Real Estate Development Model

Refers to analyzing a property from the perspective of an Investor and deciding whether to invest or not based on the risks and potential returns.

To begin, 'real estate' is defined as land and buildings that generate revenue or have the potential to do so.

In this article, we will concentrate on commercial real estate (CRE) that is purchased and then rented out to individuals or businesses, as opposed to residential real estate, such as single-family homes, that is owner-occupied and not rented out.

Individuals or businesses, known as tenants, pay rent to property owners to use their space.

The rent provides income to the owners, who use a portion of it to cover expenses such as utilities, property taxes, and insurance; in some cases, tenants are also responsible for a portion of these costs.

All of this leads us to the following definition of Real Estate Financial Modeling (aka REFM):

In real estate financial modeling (REFM), you analyze a property from the perspective of an Equity Investor (owner) or Debt Investor (lender) and decide whether or not the Equity or Debt Investor should invest based on the risks and potential returns.

For example, if you buy a multifamily property (i.e., an apartment building) for $50 million and hold it for five years, could you earn a 12% annualized return?

Could you, for example, develop a new office building by spending $100 million on land and construction, find tenants, lease out the property, sell it, and earn a 20% annualized return?

Real estate financial modeling can help you answer these questions by identifying the most important assumptions and correctly setting up your analysis.

Because all investing is probabilistic, a simple model cannot tell whether a property will generate an annualized return of 11.2% or 13.5%.

A good analysis, however, can tell you whether that range of returns – 10% to 15% – is plausible. These are the questions that real estate private equity firms spend their entire day debating before making investment decisions.

-

Real Estate Financial Modeling (REFM) involves analyzing a property from the perspective of an Equity Investor or Debt Investor to determine whether the investment is viable based on risks and potential returns.

-

There are three main strategies/types in real estate financial modeling: Core (stabilized property), Value-Added (renovations), and Opportunistic (development or redevelopment).

-

A real estate development model includes a Deal Summary and Cash Flow Model. The Deal Summary lists key assumptions, while the Cash Flow Model calculates revenues, expenses, funding costs, capital repayment proceeds, IRR, and leveraged free cash flows.

-

Real estate development models provide a holistic view of a project's financial performance, essential for informed decision-making in real estate investments.

Real Estate Financial Modeling Types

Real estate combines equities and fixed income elements and can provide a risk/return profile that falls in the middle.

A Core real estate transaction in which a firm acquires a stabilized property, makes minor changes, and then resells it, for example, may offer risk and potential returns comparable to those of an investment-grade corporate bond.

A Value-Added transaction, in which a firm acquires property with a low occupancy rate, makes significant renovations to improve it, and intends to sell the property for a significantly higher price. On the other hand, this may offer risk and potential returns similar to those of stocks.

An Opportunistic transaction in which a company builds a new property from the ground up ("development") or ultimately converts or rebuilds an existing one ("redevelopment") may carry an even higher risk than stocks but also higher potential returns.

These descriptions highlight the three main real estate financial modeling strategies and types:

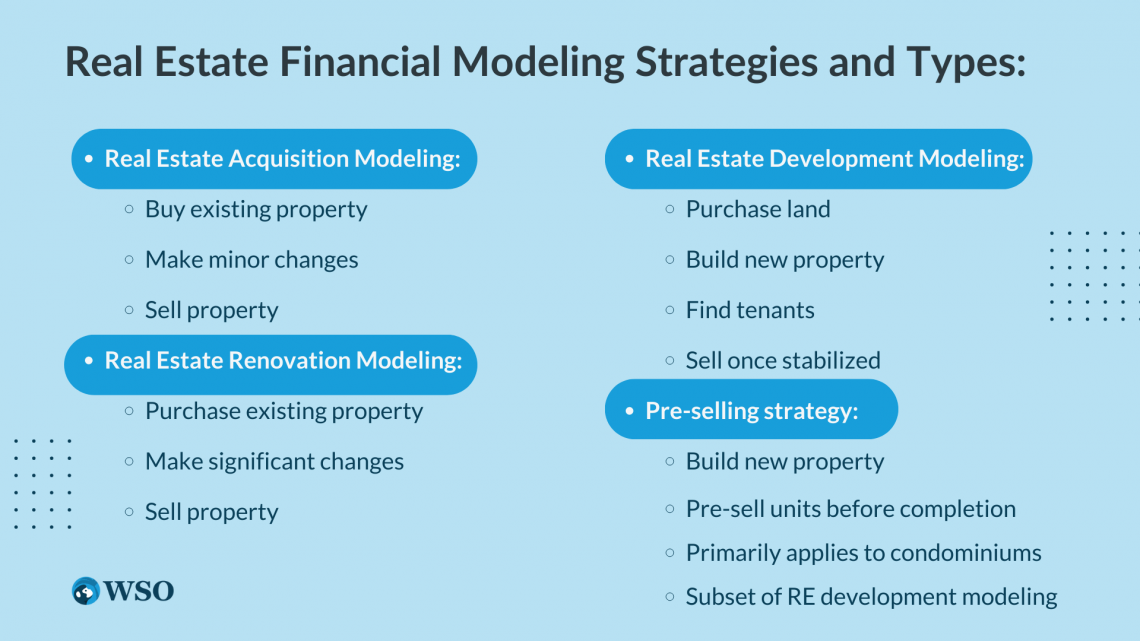

- Real Estate Acquisition Modeling: Buy an existing property, make minor changes, and sell it.

- Real Estate Renovation Modeling: Purchase an existing property, make significant changes, and sell it.

- Real Estate Development Modeling: Purchase land, build a new property, find tenants, and sell once stabilized.

- There is a fourth strategy: build a new property but pre-sell units before completion rather than leasing and selling the entire property at the end.

This is a subset of real estate development modeling, and it primarily applies to condominiums (residential real estate).

What is the definition of a Real Estate Development Model?

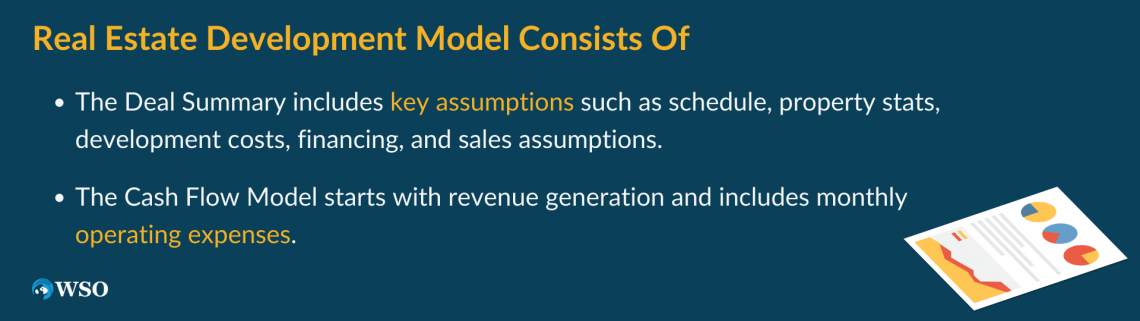

A typical real estate development model is divided into two sections:

- Deal Summary

- Cash Flow Model

All important assumptions are listed in the Deal Summary, including the schedule (which lays out the timeline), property statistics, development costs, financing assumptions, and sales assumptions, and are used to calculate the economics and profitability Index.

The Profitability Index (PI) is a ratio that calculates the present value of future cash flows versus the initial investment. The index is a component of the project.

The Cash Flow Model begins with revenue generation, followed by monthly operating expenses. An operating budget is a set of revenues and expenditures for a specific period, usually a quarter or a year, that a company uses to plan its operations.

When performing financial analysis in Excel, the monthly budgeting template has a column for each month and totals to be the full year annual figures, financing, and finally levered free cash flows, NPV (net present value), and NPV formula guide to the NPV formula.

It is critical to understand how the NPV formula in Excel works and the math behind it.

NPV = F / [(1 + r)n],

Where,

PV = Present Value,

F = Future payment (cash flow),

r = Discount rate,

n = number of future periods,

IRR (internal rate of return) of the project.

In the following sections, we will discuss the key steps to creating a well-organized real estate development model.

1. Deal summary

a) Property Statistics and Schedule:

The first step in developing a real estate development model is to fill in the schedule and property statistics assumptions. The following items should be included:

- Schedule:

- Transaction date.

- Sales Start Date.

- Construction Start Date.

- Construction End Date.

- Transaction Month Date.

- Sale Commencement Date.

- Units Sold/Month.

- Completion of Construction Closed.

- Units Closed Per Month.

- Property State:

- Gross Site Area.

- Deductions.

- Net Site Area.

- Density (FSR).

- Number of Units.

- Construction GBA.

- Net Salable.

- Average Unit Size.

b) Costs of Development:

The next step in developing a real estate development model will be to enter the assumptions for development costs in terms of the total amount, cost per unit, and cost per square foot.

Development costs include land costs, building costs, servicing, hard and soft contingencies, marketing, etc. We can calculate the numbers and complete the development costs section using the property statistics we filled out earlier.

c) Sales Predictions:

We will calculate the total revenue from this project in sales assumptions. Assume that market research has been conducted and that, based on comparables, we believe that $500 per square foot is a reasonable starting point for the sales price.

We will then use this as a revenue generator. We can calculate the net proceeds from this project by calculating sales (total, $/unit, $/SF), sales commissions (e.g., 50%), and warranty.

d) Assumptions Regarding Financing:

There are three critical assumptions for financing: loan-to-cost percentage, interest rate, and land loan.

Before calculating the total loan amount, we must first determine the total development cost. Because we haven't figured out the interest expense yet, we can link the cell to the cash flow model for the time being and get the value once the cash flow model is completed.

The commissions are the same as those described in the section on sales assumptions. The total development costs are as follows:

Total Development Cost = Land Cost + Development Cost + Interest and Commissions Added Together

We can now fill in the remaining financing assumptions.

- The maximum loan amount obtained for this project is equal to the total development cost multiplied by the loan-to-cost percentage.

- Total Development Cost – Maximum Loan Amount = Equity

2. Cash Flow Model

a) Increased Revenue:

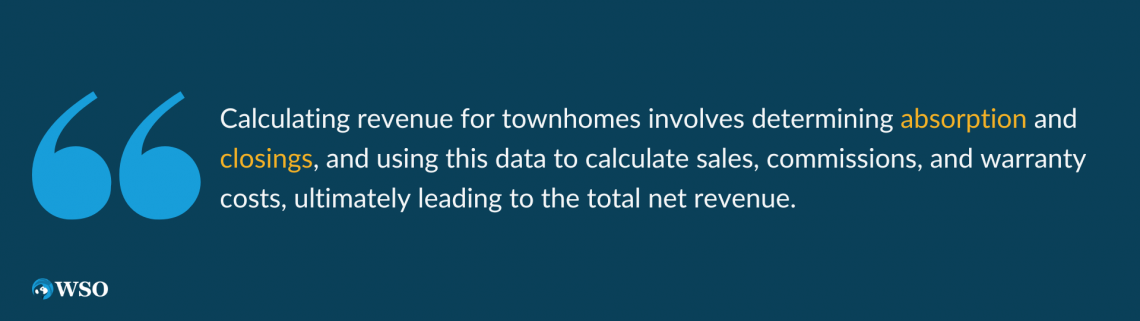

The first step in calculating revenues is determining townhomes' absorption and closings. The number of available homes sold during a given period is referred to as absorption. In contrast, the number of homes closed once construction is completed is called closings.

Using the absorption and closing data, we can now calculate revenue.

- Sales of townhomes = Sales Price/Unit x Townhome Closings

- First 50% commissions (charged when homes are sold) = Townhome absorption x Sales Price/Unit x (Commission % /2)

- Second, fifty percent commissions (charged when homes are closed) =Townhome closings x Sales Price/Unit x (Commission % /2)

- Warranty = Warranty cost per unit x Townhome closings

- Total Net Revenue = SUM(Townhome sales + 50% Commissions + 50% Commissions + Warranty).

b) Expenses:

Now we'll look at the development costs, which include the cost of land acquisition, pre-construction spending, and construction spending. The figures can be found in the Deal Summary's development costs assumption section.

- Cost of Land Acquisition = Cost of Land

- Spending on pre-construction = Spending on pre-construction ($/month)

- Construction spending = (Development costs – Pre-construction spending)/number of construction months

- SUM of Total Development Costs

- (Land acquisition costs + Pre-construction costs + Construction costs)

c) Funding Cost and Capital Repayment Proceeds:

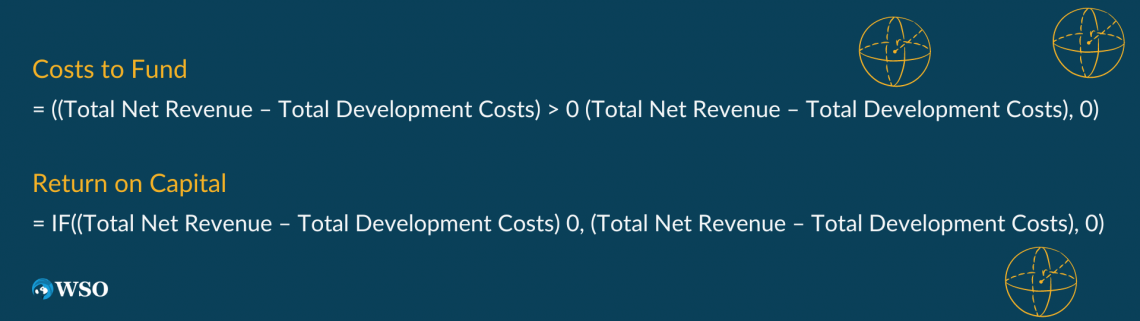

The Cost to Fund is the project cash flow shortfall that must be financed. When total net revenue exceeds total development costs, we have a negative cash flow that must be covered.

When total net revenue exceeds total development costs, we will have positive proceeds that we can use to repay borrowed capital. To compute the two numbers, we can use the following formulas:

Costs to Fund = ((Total Net Revenue – Total Development Costs) > 0 (Total Net Revenue – Total Development Costs), 0)

Return on Capital = IF((Total Net Revenue – Total Development Costs) 0, (Total Net Revenue – Total Development Costs), 0)

d) Financing:

Following that, we compute the loan balances, draws, repayments, and Interest accrued. The calculations for the first and subsequent periods are summarized below:

| First Period | Following Period | |

|---|---|---|

| Opening Balance Draws |

0$ = Land loan amount |

=Ending balance of previous Period = IF(Date > Construction start date, IF( Opening balance < Max loan amount, - Cost to fund,0),0) |

| Repayments | = - Min(Proceeds to pay back capital, Opening balance + Interest accrued) | = - Min(Proceeds to payback capital,Opening balance + Interest accrued) |

| Interest accrued | = Opening balance x interest rate / 12 | = Opening balance x interest rate / 12 |

| Ending balance | = Sum(Opening balance,draws,repayments, interest accrued) | = Sum(Opening balance,draws,repayments, interest accrued) |

We should also check quickly to ensure that none of the ending balances exceed the maximum loan amount.

e) IRR and free cash flow:

We can compute the project's levered free cash flows and resulting IRR.

- Equity Balance = SUM(Costs to Fund, Proceeds to Payback Capital, Loan Draws, Loan Repayments)

- Leveraged Free Cash Flow = first-period balance

- Previous Balance – Levered Free Cash Flow = Following Period Balances

Finally, we can compute the Levered IRR for this project using the XIRR formula:

- IRR levered = XIRR (All Levered Free Cash Flows, Corresponding period)

Financial Analysis of Real Estate: To Buy or Not to Buy?

In most cases, REFM is less complicated than traditional financial modelling.

This is due to the more limited purpose: we do not require 3-statement models, credit models, valuation, DCF models, merger models, or LBO models.

Furthermore, revenue and expense projections do not vary as much for companies in different industries.

The majority of real estate financial models can be summed up by a slight variation on Shakespeare's most famous quote:

"To buy, or not to buy?"

- Should you buy or build a property at the stated price?

- Is it possible to achieve the desired returns, or would that necessitate completely unrealistic assumptions?

- Would you lose money in the worst-case scenario, or would you survive even if the returns were disappointing?

Real estate financial modelling provides straightforward but powerful methods for answering these questions and making investment decisions.

Is real estate development a good career?

A real estate career in project development can generate the highest profits of any real estate career choice, particularly when developing commercial real estate. However, a failed real estate development project entails the most significant risk and loss.

or Want to Sign up with your social account?