Most commodity markets tend to be driven by a few basic factors which are freight on one side, price on the other side and qualities.

Each commodity market has its own particularities. Most of what I will generally talk about applies to oil and the liquids in particular which is a little bit different from the gas market. Why ? Why is the gas market different from the oil market ?-** The Logistics are different. **

Transport is one part of the logistics chain but the logistics chain involves everything that happens from once you get the basic commodity out of the ground. When it’s natural gas, you have to treat it differently as it comes out of the field, you need different type of containments and operators. It’s slightly more complicated because natural gas tends to move by pipeline, oil moves in a big bucket.

Why oil does get traded ? What is the utility of people in Physical Commodity Trading? The basic question about why does oil get traded, because you could imagine a scenario where a producer like Chevron, BP, Saudi Aramco, Conoco Phillips, Hess, Suncor … whoever pulls it off the ground, and then does every single step itself to end up selling gasoline in its own branded gas stations. In the real world it doesn’t happen that way.

When you go at Shell gas station in your town or you when you buy heating oil from CITGO for your heating system at home, you may be buying a branded CITGO product but most of the time that product wasn’t produced in a CITGO refinery. It was maybe produced in a P66 refinery, it was produced at the IRVING OIL or maybe produced in a European refinery (although Europe tends to import more than to export). Just because it’s written Shell, BP, P66 or Exxonmobil on the gas station sign doesn’t mean that the gasoline is actually produced by them.

There are a number of continued imbalances in the market that continually need to be re-balanced. Energy traders are the experts at optimizing the logistics from the well head to the gas pump. Their main role is to identify discrepancies and then re-balance markets. So what do you think is the primary factor to identify imbalances ?**- It’s prices. **

Prices are magic; if there is not enough of something, price goes up. If there is too much of something, price goes down. Anytime you are going to listen so-called experts in the commodity market who tend to be self-appointed experts, especially when it comes to regulations, is sophisticated arguments to explain to you why this and that and why that needs to be regulated. Sometimes they have good arguments; sometimes they have less good arguments.

In general, when you regulate something, what you end up to do is putting impediments to the functions of market dynamics. e.g what you really do is that you skew the functioning of commodity pricing. Pricing is what makes commodity move. Oil is always moving on the way down, it never moves on the way up. It’s simple; it’s a law of physics, gravity. The only thing that is 100% reliable in the world is gravity. It’s the only thing in this world that is an hundred percent right. The other thing is pricing. Prices mechanisms are an hundred percent right.

Price rises ?

Somewhere in the world, some genius is going to figure out “how to get stuff” to a high price place.** Price falls ?**some genius will figure out “how to take it low” and bring it to a high price place. Why does crude oil has to move around the world ? The very first reason is that it’s a naturally imbalanced market. What happens is that parts of the world have various amounts of crude oil and some other places produce zero crude oil. Regions, countries consume various amount of energy. Imbalances are also located inside countries.

Canada, one of the world’s largest crude oil producer, has the production concentrated in its western provinces (AB, SK) while its eastern parts (Ontario and Quebec) produce zero crude oil and need this energy to fuel their economy. In China has a massive deficit while in places like the Middle-East, Russia have a surplus of energy.

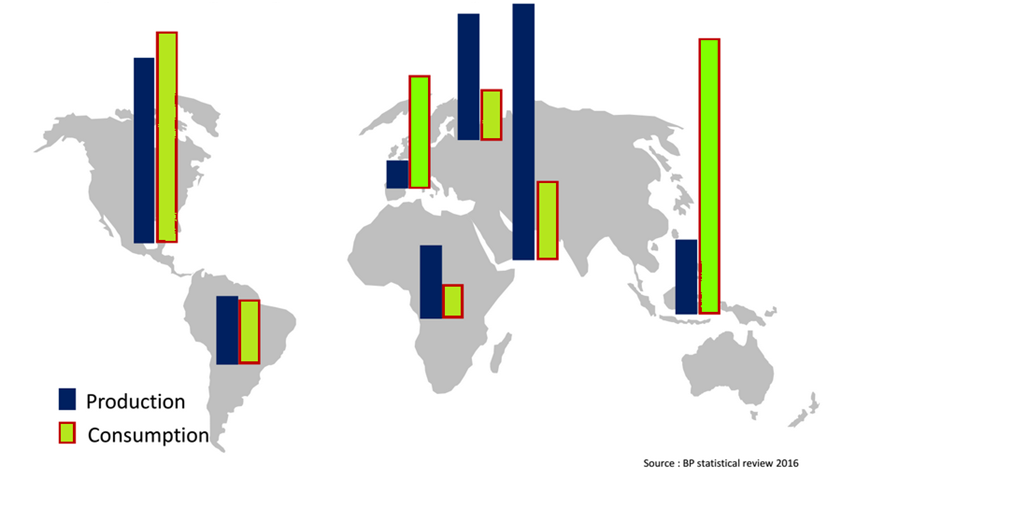

In America, relatively speaking, the market seems balanced but the consumption profile is different from Europe (more light ends).

[See the Image Attachment]

If I show you this chart in 5 years from now, I guarantee it will look differently. The market changes all the time. It is increasingly dynamic; 10 years ago, the North-Sea (Denmark, Norway, UK, Netherlands) were big producers of crude oil. Brent was the crude standard bearer of the U.S Atlantic Coast and Eastern Canadian refiner. The primary refining capacity for the U.S and Canadian market has been built for the Brent (quality) but a lot of that has disappeared now.

The supply doesn’t match geographical demand and the crude qualities rarely correspond to the requirement of the local refinery. You can immediately see why these commodities need to flow.

With quality, you have different crude prices. When we talk about heavy crude, generally speaking, the heavier they are, the more sulfur they have and the more impurities and noxious substances they contain. They also tend to be harder to refine.

The heavier a crude is and the more sulfur, the more you need processing to make it into usable products. This tends to trade at bigger discounts. The processing costs of these high sulfur heavy crude cost more than the light sweet crude. In order to maximize the value you need to optimize these crude.

A 5%S heavy Cuban crude (5% sulfur) will trade at a discount of somewhere between 10 or 20 dollars a barrel below some of the Venezuelan crude discounted between 10 -20 dollars to the Brent reference price on a FOB vessel. Some of the crude oil are traded at a premium to the Brent reference price, so again it’s a question of price is going to buy different crude.

If you invested 10B$ in a refinery, you will want to buy a lot of these heavy things with a lot of discounts because you invested a lot of money in building this complex refinery. If you invested no money at all and simply owned a simple distillation refinery, you will be quite happy to pay a premium to Brent, extracting the gasoline out of this grade.

There is a large matrix of sourcing possibilities. As an example, a refiner like MARATHON trades 30 to 50 grades on a regular basis.

LITASCO, a pure energy trader, makes a market for at least 50 to 70 crude on a regular basis. Each crude has its own specifications; its transportation and its location are directing the commodity trading.

Transportation.

Obviously each mode of transport offers its inherent risks and benefits and carries a cost to bear for it. The industry will carefully balance these two variables and chose how to move those molecules at the lowest cost possible with the lowest risk. Pipelines are by far offer the most secure and lowest cost possible option for their continuous flow, followed by tankers for the larger capacity and then by rail, barges and trucks. In some places like Saudi Arabia, “it’s very simple”, TOTAL shows up with a VLCC, they accept their vessel (provided that it is aged less than 15 years, has no any maritime liens…) . The vessel loads 2 million barrels in its holds and it takes about 60 hours of loading. There are never complications (such ice, weather etc) and the logistics is straightforward.

When KOCH loads Western-Canadian Crude in Vancouver, they nominate the oil into the Kinder Morgan pipeline between Edmonton and Burnaby (Buys the line capacity from a regular shipper), schedules a smaller vessel because of the draft limitation, sail through Panama to reach the Gulf Coast. KOCH will possibly transload two cargoes (Aframax) into a larger vessel (Suezmax). The logistics are incredibly complicated because this oil is produced landlocked in the northern part of Alberta or Saskatchewan and the trader has to take it from the oil sands production area, mix with diluent to make it transportable in a pipeline.

The location, the quality, the logistics define the price of the crude.

The Albertan crude has a different yield of kerosene, asphalt, light products and a different price (discounted between 30 and 45% below the WTI reference). Because of these price discounts, there is also sometimes blending possibilities also because of a particular customer likes a yield that is richer in intermediate and heavier products. It implies that a crude slate with its inherent characteristics is carefully balances before entering the refinery units so the processing margins are obtained at an optimum cost. This will also depend of the timing and the availability of the qualities on the market because most of the time, believe it or not, all refiner customers are very timing-sensitive.

Time is money.

Why is it so ? First you never ever want to have an unit running out of crude but what’s the second and main reason ?

The second reason is about time of working capital. Have you hear about something called just-in-time ? Crude oil is currently traded in the $50 per barrel handle. A 350Kbbl per day refinery @ 90% utilization rate requires excessive amounts of cash to be operated. You can figure that there is never excessive cash and that it is highly inefficient to hold more than 10-day production coverage (unless there is sizable economic justification in the term-structure). Part of the energy trader job is to be “on-specs”, “on-time” and provide the best price(lower). Those are the three daily functions that matters the most. Refiners don’t want nice guys, they want “on-specs”, “on-time” and best prices.

This should be good pointers for those who are interested about the Energy and Commodities path.

I have a last question for you: How do energy traders optimize of the stream value with the physical and logistics assets with these imbalances to capture the P/L and what can go wrong ?

In the part II of this contribution on WSO I will discuss on the imbalances and risk-arbitrages in the physical energy market.

For now, I will wait for your reactions and/or questions.

| Attachment | Size |

|---|---|

| BP world Production/Demand 70.09 KB | 70.09 KB |

{kind=link}

{kind=link}

Physical Energy Trading And Logistics Part II

In the part II of this contribution on WSO I will discuss an imbalances & risk-arbitrages in the physical energy market. How do energy traders optimize of the flow the physical and logistics assets/contracts with these imbalances to capture the P/L and what can go wrong ? (Risk)

This example is partly inspired by Fletcher J Sturm (1997) Trading Natural Gas: Cash Futures Options & Swaps. If you don't already have this book, get a copy of it.

It also inspired by Off-Exchange EFP cash settlement & buying/selling that I've done as a trader on another pipeline.

For the sake of simplicity, please allow me to relax some assumptions ( no bid-offer spread, the current market prices are obviously different). I also assume that illiquid physical markets aren't fixed by 5 or 6 traders.

Background: NGPL is the largest transporter of natural gas into the high-demand Chicago market and one of the largest interstate pipeline systems in the country.

Goldman Sachs has currently firm pipeline transport capacity on NGPL from from Katy, Texas to the Exxon Mobil refinery in Joliet, Il (delivery point). see attachment.![]() https://www.google.ca/search?q=ngpl&biw=960&bih=486&source=lnms&tbm=isc…</a" alt="NGPL" /> Is the Bank short or long the basis spread ?

The Bank analyst sees an imbalance in the supply and expects the spread between South Texas and Chicago to widen, essentially will they buy or sell the spread ?

https://www.google.ca/search?q=ngpl&biw=960&bih=486&source=lnms&tbm=isc…</a" alt="NGPL" /> Is the Bank short or long the basis spread ?

The Bank analyst sees an imbalance in the supply and expects the spread between South Texas and Chicago to widen, essentially will they buy or sell the spread ?

Transportation costs

• A demand charge, which recovers a portion of fixed costs, is paid on all contracted volumes, regardless of the amount of gas actually purchased.

• The commodity charge, which covers remaining costs and all variable costs, is paid only for volumes of gas actually sold. • The demand charge on NGPL is $0,23/MMBTU and the commodity charge is $0,28/MMBTU.

• The bank owns firm pipeline transport capacity on NGPL and now expect the South Texas/Chicago basis spread to narrow

The index for Katy, (South Texas) is $4.05/mmbtu, The index for Joliet, IL (Chicago) is at $4,45/MMBTU. Prevously, GS has hedged the basis spread at $0,46/MMBTU.

'A trader question to his analyst' What is my all-in cost to pipe the South Texas gas to Joliet ?

The index for South Texas is now $4.25/mmbtu while Chicago is at $4,00/MMBTU. 'A Risk question' What has gone wrong ?

'A trader accountant question': What is the unrealized P/L for the Goldman Sachs ?

Let's crunch numbers and discuss the possible answers.