The Chinese economy made headlines last week when updated data by the IMF reflected that the Chinese economy ranked number one in terms of Purchasing Power Parity. Historically, the now ‘emerging nations’ had dominated the global GDP scene. The onset of the industrial revolution was the watershed moment for the now ‘advanced economies’. US in particular was most successful in harnessing disproportionate gains from this paradigm shift and emerging as a world leader in terms of GDP. The recent decade witnessed ‘catching up’ by the emerging economies with China as the strongest player. In terms of per capita income however the Chinese economy has a long way to go – currently ranking 93rd in the world (out of 199 countries).

The image has been sourced from the article published by: The Economist.

The last couple of decades witnessed China move ahead exploiting the idea of export fueled growth supported by cheap labor costs and declining transportation costs. Consequently, exports soared from 16% of GDP in mid-nineties to ~27% in 2008. One of the major consequences of higher exports was large accumulation savings and eventually translating into dollar denominated debt. As of July 2014, China accounts for 21.09% of the $5.1 trillion dollars of US debt owned by foreign governments.

The accumulation of dollar denominated debt played its controversial part in currency manipulation whereby Chinese exports maintain competitive advantage despite rising demand. In the recent past the Chinese government has faced criticism owing to maintaining an undervalued Chinese Yuan.

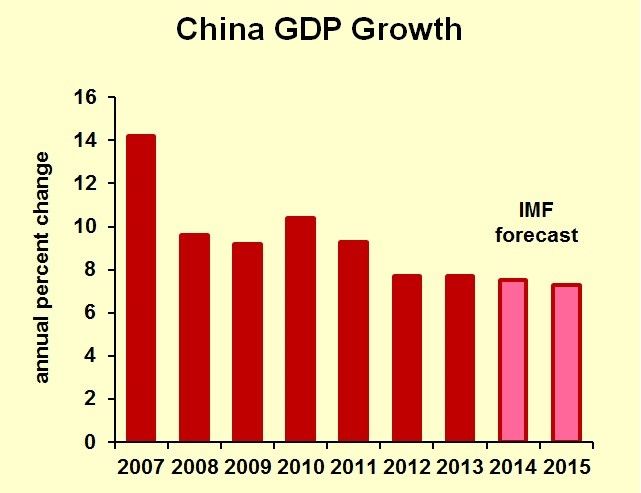

Post the crisis however, the growth story slowed down as we know with current GDP forecast being somewhere between 7.1 and 7.3%, as opposed to >10% growth in 2007. The export share of GDP however continues to remain stable at about ~26.4%.

The image has been sourced from article from Forbes magazine.

Despite recording strongest GDP growth numbers among the BRICs nations (Brazil: 0.3% Russia: 0.2%, India: 5.6%) the growth estimate is modest and indicative of the slowest year on year expansion since 2009.The slowdown has mostly been triggered by sluggish movement in the property and real estate department. The Chinese government has also started focusing attention on much needed infrastructure development accompanied with loosening monetary policy and stimulating domestic demand. This is particularly well timed since economic activity in the rest of the world particularly the Euro is witnessing sluggish recovery.

At this juncture, it is important for the Chinese economy to focus on productivity gains to sustain longer term growth as much of the GDP expansion that the country witnessed has been attributed to larger employment of labor and capital. Thus, underscoring the importance of infrastructure investment and development.

The major short term challenges ahead if the Chinese economy comprise of transitioning from export led growth to greater emphasis on stimulating domestic demand as incomes rise. Environmental factors also contribute to the short term slump as shift to a clean iron ore and coal technology is time consuming. Finally, political scenario in Beijing calls for a much needed re-vamp and move away from excessive state and bureaucratic intervention.

The IMF points out that despite of these short run concerns which most likely will lead to a temporary deceleration, the Chinese economy is on a robust long term growth trajectory.

So what are your thoughts?

The content for the blog has been sourced using:

U.S. National Debt Clock October 2014 , China offers hint of growth prospects, Germany expects more bad news , China Economic Forecast 2014 - 2015: Rocky Growth , When giants slow down , Unproductive production , China’s back , RECENT DEVELOPMENTS, PROSPECTS, AND POLICY PRIORITIES

Great post, that chart from the economist is super interesting. I say Chinese economy will continue to grow, possible real estate bubbles, decline in manufacturing, and export-centric to consumer-oriented transitions all withstanding.

To me the big question is if their semi-centralized state run model will work. On the bright side, they seem interested in partnering with Russia as being their main energy import (steering them away from former Western partners, maybe why Russia felt so bold taking over Chechyna, forget Germany, they have China now) as well as trying to position the Yuan as a competing reserve currency in the future against the U.S. $. They have a lot of investments in Africa and the Middle East (which is particularly embarrassing for us since we went to war for that oil http://www.nytimes.com/2013/06/03/world/middleeast/china-reaps-biggest-…), which might all pay off big time.

On the other hand, they'll get hit hard if N. Korea's regime ever implodes, there's a huge potential for political instability (already happening in Hong Kong), environmental concerns (all the concerns you mentioned in your post), and I think popular perception is that U.S. is still a better place to live. The U.S. higher education system is a huge brain drain for Chinese talent, and it's been my personal experience that a lot of them stick around here. I don't have data to back that up though. I was in Beijing back in 2008 and to be honest, I thought it was a pretty miserable place to live. Smog, crowded, I didn't see the sun for days because of all the pollution. There are a lot of other really beautiful places in China though, and that was admittedly 6 years ago, a very long time for a dynamic economy like China.

Personally I hope China and U.S. will be able to work together and harness each other's powers to lead the global economy, instead of fighting each other and getting stuck at a lower Nash equilibrium so to speak. Americans and Chinese can do great things together but there's also inevitably the suspicion and mistrust that one will fuck over the other.

@"bkzen"

-Definitely a trendIf this ever happens we are talking 25+ years away. There is no real short term implications here.

Zero chance.

Voluptates dicta magnam nemo quia. Inventore harum earum blanditiis.

Aut alias veniam recusandae aliquid ea. Sunt quis ut at qui sed. Rem voluptatibus ut possimus praesentium. Aut quas doloribus dolorum. Ad autem aperiam et dicta dolores itaque iste.

Suscipit quibusdam explicabo non quia totam sunt rerum. Rerum accusamus sit dolores dolorem voluptatem. Odio omnis blanditiis sed iusto unde rerum. Hic possimus neque sit quisquam non eius.

Deleniti cumque et rerum id ducimus dolores. Natus delectus ad omnis at sit quia. Porro tempore consequatur ad impedit quo autem.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...