Net Interest Margin

The difference between the interest income generated by banks or other financial institutions and the amount of interest paid out to their lenders.

What Is Net Interest Margin?

The net interest margin (NIM) is a financial metric that assesses the difference between the interest income generated by banks and financial institutions and the total amount of interest paid to the borrowers.

Net Interest Margin (NIM) is a commonly used financial metric in banks and credit unions to determine profitability. It is calculated by subtracting the expenses incurred by a bank or a credit union on investment from the income generated (a step commonly referred to as netting) and dividing the result by the average of invested assets.

NIM is a crucial metric for assessing the performance and health of a financial institution's finances as it reflects its capacity to earn money by lending and investing, which constitutes its main source of income.

A bank or credit union with a high NIM will likely be more profitable since it can properly manage its assets and liabilities.

Note

Changes in interest rates, modifications to the balance sheet's composition, and alterations to the degree of credit risk and liquidity risk can all have an impact on a financial institution's NIM.

For instance, if a bank charges greater interest rates on loans than on deposits, its NIM will be positive, and the bank will generate profits. On the other hand, the net interest margin will be negative, and the bank will experience a loss if the interest rates on deposits are higher than those collected on loans and investments.

NIM Formula = (Interest Received - Interest Paid) / Average Invested Assets

Let's take a hypothetical example to illustrate this formula. Suppose a bank has the following financial information:

- Interest income generated by interest-earning assets: $500,000

- Interest expense incurred by interest-bearing liabilities: $100,000

- Average interest-earning assets: $20 million

By applying this formula,

NIM = (500,000 - 100,000) / 20,000,000 = 400,000 / 20,000,000

NIM = 0.02 or 2.0%

In this example, the NIM of the bank comes out to be 2.0%. This means the bank earns a 2.0% return on its average interest-earning assets after accounting for its interest expenses.

- Net interest margin (NIM) is a financial metric banks and credit unions use to determine their profitability. It reflects the institution's capacity to earn money by lending and investing, which constitute its main source of income.

- NIM is calculated by subtracting the expenses incurred by a bank or credit union on an investment from the income generated and dividing the result by the average of invested assets.

- NIM is of great importance to banks and other financial institutions because it measures profitability, reflects the quality of the loan portfolio, helps banks manage interest rate risk.

- Factors that affect NIM include the interest rate environment, loan pricing, deposit pricing, asset and liability mix, interest rate sensitivity, credit risk, and operating expenses.

Importance of Net Interest Margin

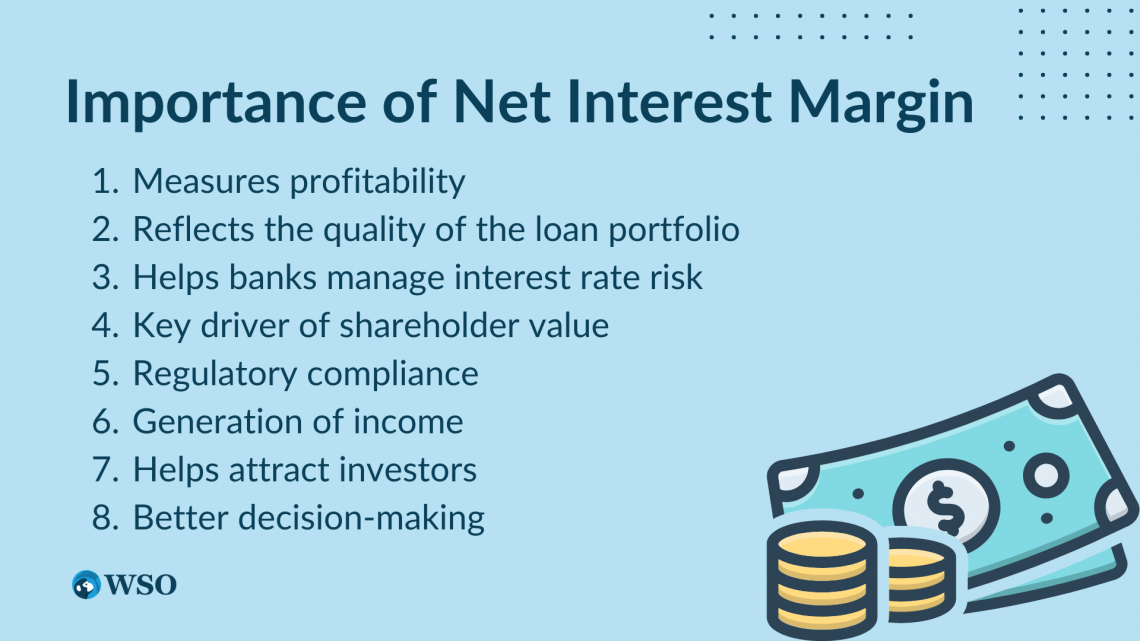

NIM is of great importance to banks and other financial institutions. Some of the reasons behind it are:

- Measures profitability: NIM is an important indicator of profitability for banks and other financial institutions. A higher NIM shows that a bank is more lucrative since its interest income exceeds its interest expenses.

- Reflects the quality of the loan portfolio: NIM is a reflection of the quality of the loan portfolio. A bank with a higher proportion of high-quality loans will likely have a higher NIM because these loans generate more interest income.

- Helps banks manage interest rate risk: NIM is an important tool for banks to manage interest rate risk. Banks with a higher NIM can better withstand fluctuations in interest rates because they have more cushion to absorb interest rate changes.

- The key driver of shareholder value: NIM is a key driver of shareholder value for banks and other financial institutions. A higher NIM is associated with higher profitability, which can lead to higher earnings per share and higher stock prices.

- Regulatory compliance: NIM is an important factor in regulatory compliance for banks and other financial institutions. Regulators monitor NIM to assess a bank's financial health and may require banks to take action if their NIM falls below certain thresholds.

- Generation of income: NIM is a key source of income for banks. A large NIM indicates that the bank's interest-earning assets are bringing in more money than its interest-bearing liabilities are costing it.

- Helps attract investors: A consistently high NIM may attract investors to the bank. In addition, investors will likely view a bank that can generate consistent profits from its core lending and borrowing activities as a sound investment.

- Better decision-making: By analyzing the NIM, bank management can make better decisions about their lending and investing activities. In addition, it can help them identify growth opportunities and adjust their strategies as needed.

Factors Affecting Net Interest Margin

The NIM of a bank is affected by various factors:

- Interest rate environment: When interest rates rise, banks can earn higher interest income on their loans and other interest-earning assets, increasing their NIM. Conversely, when interest rates fall, banks earn lower interest income, which can reduce their NIM.

- Loan pricing: A bank's NIM can be affected by changes in loan pricing. If a bank raises its loan pricing, it can earn more interest on its loans, increasing its NIM. However, if a bank lowers its loan pricing, it can reduce its interest income and lower its NIM.

- Deposit pricing: Deposit pricing refers to the interest rate paid on deposits. A bank's NIM can also be affected by changes in deposit pricing. For example, if a bank lowers its deposit pricing, it can reduce its interest expense and increase its NIM and vice versa.

- Asset and liability mix: Loan interest revenue is often higher for banks than interest-earning assets like securities. As a result, banks with a higher share of loans in their asset mix can have a higher NIM than banks with a lower share.

- Interest rate sensitivity: Suppose a bank's assets are more sensitive to interest rate changes than liabilities. In that case, changes in interest rates can have a greater impact on its interest income than its interest expense. This can result in a higher NIM.

- Credit risk: If a bank has a higher proportion of low-quality loans in its asset mix, it may have to set aside more provisions for loan losses. This can reduce its interest income and lower its NIM.

- Operating expenses: A bank's operating expenses, such as salaries, rent, and technology costs, can also impact its NIM. If a bank has higher operating expenses, it may have to generate more interest income to cover these expenses, which can reduce its NIM.

Risks and challenges associated with Net Interest Margin

NIM is a critical financial metric for banks and financial institutions. While NIM provides insight into an institution's profitability, it also carries inherent risks. These risks include:

1. Interest rate risk

Because interest rates influence both interest revenue and interest expenses, changes in interest rates might result in changes in NIM. In a situation where interest rates are rising, interest costs might rise faster than interest revenue, which would pressure NIM to the downside.

2. Credit risk

The poor credit quality of borrowers can lead to increased non-performing loans, negatively impacting NIM. In addition, banks that lend to borrowers with a higher risk of default may experience higher loan losses, reducing interest income and NIM.

3. Liquidity risks

A bank may be obliged to borrow money at higher rates if its current funding sources are insufficient to cover its debts, lowering its NIM. Banks with a high reliance on short-term funding sources may be more susceptible to liquidity shocks, resulting in funding constraints and a decreased NIM.

4. Competition

Increased competition can pressure NIM as banks may need to lower their interest rates to remain competitive. This can result in reduced interest income and NIM for the bank.

Weak economic conditions can lead to lower loan demand, which can reduce interest income and NIM.

Note

In a recessionary environment, loan defaults may also increase, leading to higher loan losses and lower NIM.

6. Regulatory changes

Regulation changes, such as new capital requirements, can affect a bank's ability to generate NIM. For example, increased regulatory requirements may limit banks' ability to take on riskier loans, reducing interest income and NIM.

7. Asset-liability management

Poor management of the bank's asset and liability mix can lead to a negative impact on NIM. Banks that hold too many long-term assets while relying on short-term funding sources may experience lower NIM.

Net Interest Margin and Interest Rates

The level of interest rates is a critical determinant of a bank's NIM. When interest rates rise, the bank earns more interest income from its loans and investments, which can lead to higher NIMs.

Conversely, when interest rates fall, the bank earns less interest income, which can reduce its NIMs.

However, the relationship between interest rates and NIM can be complicated. Numerous variables, such as the mix of deposits, interest rate sensitivity, interest rate environment, and competition, can impact the relationship.

1. Loan Portfolio Composition

The composition of a bank's loan portfolio can impact its NIM in response to changes in interest rates.

For instance, PQR Bank has a sizable portfolio of long-term, fixed-rate loans with rising interest rates. PQR Bank, in this situation, could be unable to raise the interest rates it charges on such loans, which would cause a drop in NIMs.

Conversely, if it had a large portfolio of adjustable-rate loans, it may benefit from rising interest rates, as the interest income on these loans will increase.

2. Deposit Mix

The bank's mix of deposits can also affect its NIM in response to changes in interest rates.

For example, if PQR Bank has a high proportion of time deposits, it may experience less of an impact from rising interest rates than a bank with a higher proportion of demand deposits. This can be attributed to demand deposits, which comprise a major chunk of PQR Bank’s portfolio and are more sensitive to interest rate changes.

If PQR Bank had fixed deposits - whose interest rate is fixed for a predetermined period, it might have experienced a minimal impact from the changes in interest rates.

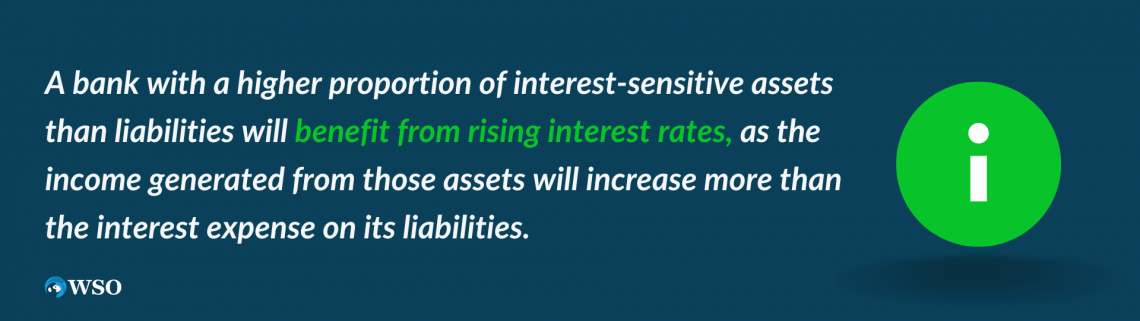

3. Interest Rate Sensitivity

The interest rate sensitivity of a bank's assets and liabilities is another important factor in the relationship between NIM and interest rates.

A bank with a higher proportion of interest-sensitive assets than liabilities will benefit from rising interest rates, as the income generated from those assets will increase more than the interest expense on its liabilities.

Conversely, a bank with a higher proportion of interest-sensitive liabilities than assets will experience a decline in NIM when interest rates rise.

4. Interest Rate Environment

The interest rate environment also influences the relationship between NIM and interest rates. Low-interest rates can make it difficult for banks to earn enough interest income to cover their interest costs, which lowers NIMs.

Conversely, in a high-interest-rate environment, banks may be able to generate higher NIMs as interest income from their assets increases.

5. Competition

Finally, competition among banks can also influence the relationship between NIM and interest rates. For example, if multiple banks in a market increase their interest rates in response to rising interest rates, this can pressure NIMs as banks compete for deposits.

On the other hand, a bank may produce a higher NIM if it charges a higher interest rate than its rivals on its loans and investments.

Net Interest Margin Analysis

Analyzing NIM over time can provide valuable insights into a bank's performance and risk exposure.

Trend Analysis of NIM

Trend analysis of NIM over time can reveal whether it is increasing, decreasing, or stable. For example, a decreasing NIM may indicate that a bank faces increased competition or interest rates decline. This can put pressure on the bank's earnings and profitability.

An increasing NIM may indicate that a bank is successfully managing its interest rate risk or that it has improved its asset-liability management practices. This can boost the bank's profitability and earnings.

A stable NIM may indicate that a bank's core lending and deposit-taking activities are performing consistently.

Benchmarking NIM Against Industry Peers

Benchmarking NIM against industry peers can also provide insights into a bank's relative performance. For example, a bank with a higher NIM than its peers may better manage its core lending and deposit-taking activities.

Note

It's important to consider other factors, such as credit risk and non-interest income when comparing NIM across different banks. For example, a bank may have a higher NIM but higher credit risk or lower non-interest income than its peers.

Comparison of NIM Across Different Financial Institutions

Comparing NIM for banks versus credit unions can provide insights into how different business models and regulatory frameworks impact NIM. For example, banks may have a higher NIM because they can access cheaper funding sources or offer higher interest rates on loans.

On the other hand, credit unions may have a lower NIM due to their focus on loan rates. Credit unions, on the other hand, may have a lower NIM due to their focus on serving their members and offering lower rates on loans and higher rates on deposits.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?