Institutional Capital Allocation: Decoding the Macro Shift Through Regulatory Disclosures

As the broader market absorbs ongoing macroeconomic headwinds and shifting interest rate expectations, analyzing the structural repositioning of institutional capital provides a more grounded perspective than daily price action. Instead of relying on market sentiment, observing the mandated quarterly disclosures offers an empirical look at how major funds are managing risk and liquidity in a high-variance environment.

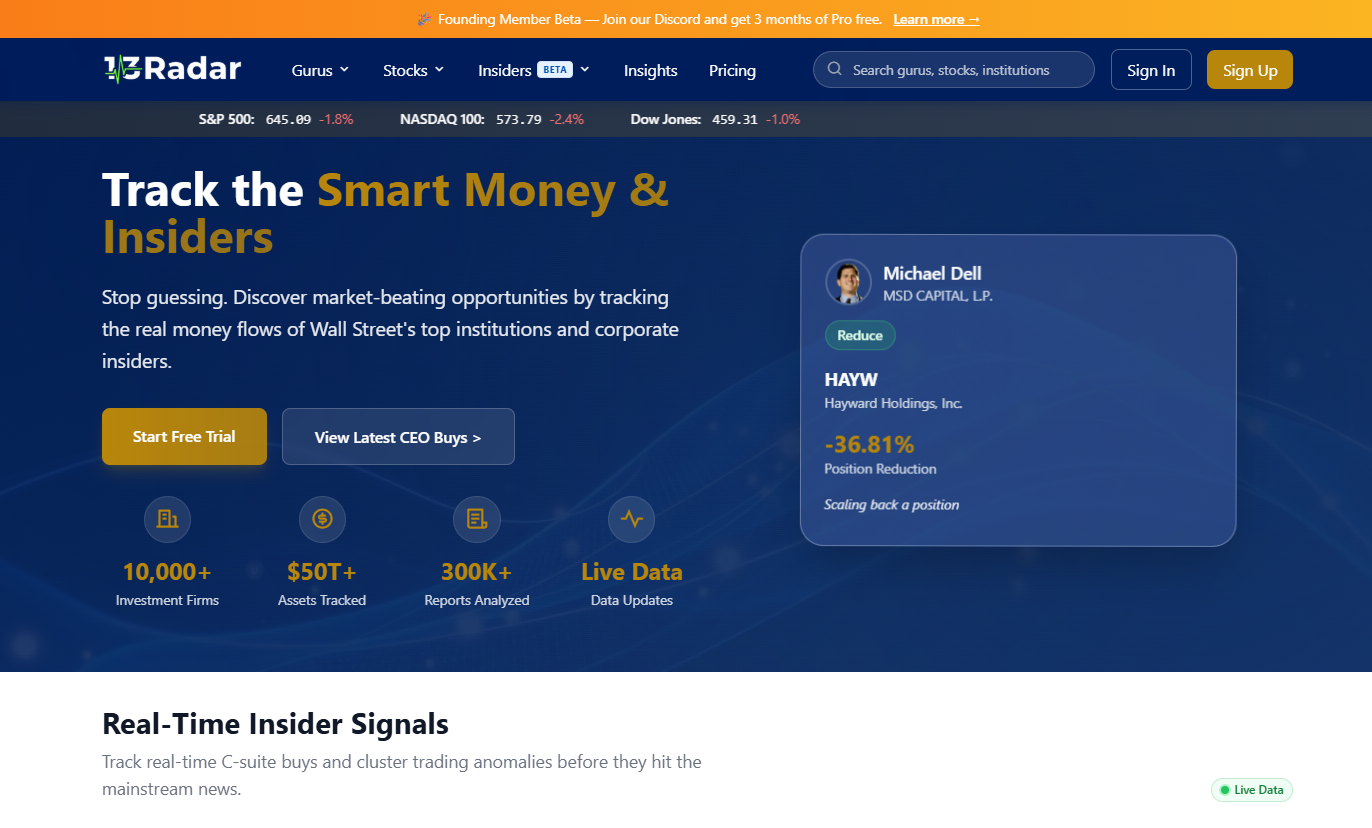

Analyzing the Berkshire and Scion Disclosures

A review of recent activity from established capital allocators reveals a distinct preference for defensive posturing over aggressive growth. For example, Warren Buffett’s Berkshire Hathaway has systematically reduced long-held equity positions, notably trimming exposure in the technology sector, while accumulating a historically significant cash reserve. This accumulation of liquidity suggests a broader institutional consensus that current market valuations may not fully price in upcoming economic friction. Simultaneously, funds like Michael Burry’s Scion Asset Management have demonstrated highly concentrated allocations, focusing on asymmetrical bets rather than broad index participation.

🔥 SECTOR ROTATION: Examining the Tech to Value Transition 🔥

The institutional data points toward a quantifiable rotation rather than a pure liquidation event. We are observing a reallocation of capital moving out of overextended mega-cap technology equities and shifting toward defensive, cash-generating value sectors. Understanding the mechanics of this sector rotation is critical for accurately modeling current market dynamics. While retail volume often concentrates on speculative growth names during volatile periods, aggregate fund behavior indicates a sustained accumulation of fundamentally sound, lower-beta assets designed to withstand prolonged economic pressure.

The Utility of Regulatory Data in Macro Analysis

Tracking these capital shifts requires relying on raw regulatory data rather than secondary commentary. Under U.S. securities law, institutional investment managers overseeing more than $100 million in qualifying assets are obligated to disclose their U.S. equity holdings on a quarterly basis. By analyzing the aggregated sec 13f filings, analysts can identify sector-level trends and cross-reference them with broader macroeconomic models. This standardized reporting mechanism remains one of the few objective tools available for reverse-engineering the risk appetite of the largest participants in the financial system.