Basel Accords

A set of international banking laws for central banks and banking supervisors worldwide.

What Are The Basel Accords?

The Basel Accords are a set of international banking laws developed by the Basel Committee on Banking Supervision (BCBS), a global forum for central banks and banking supervisors worldwide.

Basel I, implemented in 1988, created a framework for gauging credit risk and required banks to maintain a certain level of capital in proportion to their risk-weighted assets. This ensured banks had adequate capital to pay their losses if a crisis occurred.

Basel II, implemented in 2004, aims to increase risk measurement accuracy and better link capital requirements with the degree of risk banks face.

It also included additional operational risk management criteria and emphasized regulatory assessment of banks' risk management processes.

Basel III, implemented in 2010, reacted to the 2008 global financial crisis. It raised the minimum amount of capital banks must retain and imposed additional liquidity risk management criteria.

Basel III also offered a new methodology for monitoring counterparty credit risk and emphasized the importance of bank capital quality.

The Basel Accords are crucial because they establish a uniform framework for banking rules across nations and regions, creating a fair playing field for banks operating in various jurisdictions.

They have also strengthened regulatory monitoring of banks' risk management methods, contributing to the banking system's safety and soundness.

The Basel Accords aim to guarantee financial stability and limit the danger of bank failures.

- The Basel Accords are international banking laws developed by the Basel Committee on Banking Supervision (BCBS), a global forum for central banks and banking supervisors worldwide.

- They aim to enhance financial stability by establishing minimum capital requirements and other safeguards for banks.

- The Basel Accords require banks to identify, measure, monitor, and control risks, while Basel II and III emphasize stronger oversight by regulatory authorities.

- The Basel Accords significantly impact the global banking industry by standardizing regulatory practices across countries and enhancing the stability of the international financial system.

History of Basel Accords

In the history of the Basel Accords, a body known as The Banking Regulations and Supervisory Practices was established in 1974.

Ten nations supported it. The partnership was a reaction to the Bankhaus Herstatt (West Germany) collapse. Bankhaus significantly disrupted global currency and banking.

The committee met for the first time in February 1975. As a result, the members met regularly—four times annually.

The G10 nations—the Netherlands, the US, the UK, Italy, Japan, Sweden, Switzerland, Belgium, Canada, France, and Germany—were the original members of the Basel committee. However, the network grew to include 28 jurisdictions and 45 institutions.

The committee put a lot of effort into closing gaps in international banking so that no bank would be exempt from oversight. As a result, international supervisory coverage is the official term for this function.

The Concordat made declarations about banking regulations in 1975. The Principles for the Supervision of Banks' Foreign Establishments was the new name for this document when further revisions were made in May 1983.

The Basel Committee established a cross-border banking oversight authority in October 1996. In addition, G7 finance ministers collaborated on a paper from 1996 that called for effective oversight of all markets, particularly those in emerging markets and economies.

Note

The 1997 paper revision added 25 Basel Accords principles of oversight.

The most recent addition is the Basel principles update from September 2012. Since then, 29 norms, powers, and principles have been highlighted in the paper.

Basel I: The Basel Capital Accord

The Basel Capital Accords, sometimes called Basel I, was established in the 1980s in reaction to the American debt crisis. The debt crisis raised questions about the capital adequacy of foreign banks.

Basel I was created to reduce risk to customers, financial institutions, and the economy. The capital reserve requirements for banks were lowered when Basel II was introduced a few years later.

This drew some criticism, but many banks continued to operate under the old Basel I framework, which was eventually expanded by the Basel III addenda because Basel II did not replace Basel I.

G10 nations backed the implementation of higher capital requirements and adequacy standards. As a result, banks received the amended banking regulations in July 1988.

The following are Basel I's essential components:

- Banks must retain a minimum of 8% in risk-weighted assets under Basel I.

- Not just member countries but all nations adopted the framework.

- In 1998, a change was made to the agreement to add generic protections for loan losses.

- The proposed agreement included both financial and credit risks.

Basel II: The New Capital Framework

In 2004, the second Basel resolution was announced. But persistent efforts went before it. The committee proposed a new capital adequacy framework to replace the 1988 agreement in June 1999.

In addition to confirming the need for banks to maintain a capital reserve equivalent to at least 8% of their risk-weighted assets, Basel II expanded upon Basel I by providing rules for calculating minimum regulatory capital ratios.

Basel II creates three layers for a bank's permissible regulatory capital. The more secure and liquid the tier's assets are, the higher it is.

The following are Basel II's features:

- The agreement provided further details and specificity to the rules outlined in the 1998 agreement.

- The new agreement examined the internal evaluation procedure and strengthened market discipline through disclosure. It further encouraged good banking procedures as a result.

- The second agreement was centered on controlling capital requirements.

- The range of collaboration between home and host supervisors was broadened.

Basel III: 2008 Financial Crisis Response

Many people think Basel III was just a reaction to the financial crisis of 2008. But even before the September 2008 Lehman Brothers bankruptcy, the banking system had already identified flaws.

Liquidity problems in the banking industry resulted from bad governance and an ineffective incentive system.

The collapse of the housing market was only the result of underlying inefficiencies. Basel resolutions always change, but banking institutions become stable only if the rules are followed.

The Basel Committee unveiled a new accord regarding general capital design and liquidity improvements in September 2010. As a result, the Basel III Agreement was given that moniker. Basel III underwent additional revisions in December 2010.

The following are Basel III's features:

- Basel III modified the system in charge of keeping track of liquidity risks.

- It promoted making banking systems more resilient.

- It concentrated on the type and amount of common equity.

- Common equity requirements were raised from 2% to 4.5%, with a further 2.5% cushion. Common equity in this context refers to a share of banks' risk-weighted assets.

- The agreement also included a leverage ratio that could cover 30 days' worth of stress.

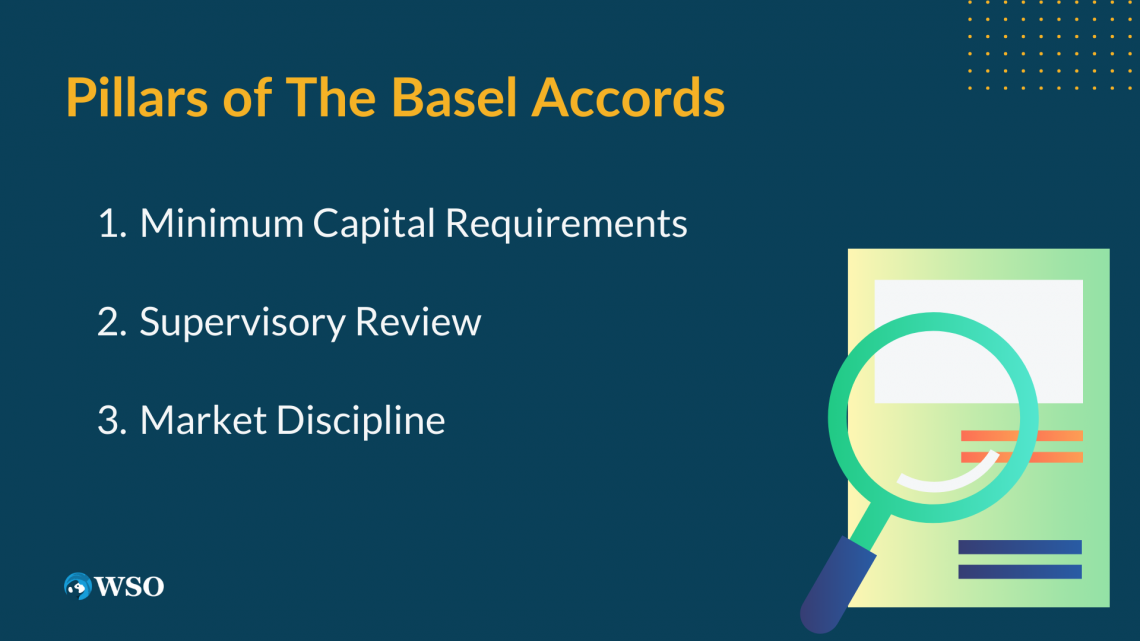

Pillars of The Basel Accords

The Basel Accords offer a comprehensive framework for banking rules and are built on three pillars. They are as follows:

Minimum Capital Requirements

The first pillar mandates that banks maintain a minimum amount of capital in proportion to their risk-weighted assets. In the case of a crisis, this guarantees that banks have sufficient capital to pay their losses.

The Basel Accords mandate that banks maintain a minimum Tier 1 capital ratio of 6%, a countercyclical capital buffer that may be raised during periods of economic boom, and an extra capital conservation buffer of 2.5%.

Banks' overall minimum capital requirement is 10.5%, with a minimum Tier 2 capital ratio of 2%.

Supervisory Review

The second pillar mandates that regulators undertake supervisory reviews of banks' risk management procedures and that institutions establish strong risk management practices.

This includes stress testing and scenario analysis to detect risks and ensure institutions have proper risk management frameworks.

A qualitative evaluation of banks' risk management procedures, corporate governance, and regulatory compliance is also a part of the supervisory review process.

Market Discipline

By mandating banks to inform market participants of their capital adequacy and risk management procedures, the third pillar seeks to encourage market discipline.

This entails providing details on their capital adequacy ratios, risk-weighted assets, and important risk markers.

Note

The third pillar seeks to enhance market discipline and assist in aligning the interests of banks and their stakeholders by promoting more openness and disclosure.

The Basel Accords' three pillars collectively offer a comprehensive framework for banking laws that encourage financial stability, lessen the danger of bank failures, and guarantee the security and soundness of the world banking system.

What Is New in Basel IV?

As part of the completion of Basel III, the Basel Committee approved modifications to the worldwide capital requirements in 2017.

The modifications are so extensive that they are increasingly perceived as a whole new framework, known as "Basel IV," scheduled to go into effect under transitional regulations in 2025.

The Basel Committee's investigation revealed a concerning level of diversity in how banks calculate their risk-weighted assets. As a result, the most current rules restrict banks' use of internal risk models to restore the validity of those calculations.

Advanced internal risk models provide the biggest flexibility in estimating credit risk, frequently producing substantially lower risks than the regulator's conventional model.

Banks can utilize these frequently more complex and sophisticated methods under Basel IV.

Basel IV also adds a measure known as an "output floor" that bans a bank from measuring its risk exposure internally to the point where it yields less than 72.5% of the standard method.

Sonebäck says you can lower your risk-weighted assets by a maximum of 27.5%. So this is a significant modification that affects the value you may derive from these internal models. The most affected banks are those that rely on internal models.

Note

The new reforms alter the bank's overall exposure definition, changing the leverage ratio. They also alter the operational risk and credit valuation adjustment (CVA) frameworks.

The BCBS was still adjusting Basel III's provisions as it awaited its final implementation deadline. As a result, these suggestions are now commonly referred to as Basel IV in some circles of the financial industry.

In contrast, William Coen, the Basel Committee's then-secretary general, stated in a speech in 2016 that he did not think the modifications were significant enough to warrant their Roman numeral.

Basel IV started its implementation on January 1, 2023, whether it is only the conclusion of Basel III or a "Basel" in and of itself.

Note

The committee's main objective is to "improve the comparability of banks' capital ratios and restore credibility in the calculation of RWAs."

Here are several changes coming into Basel IV:

1. Credit Risk

Enhancing the standardized procedures for credit, operational, and credit valuation adjustment (CVA) risk in the previous accords.

New risk ratings for numerous asset classes, such as bonds and real estate, are outlined in these regulations. The cost of derivative instruments is referred to as credit valuation risk.

2. Constraining Use of Internal Model Approaches

Restricting how some banks compute their capital requirements using internal model methodologies. Unless they receive regulator approval to employ an alternative, banks will typically be required to adhere to the standardized strategy outlined in the accords.

Banks have been accused of underestimating the amount of capital they need to hold in reserve and the riskiness of their portfolios due to internal models.

3. Leverage Ratio

A leverage ratio buffer is added to restrain further the leverage used by globally significant banks (banks whose failure would jeopardize the global financial system). As a result, they must hold more money in reserve due to the greater leverage ratio.

4. Replacing Basel II Output Floor

Changing the Basel II production floor to one that is more risk-sensitive. The difference between the amount of capital a bank would be obliged to have in reserve based on its internal model and not the standardized model is the subject of this clause.

Regardless of what their internal model says, the new regulations would compel banks to keep capital that is at least 72.5% of the amount indicated by the standardized model by the start of 2027.

Researched and authored by Karnic Boudoughian

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?