Protective Put

A risk-management approach that uses options contracts to safeguard investors against the depreciation of their investments.

What Is A Protective Put?

In the finance world, risk management is one of the key skills to learn. To manage the risk of a particular investment someone will make for years, new research is conducted, and new methods are invented. These methods are called risk management strategies.

One very common risk management strategy is the protective put. It is one of the famous options strategies used to protect investments from huge losses.

A protective put is a risk-management approach that uses options contracts to safeguard investors against the depreciation of a stock or asset they hold. The hedging method entails an investor paying a premium to buy a put option.

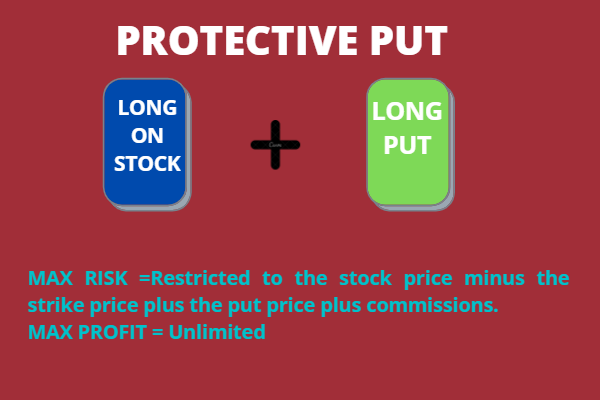

A protective put is a risk management and options strategy in which one buys a put option with a strike price that is either equal to or near to the current price of the underlying asset while maintaining a long position in the underlying asset (stock, for example). Synthetic calls are another name for a protective put technique.

It is also called married put. An investor buys shares of a stock and enough put options to cover those shares at the same time. This method will have the same net payoff as buying a call option in the long run.

It is generally utilized by an investor who is still optimistic about a stock but wants to protect himself from potential losses and uncertainties. In the event that the asset's price falls, it functions as an insurance policy, providing downside protection.

Understanding A Protective Put

The nature of insurance is comparable to a protective put strategy. A protective put's primary objective is to reduce possible losses that can arise from an unanticipated decline in the value of the underlying asset.

Using this tactic does not completely cap the investor's prospective earnings. The underlying asset's growth potential determines the strategy's profit margin. The premium paid on the put, however, takes away from some of the earnings.

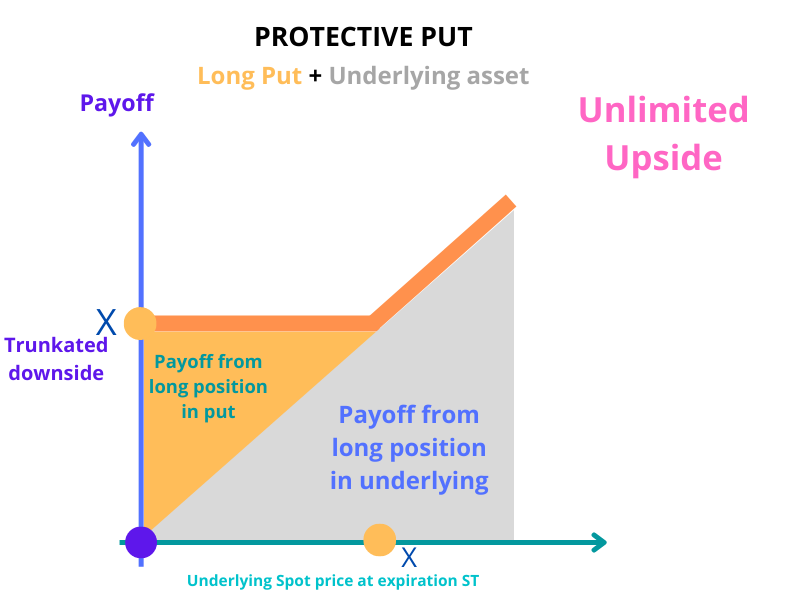

So, a protective put is nothing but a combination of a long put and a long equity position. There are usually two reasons why an investor might opt for the defensive put strategy:

- To reduce risk when purchasing a stock for the first time. This is also called a "married put."

- The short-term outlook is negative, but the long-term forecast is positive, protecting a previously purchased investment.

However, because profits from the option will offset any losses in the long stock position below the put option's strike price, the protective put strategy does set a maximum loss limit. Bullish investors who seek to hedge their long positions in the asset usually use a protective put strategy.

For example, one put is acquired, and 100 shares are purchased (or owned). The purchased put protects the strike price if the stock price falls. However, the protection is only valid until the expiration date. If the stock price rises, the investor reaps the full benefits minus the put cost.

Maximum Profit:

Because the underlying stock price can climb endlessly, the potential return is limitless. The total profit, however, is lowered by the cost of the put and commissions.

Maximum Risk:

The amount of risk is restricted to the stock price minus the strike price plus the put price plus commissions. In the example above, let's say the put price is $3.25 per share, and the stock price is equal to the strike price, $100. As a result, the maximum risk is $3.25 per share plus commissions. The full risk is realized if the stock price is at or below the put's strike price at expiration. If the stock price falls below a certain level, the put can be exercised or sold.

At expiration, the stock price must equal the breakeven price.

Maximum risk = price of the stock - strike price + the cost of the put + commissions

In this case,

$100.00 - $100 + 3.25 + 0 = $3.25.

Even if the underlying asset's price decreases, this establishes a known floor price below which the investor will not lose any more money.

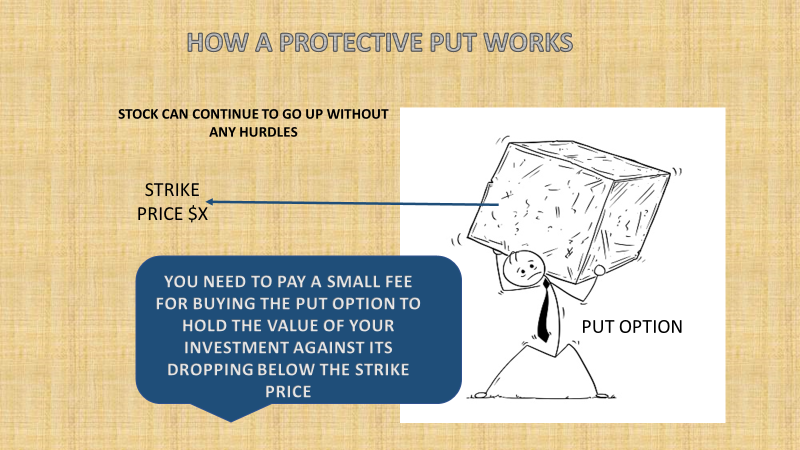

How A Protective Put Works

As the name suggests, it protects an investment from adverse results. A put option is a contract that allows the owner to sell a certain amount of an underlying security at a predetermined price before or on a certain date.

Unlike futures contracts, option contracts do not bind the holder to sell the asset; instead, they allow them to do so if they desire. The strike price is the contract's set price, and the stipulated date is the contract's expiration date or expiry.

Usually, 100 shares of the underlying asset equal one option contract. The owner of a put option may sell a certain amount of the underlying security at a predetermined price before or on a specific date.

Put options do not come free. Instead, an option contract costs a minimal premium. This price is determined by the current price of the underlying asset, the time remaining until expiration, and the asset's implied volatility (how likely it is that the price will change), along with a litany of other factors known as the "Greeks."

Example of a protective put

Let's say you have ten shares of PQR Ltd. in your portfolio, each valued at $100. You firmly believe it will move upwards in the long term. However, there is some news of a new COVID-19 variant and rumors of lockdown.

This situation poses risks for the company, and the share price could tumble shortly. However, as you predict a surge in the future, you don't want to sell the stock.

At the same time, the downside risk is very real. So, to hedge your investment, you decide to use a protective put. First, you purchase a put option, protecting a portion of your equity position for as long as the option contract is in force.

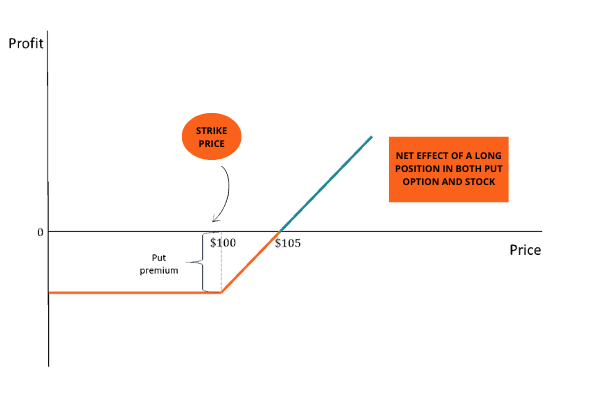

Let's assume the put option has a premium of $5. As a result, you buy one protective put contract with a strike price of $100 (one put agreement contains 100 shares).

The company's share price now determines the protective put's profit in the future. There are a variety of possible outcomes:

1. If the share price goes above $105:

You will obtain an unrealized benefit.

The profit can be determined using the following formula:

Current share price – $100 (previous market price) - $5 (premium)

The put option will not be used, as exercising it would mean selling your shares at a price lower than market value.

2. If the share price is between $100 and $105:

You will lose money or reach the breakeven point. The premium you paid for the contract is to blame for the slight loss. The put will not be executed, as in the preceding situation.

3. If the share price goes below $100:

You will use the defensive put option in this scenario to limit your losses. After the put is exercised, you'll sell your 100 shares at $100. As a result, your loss will be restricted to the cost of the protective put, $5.

Finally, the investor should remember that the put premium is essentially the cost of the position's insurance. If the stock maintains over $100, it may be argued that they would have been better off not buying the put. However, it provides peace of mind and protection in the event of a negative catastrophe, as does all insurance.

Summary

The put option's strike price is a stop-loss line for the underlying equity. In a protective put, the ideal scenario is for the stock price to rise significantly, which would help the investor's long-term stock position.

However, the put option will expire worthless in this situation, and the investor will have paid the premium.

To briefly summarize, the advantages and disadvantages of using a protective put are discussed below:

Advantages

- It provides downside protection from an asset's price drops for the cost of the premium.

- It allows investors to keep their positions in a stock that has the potential to grow.

Disadvantages

- When an investor buys a put, and the stock price rises, the premium cost diminishes the trade's returns.

- The premium adds to the trade's losses if the stock falls in value while a put is active.

Because the timing of protective puts might impact the stock's holding period, there are crucial tax implications in a protective put strategy. As a result, the stock profit or loss tax rate may be impacted.

When calculating taxes on options trades, investors should seek professional tax counsel. The following issues are taken from The Options Industry Council's pamphlet "Taxes and Investing," which is accessible for free.

On a share-for-share basis, "protective puts" and "married puts" include the identical combination of long stock and long puts, but the titles indicate a difference in when the puts are purchased. The term "married put" refers to the acquisition of both stock and puts simultaneously.

A "married put" means that the stock and puts are purchased simultaneously, and married puts have no impact on the stock's holding term. Long-term rates apply if a stock is held for more than a year before being sold, regardless of whether the put was sold for a profit or loss or whether it expired worthless.

or Want to Sign up with your social account?