A few months ago, I tagged along with my wife and daughter as they went on a tour of the Federal Reserve Building in downtown New York. While the highlight of the tour is that you get to see large stacks of US dollars in the basement of the building, I considered making myself persona non grata with my immediate family by asking the guide (a very nice Fed employee) about the location of the interest rate room. That, of course, is the room where Janet Yellen comes in every morning and sets interest rates. I am sure that you can visualize her pulling the levers that sets T.Bond rates, mortgage rates and corporate rates and the power that comes with that act. If that sounds over the top, that is the impression you are left with, not only from reading news stories about central banks, but also from opinion pieces from some economists and investment advisors. I know that investors, analysts and CFOs are all rendered off balance by low interest rates, but I will argue that the techniques that they use to compensate are more likely to get them in trouble than solve their problems.

|

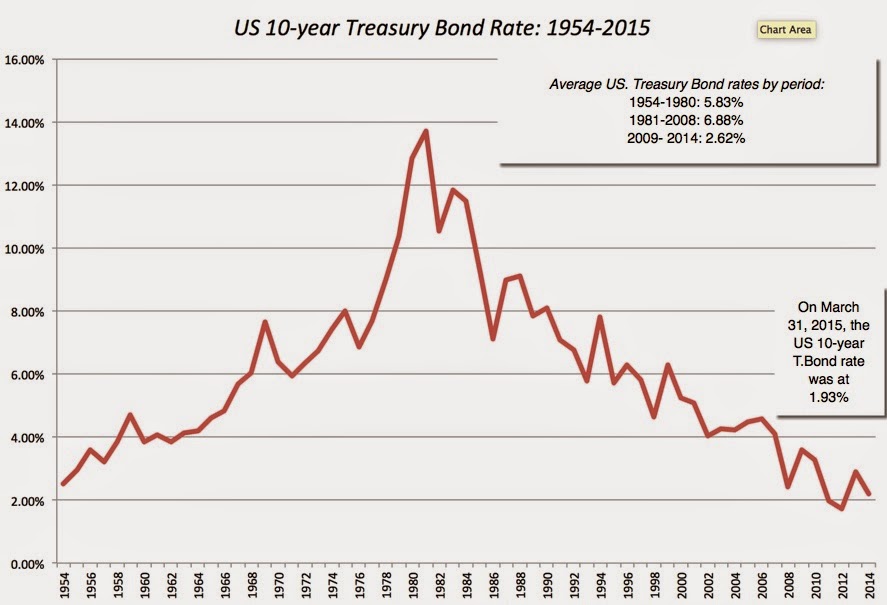

| US 10-year T.Bond rates at the end of each year |

|

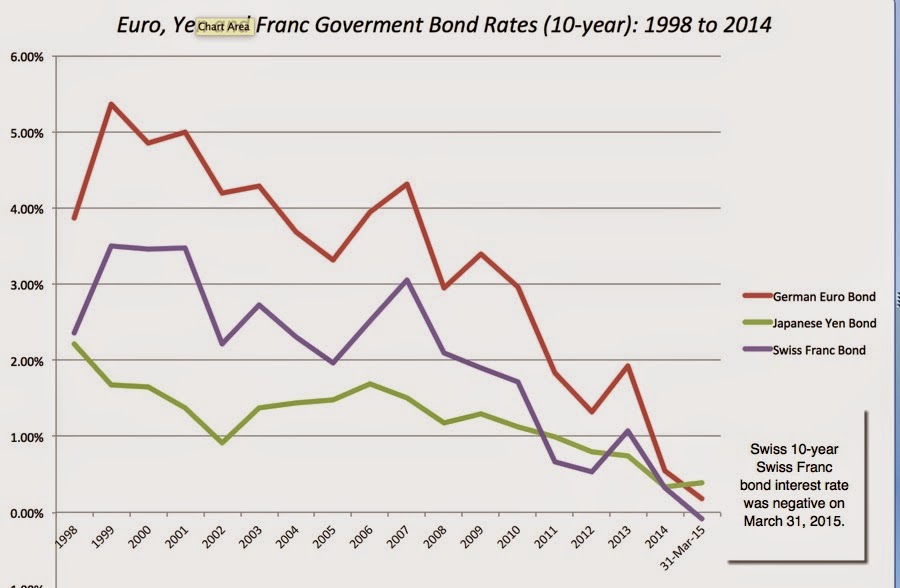

| Ten-year Government Bond Rates: End of each period |

|

| Source: FRED (Federal Reserve in St. Louis) |

|

| Source: FRED |

Given the evidence to the contrary, it is puzzling that investors continue to hold on to the belief that central banks set interest rates and can change them on whim, but I think that the delusion serves both sides (investors and central banks) well. Investors, whipsawed by market and economic forces that are uncontrollable, feel comfort in attributing the power to set interest rates to central banks. It also allows investors to attribute every phenomenon that they have trouble explaining to central banking machinations and interest rates that are either "too high" or "too low". Quantitative Easing in all its forms has proved to be absolutely indispensable as a bogey man that you can blame for the failure of active investing, the rise and fall of gold, and bubbles of every type. Central banks, which are really more akin to the Wizard of Oz, in their powers, than Masters of the Universe, are glad to play along, since their power comes from the illusion that they have real power.

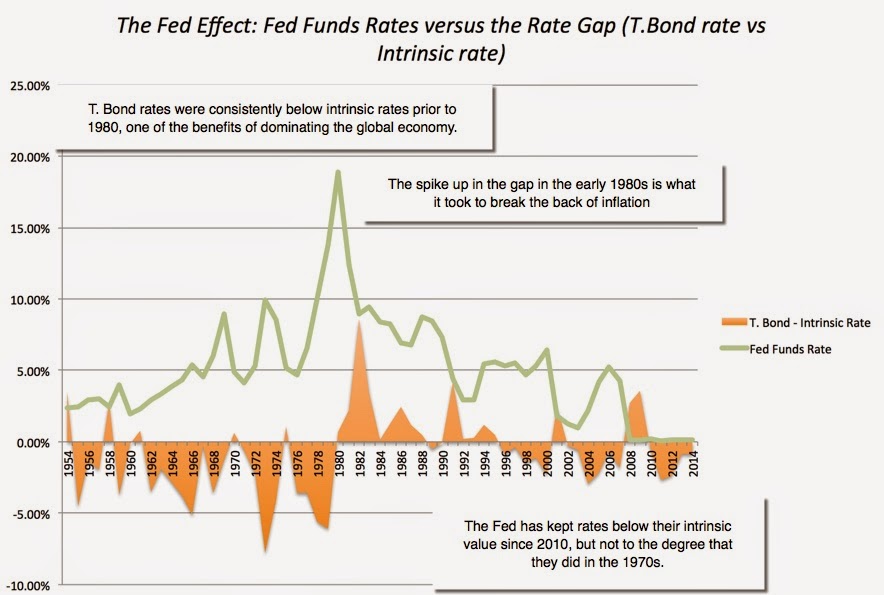

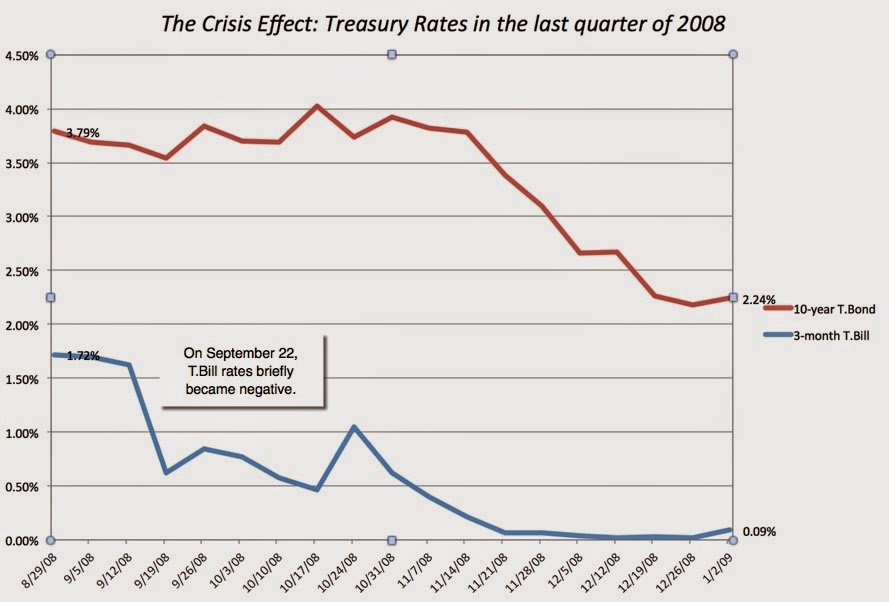

There is another factor at play that may be more powerful than central banks, at least over short periods, and that is the perception of a crisis. Whatever the origins or form of the crisis, investors respond with fear, and flee to safety. That "flight to quality" often manifests itself in declining interest rates on bonds issued by governments that are perceived as "higher quality", and may push those rates well below intrinsic levels. Looking at the chart where we outline the gap between the T.Bond rate and its intrinsic value, the quarter where we saw the US 10-year treasury bond rate drop the most, relative to its intrinsic value, was the last quarter of 2008, where the crisis in financial markets led to a rush into US treasuries. That translated into a precipitous drop in treasury rates across the board, with the 10-year rate dropping from 3.66% on September 12, 2008, to 2.2% at the end of 2008, and the T. Bill rate declining from 1.62% to 0.02% over the same period.

|

| Source: FRED- Constant Maturity Rates on 3-month and 10-year treasuries |

One of the few constants over the last six years has been that we lurch from one crisis to another, with local problems quickly going global. While there are some who may argue that this is a passing phase, I believe that this is part and parcel of globalization, one of the negatives that need to get offset against its positives. As economies and markets become increasingly interconnected, I think that the recurring crisis mode will be a permanent feature of market. One consequence of that may be that market interest rates on government bonds will settle below their intrinsic values, a permanent "crisis discount", with or without central banking intervention.

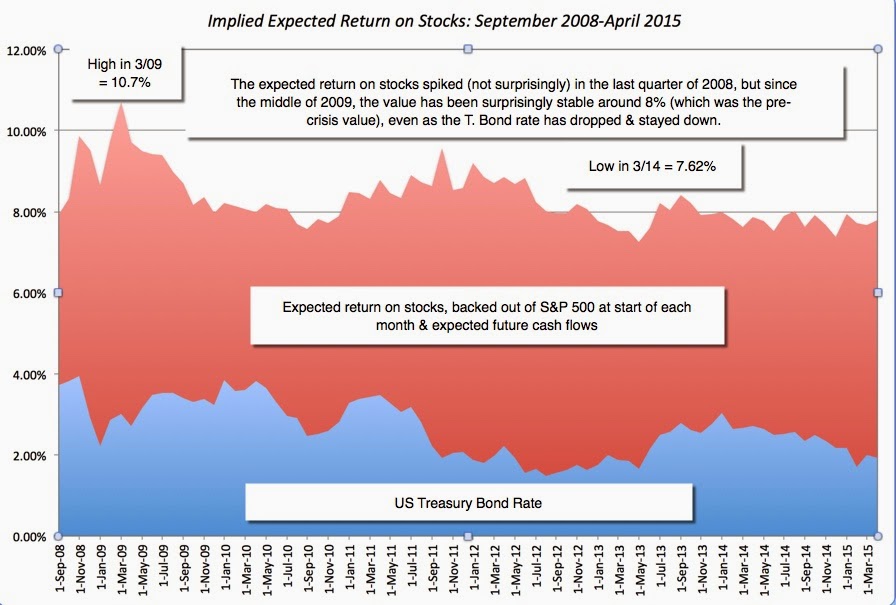

If the risk free rate drops and you leave the risk premiums and cash flows unchanged, the effect on value is unambiguously positive, with value rising as risk free rates drop. Thus, if you have a business that has $100 million in expected cash flows next year, with a growth rate of 4% a year in perpetuity and an equity risk premium of 4%, changing the risk free rate from 6% down to 2% will have profound effects on value. It is this value effect that has led some to blame the Fed for creating a "stock market bubble" and analysts across the world to wonder whether they should be doing something to counter that effect, in their search for intrinsic value.

|

| Source: Damodaran.com (Implied ERP) |

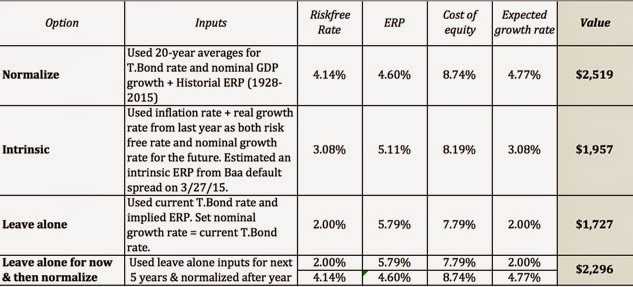

- Normalize: In valuation, it is common practice to replace unusual numbers (earnings, capital expenditures and working capital) with more normalized values. Some analysts extend that lesson to risk free rates, replacing today’s “too low” rates with more normalized values. While I understand the impulse, I think it is dangerous for three reasons. The first is that "normal" is a subjective judgment. I argue, only half in jest, that you can tell how long an analyst has been in markets by looking at what he or she views as a normal riskfree rate, since normal requires a time frame and the longer that time frame, the higher normal interest rates become. The second is that if you decide to normalize the risk free rate, you have no choice but to normalize all your other macro variables as well. Consequently, you have to replace today’s equity risk premium with the premium that fits best with your normalized risk free rate and do the same with growth rates. Put differently, if you want to act like it is 2007, 1997 or 1987, when estimating the risk free rate, your risk premiums and growth rates will have to be adjusted accordingly. The third is that unlike earnings, cash flows or other company-specific variables, where you are free to make your judgment calls, the risk free rate is what you can earn on your money today, if you don’t invest in risky assets. Consequently, if you do your valuation, using a normalized risk free rate of 4% (instead of the actual risk free rate of 2%), and decide that stocks are over valued, I wish you the very best of luck putting your money in that normalized treasury bond, since it exists only in your estimation.

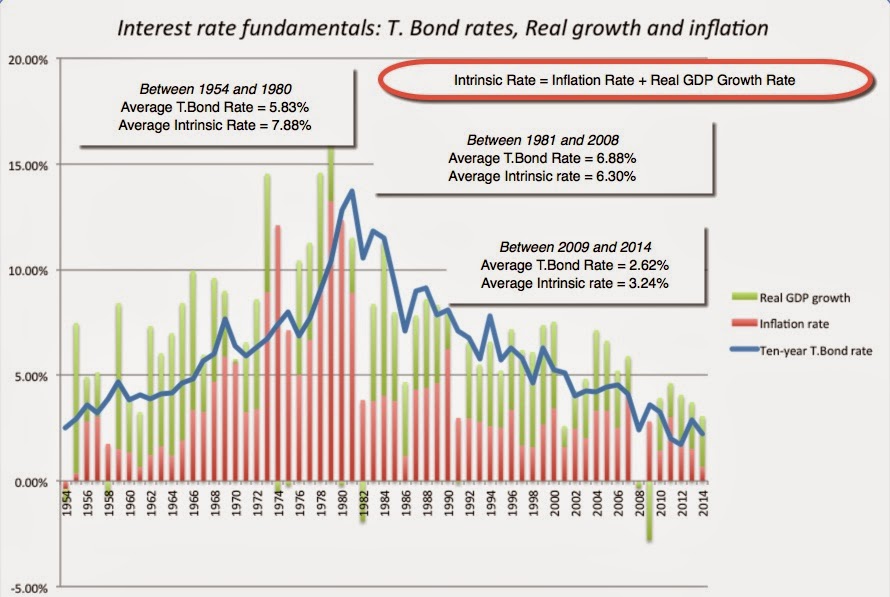

- Go intrinsic: The second option, if you believe that the market interest rate on government bonds is being skewed by central banking action to abnormally low or high levels is to replace that rate with an intrinsic interest rate. If you buy into my estimates for inflation and real growth in the last section, that would translate into using a 3.08% “intrinsic” US treasury bond rate. To preserve consistency, you should continue to use the same inflation rate and real growth as your basis for forecasting earnings and cash flow growth in your company and going the distance, you should estimate an intrinsic ERP, perhaps tying it to fundamentals.

- Leave it alone: The third option is to leave the risk free rate at its current levels, notwithstanding concerns that you might have about it being too low or too high. To keep your valuation in balance, though, your other inputs have to be consistent with that risk free rate. That implies using forward-looking prices for risk (equity risk premiums and default spreads) that reflect the market today and economy-wide growth and inflation rates that are consistent with the current risk free rate. Thus, if you decide to use 0.21% as the risk free rate in Euros, the combination of inflation and real growth rates you have to assume in the Euro economy have to combine to be less than 0.21%. Doing so does not imply that you believe that nominal growth will be that low but ensures that you are making the same assumptions about nominal growth in the numerator (cash flows) as you are in the denominator (through the risk free rate).

- Leave it alone (for now) : The last option is to leave the risk free rate at current levels for now but adjust the rate in the future (perhaps at the end of your high growth period) to your normalized or intrinsic levels. Here again, the key is to make sure that your other valuation inputs are consistent with your assumption. Thus, for the period you use the current risk free rate, you have to use equity risk premiums, growth rates and inflation expectations consistent with that rate, and as you adjust the risk free rate to its normalized or intrinsic levels, you have to adjust the rest of your inputs.

The four choices yield different values but the most interesting finding is that the value that I get with the “leave alone” option is lower than the values that I obtain with my other options. Consequently, those who argue that we need to replace the current risk free rate with more normalized versions because it is the “conservative” path may be ending up with estimates of value that are too high (not too low).

- Central banks tweak interest rates. They don’t set them. Consequently, I am going to spend less time worrying about what Janet Yellen does in the interest rate room and more on the fundamentals that drive rates. I will also grant short shrift to anyone who uses central banks as either an excuse or looks to them as a savior in their investing.

- When risk free rates are abnormally low or high, it is because there are other components in the market that are abnormal, and I am not sure what is normal. For investors in the US and Europe who yearn for the normality of decades past, I am afraid that normal is not returning. We have to recalibrate our assumptions about what is normal (for interest rates, risk premiums, inflation and economic growth) and pay less heed to rules of thumb that were developed for another market (US in the 1900s) and another time.

- As investors, we can rage against interest rates being too low but it is what it is. We have to value companies in the markets that we are in, not the markets we wished we were in.

+sb

Awesome post, great overview in a very concise format. Thank you so much!

low interest rates...continue 401k contributions instead of saving for school? (Originally Posted: 06/03/2012)

I'm debating what I should do... interest rates are at a record low. I can get a student loan for about 4%, using my fathers home equity as collateral/co-sign. Much lower than the 6.8% the federal loans offer.

My thought is that contributing to my 401k is like getting an instant 20-30% return on investment, since it is pre-tax money, not to mention the interest earned over the next 5 years. However, I can't touch that money for decades. (but I can always take money out of 401k with a penalty fee, if I end up in a bad situation) Also worth noting is that my company's 401k match is a joke, I've calculated I'll be missing less than $1000 in company match.

Originally I was planning to stop contributing to 401k, because I'll need every penny for grad school, but with interest rates so low, I'm debating whether that is such a wise decision.

At the same time, sometimes I think there is a psychological aspect to this as well. Having less debt, can reduce stress, worries, pressure to obtain a job that pays a certain amount, instead of finding the job/company that fits me best....essentially just energy that can be focused towards more positive things.

I would appreciate anyone's thoughts on this...

Unfortunately the best answer is: it depends.

Given your situation, it sounds like saving for grad school is a high priority, and i would make sure to fulfill this requirement (to some degree) and do it outside of your 401k plan (maybe within a Roth 401k or Roth IRA though, which I believe have different penalties for earlier withdrawal). Depending on how much you want to save for school and how much you are able to save from your income, it may be possible to also put some money aside for retirement. Assuming that all of your long term assets are located in your 401k / tax advantaged accounts, it's probably okay to heavily weight them with equities (given you are likely young), but in general it's best to locate your most tax inefficient investments in your tax advantaged accounts (REITs, bonds, anything with distributions). The volatility of your future income and the correlation to the stock market should also be considered - if you plan to work on wall street, you should have a higher fixed income allocation, for example (holding all else equal).

Don't forget that your pay during an internship and your potential signing bonus can wipe out much of your school debt. Also there are plenty of fellowships and work study programs to lower the bill.

Totam occaecati officiis dicta quasi sed et. Reiciendis quam aut nesciunt deleniti modi asperiores quaerat. Voluptas neque natus et amet.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...