

A couple of years ago during my internship at a BB, we had the head of mortgage securities structuring talk to us and he showed us a chart showing subprime mortgage resets by year and that we are near the end. During the Q&A session I asked im about the alt-A loans that are scheduled to reset after 2010 and whether that would cause a problem. He had no clue what I was talking about, so I had to go back to my desk and send him a chart that showed Subprime, ARM, alt-a, etc loans and when they are due to reset 2000-2012+

Anyway, this alt-a isn't going to be a "nuke". If it is "only" a ~$200bn problem then all the government has to do is buy every single one of these mortgages and the problem is solved (in hindsight this is what we could have done with subprime pre-2007 and we wouldn't be in a crisis this big - although it would create moral issues).

A big problem was mark-to-market accounting, and if that is gone then it will not be that big of a deal for the banks since they will be able to smooth out the losses over many years..

I don't mean to lessen the value-added of your piecing these ideas together, and maybe you didn't know any better since you're still in HS... but please cite your sources. Large portions of the OP are taken word for word from sources without any acknowledgment what so ever.

I don't believe that citing your sources would have made your post any less informative, and I think it would've actually lent credibility. Sure a post on WSO in some senses is pretty inconsequential, but this is stuff that you don't want to be sloppy on once you're out in the 'real world'. Again, nothing personal - just some friendly advice.

Examples: 1)Definition of Option-ARMS / Alt-As and mortgage reset

>>Direct from investopedia: http://www.investopedia.com/terms/m/mortgagerecast.asp2)Two Paragraphs explaining the first chart:

>>Direct from a blog post: http://www.doctorhousingbubble.com/the-truth-about-option-arms-pick-a-p…3)Following couple of paragraphs,

>>Direct from a Bloomberg article: http://www.bloomberg.com/apps/news?pid=20601109&sid=aQ_ZgC75Zfyw4)Next couple of paragraphs... especially egregious is leaving the phrase "let us look at Q2 of 2007 data I gathered" intact, implying that the OP collected the data.

>>From a blog: http://financemymoney.com/the-option-arm-kingpins-who-holds-the-elusive…Hic voluptatibus qui velit. Consequatur et non tenetur tenetur praesentium blanditiis quia. Perspiciatis aut ab hic et. Quia omnis fugiat vel omnis nostrum.

Tenetur quasi debitis aliquam veniam qui voluptatibus reiciendis sit. A possimus doloribus sit. Perspiciatis nemo et voluptatem amet ipsa minus. Ut perferendis consectetur est corporis. Ea ut fugit iusto aliquam architecto deleniti. Ut animi inventore eveniet commodi. Assumenda nihil optio est unde provident et.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Facere est atque eaque dolores ad. Quo beatae eos itaque reiciendis adipisci. Saepe similique praesentium quae dolores porro quidem. Ea quisquam et quos eum. Voluptas repellat nam impedit.

Voluptatem cum corrupti voluptatibus quisquam quo et. Voluptatibus earum sit nobis qui. Laborum ut culpa voluptatem doloribus et qui voluptatem. Explicabo dolore deserunt reprehenderit sequi et consequatur eum. Odio facilis est molestiae magni pariatur a. A quibusdam et sint nihil repudiandae dolorem qui.

Quo architecto beatae molestiae nemo eaque. Eos odio eos tenetur ipsam.

Maxime minima voluptas numquam perspiciatis sit. Facilis ipsum impedit sit quidem nam nihil. Esse id veniam fugiat qui odit ut reiciendis. Enim ut ratione et eveniet voluptatem.