Economic Efficiency

A state where every resource is optimally allocated to satisfy the needs of every individual while eliminating or minimizing wastes and inefficiencies altogether.

What Is Economic Efficiency?

Economic efficiency is a state where every resource is optimally allocated to satisfy the needs of every individual or entity while eliminating or minimizing wastes and inefficiencies altogether.

In economic terms, economic efficiency is related to optimal production and the distribution of scarce resources and is expressed as follows:

Minimum costs for producing goods and services while achieving maximum social benefits

It is crucial to remember the assumption that all other factors are fixed. For instance, a change that lowers the cost of production but also lowers the quality of the product does not indicate economic efficiency.

It is also important to remember that it is mainly a theoretical concept; it can be approached but is never attained.

Economists, in this case, look at the loss in reality and the loss that is calculated theoretically to see how efficiently the economy functions.

- Economic efficiency refers to the optimal use of resources to maximize the production of goods and services.

- An economy is considered efficient when it can produce the maximum amount of output from a given set of inputs, or conversely, it can produce a given level of output using the minimum amount of inputs.

- Productive efficiency is achieved when goods and services are produced at their lowest possible cost. This means that firms are using the best combination of inputs and the most efficient production techniques.

- Dynamic efficiency refers to the economy’s ability to improve over time through innovation, technological progress, and investment in human and physical capital.

Why is economic efficiency important?

Being efficient means making the most out of your resources. And because economic efficiency advocates limited government intervention or Laissez-faire, this leaves many factors solely up to the people in charge.

Having them play their cards right and make the right decisions would greatly benefit them in the following ways:

1. Reduced costs

Working towards efficiency lowers the cost of production, which could reduce the price of goods and services for consumers.

An efficient economy improves productivity and output production by maintaining the quality of its products while decreasing the amount spent on making them.

2. Increased profits

Since being efficient decreases the time spent on making products and lowers the cost of producing them, the economy will have an increased range of products which in return will fulfill a more significant number of customers and increase sales.

3. Equal access to goods and services

Economic efficiency promotes the fair allocation of goods and services to everyone.

In other words, no individual can benefit while costing another.

This makes it easy for businesses to distribute their goods and services and price them in a way that both consumers and the business can benefit from.

4. Balanced losses and gains

When economic efficiency is achieved, this promotes a balance of social benefits and business benefits between both the suppliers and consumers.

This means that a business may favor producing a good or providing a service instead of another due to increased demand.

Businesses in such economies may quickly adapt to the changes in consumer demand and compensate for any losses.

Types Of Efficiencies

When it comes to economic efficiency, we are met with several types, which include the following.

Productive Efficiency

This happens when the maximum number of goods and services are produced using a given number of inputs.

In other words, when resources are allocated most efficiently without affecting the quality of the product.

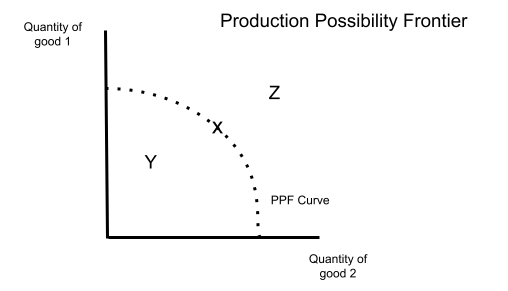

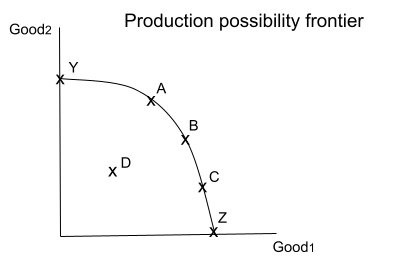

It is attained when the Average Cost (AC) of production is minimized and is best expressed on a production possibility frontier curve (PPF).

Based on the graph above, we are comparing the production of two different goods.

- Point Y on the graph lies below the PPF line, which means that the resources aren’t well distributed and thus aren’t giving the best efficient output.

- Point X lies on the PPF curve, which expresses that all resources have been well allocated, thus giving maximum output using the given input, resulting in optimal production efficiency.

- Point Z lies outside the PPF curve, which expresses an unattainable point given the scarce resources.

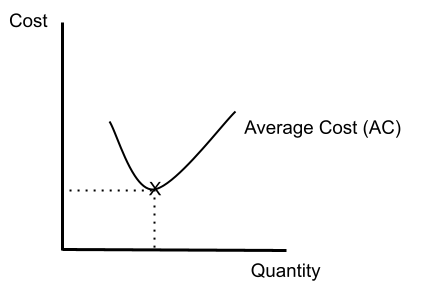

Production efficiency can also be expressed in another way:

The average cost of production, usually in a short-run period, or the cost of producing one unit of a product.

It is calculated as:

AC = Total cost / Quantity

- Total cost (TC): Total cost of producing the products

- Quantity (Q): Total number of outputs of products

Production efficiency is represented in the above graph as point X, the lowest point on the AC curve.

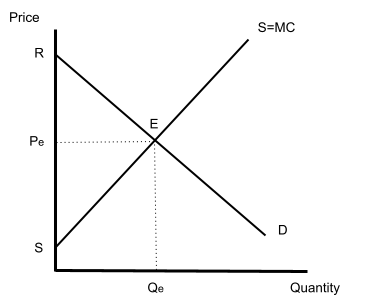

Allocative Efficiency

This is when the distribution of goods and services aligns with consumers’ preferences.

This type of efficiency allows consumers to pay an amount equal to how much they value the good/service. So producers must produce enough products to match their consumer demand.

In other words, it is when the value the consumers place on goods and services (the amount they’re willing to pay) is equal to the marginal cost (MC) of production.

MC is the cost of producing an additional unit of goods or services.

It is calculated as:

MC = ΔC / ΔQ.

Allocative efficiency is expressed as output that maximizes the total consumer welfare.

The condition for allocative efficiency for a market is to produce an output at a point where the market price is equal to the MC of supply.

According to the above graph, the supply curve represents the marginal cost, and the demand curve represents the consumers’ ability to pay for several goods. At the equilibrium price, Pe is equal to MC, thus indicating allocative efficiency.

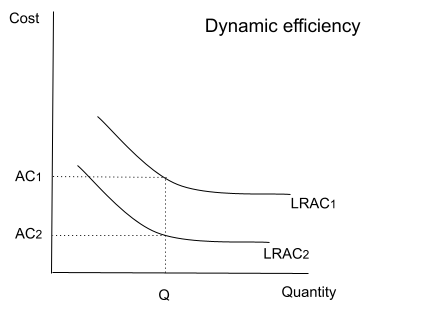

Dynamic Efficiency

It’s a process that happens in a market over a period of time and is linked to the pace of innovation because technology usually increases productivity and reduces costs.

This then leads to improvements in the range of choices of consumers as well as the quality of products. There are two ways markets can benefit from innovation.

- Product innovation: The creation of a good or service that is either new or an improved version of a previous one.

- Process innovation: Implementing new or improved production techniques to an existing product.

In other words, dynamic efficiency is the market helping to meet the constant change of wants and needs.

This type of efficiency is looked at in the long term and aims to bring down the marginal and average cost of supply.

Based on the above graph, there’s a comparison between the long-run average cost of year one and year 2. This indicates that the average cost for the same quantity has decreased from AC1 to AC2 - meaning they obtained dynamic efficiency.

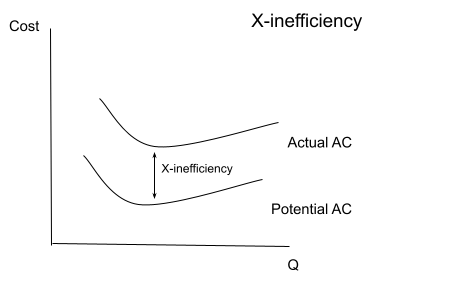

X-Efficiency And X-Inefficiency

While both these terms may seem like opposites, they are, in fact, the same economic concept.

X-efficiency calculates how close a firm operates to optimal efficiency, whereas

X-inefficiency focuses on the gap between potential and absolute efficiency.

- X-inefficiency occurs when a firm operates in a market that lacks real competition. This leads to the AC being higher than it would be in a competitive market.

Since there is almost no competition, this gives the monopoly supplier a weaker incentive to control costs and improve consumer welfare, thus lowering productivity.

- On the other hand, firms can achieve x-efficiency when the production goals are met or exceeded despite their insufficient means.

This is likely to happen when firms operate in competitive markets where suppliers are motivated to improve their production and consumer welfare.

Based on the above graph, the firm is facing x-inefficiency because the actual cost of production is higher than the cost it would need if it were to operate in a competitive market.

Technical Efficiency

This type of efficiency is when a firm produces a maximum output using the least amount of inputs or resources.

Technical efficiency = [actual output from given inputs/ potential output from given inputs] * 100

It can be shown on a PPF curve as well.

Based on the above PPF graph, the firm is producing goods at levels A, B, or C, all experiencing technical efficiency. Point D is technical inefficiency because some resources are used but don't produce maximum output.

Points Y and Z are also points of technical efficiency where resources can be used to produce maximum production of only one good, thus resulting in maximum efficiency.

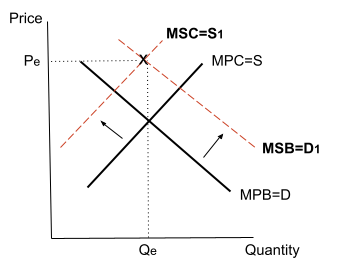

Social Efficiency

This is when private and external costs and benefits are considered to achieve optimal distribution of resources in a society.

It occurs when the marginal social benefit equals the marginal social cost.

Social benefit = Private benefit + External benefit

Social cost = Private cost + External cost

One way to achieve this would be for the government to impose taxes to help influence production and benefit society.

Based on the above graph, we see that we have social efficiency at point X because the marginal social cost (MSC) equals the marginal social benefit (MSB).

Both the marginal social costs and benefits are based on whether the firm faces positive or negative externalities.

How to Calculate Economic Efficiency

As mentioned, economic efficiency is producing maximum outputs using the least amount of input, hence measuring the relationship between inputs and outputs.

This can be in terms of measuring the cost, person-hours, materials needed for production, income revenues, or the number of products produced, respectively.

Economic efficiency can be mathematically calculated by a function of the ratio of the actual value of efficiency in an economy over its potential.

Another way is using a ratio of output over total input. It can also be expressed as a percentage by multiplying the ratio by 100.

![]()

This type of equation can be used to calculate efficiency in an economy.

Efficiency = Output/Input * 100

This equation can calculate how efficient a firm or market is.

Ways to Improve Economic Efficiency

Since economic efficiency is only a theoretical term and can never be achieved, it can at least be improved through a few steps.

Increase Competition

Competition between firms gives the incentive to increase efficiency to stay in the market, whereas the least efficient/productive firms are forced to leave the market.

This isn’t the case in monopolistic markets where they lack competitors.

In such cases, these firms have no incentive to improve their productivity.

That’s because they are not in competition with anyone. Hence there aren’t any substitutes or alternatives to the goods and services they provide.

Advancement Of Technology

Undoubtedly, technology plays a huge role in our day-to-day lives. It controls all our decision-making processes as well as other essential life functionalities.

From a firm’s perspective, machinery is key in improving efficiency, and as technology advances, it paves the way for enhancing the production of goods.

Compared to labor, technological advancement decreases the time needed to produce a product and avoids wasting resources.

Improve Skills

Skills used in labor work or machinery can be a great indicator of how a firm will function in the economy because it is directly linked to the production of its outputs.

This can be through the optimal distribution of laborers or the introduction of machinery for the specific production of outputs.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?