Accounts Receivable

The money for goods and services a company has delivered or used by customers but has not yet paid for

What Are Accounts Receivable (AR)?

Accounts Receivable (AR) is the money for goods and services a company has delivered or used by customers but has not yet paid for. It is a current asset listed on the balance sheet, representing the amount for goods and services delivered but not yet paid for by customers.

It is created when customers buy goods and services on credit, which requires payment within a short period. If a company has receivables, it has made a sale on credit but has yet to collect the money from the purchaser.

When an organization extends credit to the client, it allows a period for the clients to pay the sum after the deal is acknowledged. The time span could differ from 30 days to a couple of months.

Accounts Receivable are considered liquid assets because they can be used as collateral to secure loans, help meet short-term debt, and are part of the company's working capital.

- Accounts Receivable (AR) represents money for goods and services a company has delivered but not yet received payment for. It is a current asset on the balance sheet created when customers buy on credit.

- Understanding AR is crucial for investment banking, equity research, and accounting professionals. It plays a key role in analyzing the cash conversion cycle and a company's cash flow.

- AR is essential for business analysis, but growing receivables without timely payments can strain finances. Risks include bad debt and cash flow deficiencies, emphasizing the importance of managing receivables effectively.

- To improve AR, businesses can offer discounts, impose penalties for late payments, use collection services, and establish a line of credit to address cash flow needs.

Understanding Accounts Receivable (AR)

Some businesses allow paying the bill on credit to make the process easier. For example, suppose a company sells laptops. Because the unit price for a laptop is high, some people may not have that large amount of money at the time that they want to buy the laptop.

In this situation, the customers can pay in credit and pay the bill at the end of the month. Although the laptop firm has not received money, they have already delivered the laptop to the customers.

Businesses typically issue invoices to clients and customers with specific payment terms. While most terms have a quick turnaround time, some may extend up to a full calendar year before the final payment is due.

We record the amount customers owe under the current asset, which is called accounts receivable.

This concept is essential in the accounting and finance field. For professionals in investment banking, equity research, and accounting, understanding accounts receivable is crucial for analyzing the cash conversion cycle and a company’s cash flow.

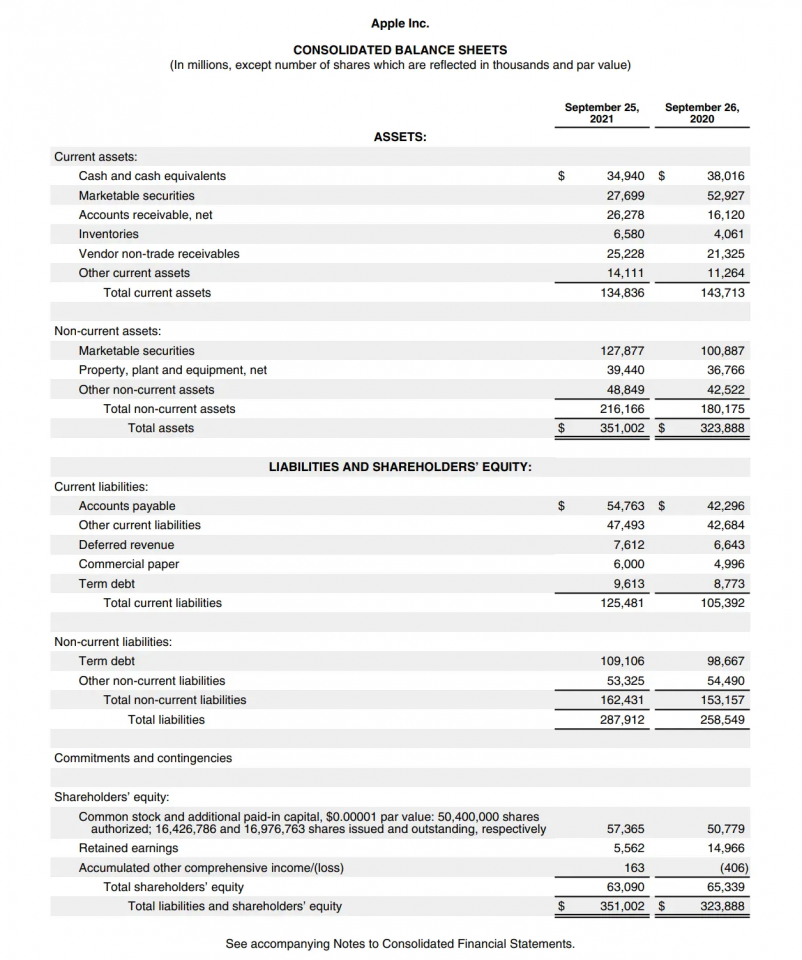

Where do you find Accounts Receivable (AR)? We can find annual or quarterly reports from a particular company on the balance sheet.

Let’s take the example of Apple Inc.

Benefits of Accounts Receivable

It is an important concept for business analysis, measuring the ability of a company to cover short-term obligations through its cash flows.

Tracking your receivables is crucial to managing your cash flow. While your sales might be going well, if your receivable continues to grow and your customers aren’t paying you fast enough, it could lead to financial strain or potential bankruptcy.

Fast growth poses challenges for small businesses, especially when many customers pay on credit. This can make it difficult for your company to pay operating expenses promptly in the future.

Tracking receivables is crucial for a business to ensure the timely collection of money owed.

Risks of Outstanding Accounts Receivable Balances

Some of the risks are:

- Bad Debt: If a company has a high AR and is uncollected for a long time, it would probably be a bad debt. It means the company that owes money to you goes bankrupt or cannot pay the invoice.

- Cash Flow Deficiencies: AR is just a number written on the balance sheet, but the company has no cash inflow from the transaction. The company needs cash to operate and pay its expenses. If the AR is too high, a company may run short of cash to pay the expense in the long run.

Accounts Receivable vs. Accounts Payable

Accounts Payable is an accounting term that describes the money owed to vendors or suppliers for goods or services purchased on credit. It will be recorded on the balance sheet as liabilities.

These two concepts are regularly compared as part of liquidity analysis to determine whether there are sufficient funds in AR to settle outstanding liabilities. This comparison commonly uses current ratios, although quick ratios can also be used. Other differences between AR and AP are:

| Aspect | Accounts Receivable | Accounts Payable |

|---|---|---|

| Definition | Money owed to a company by its customers | Money a company owes to its suppliers |

| Nature | Asset - represents money to be received | Liability - represents money to be paid |

| Source | Sales of goods or services on credit | Purchases of goods or services on credit |

| Timing | Created when sales are made on credit | Created when purchases are made on credit |

| Role in Cash Flow | Increases cash inflow when collected | Decreases cash outflow when paid |

| Management Importance | Critical for liquidity and working capital | Important for managing vendor relationships and cash flow |

| Aging Analysis | Tracked to monitor overdue payments | Tracked to manage timely payments to avoid late fees |

| Example | Invoicing a customer for products sold | Receiving an invoice from a supplier |

Accounts Receivable Related Calculations

The accounts receivable turnover ratio is helpful for business owners to gauge how effectively the company manages its revenue and assets. A higher turnover ratio indicates that a business has efficiently converted accounts receivable into cash over time for the goods or services it has provided.

There are a few calculations related to this topic:

1. Accounts Receivable Turnover Ratio (AR Turnover/Receivable Turnover/Debtors Turnover Ratio)

It measures how efficiently and quickly a company converts its AR into cash within a given accounting period.

The formula for calculating the AR turnover rate for one year looks like this:

AR Turnover = Net annual credit sales/ Average AR

2. Current/Working Capital Ratio

It is the measure of liquidity, whether your company can pay short-term obligations with available cash or other liquid assets that can be converted into cash within a year.

The formula for calculating the current ratio for one year looks like this:

Current ratio = Current Asset/ Current Liability

3. Days Sales Outstanding (DSO)

It shows how long, on average, it takes customers to pay your company for goods and services.

The formula for calculating the DSO looks like this:

DSO = Accounts Receivable for a given period/ Total Credit Sales Number of days in the period

It may be tempting to relax the restrictions you have in place for giving your customers credit (also known as your credit policy or terms). This is only a temporary solution, frequently makes things worse than they get better, and might lead your business in the wrong direction.

How to improve Accounts Receivable?

If you want customers to pay cash more quickly or need more cash to grow, you can improve your AR in the following ways:

- Offer discounts to customers to pay quicker: The discount is an incentive for customers to pay the bill faster. For example, the company could offer a discount of 3% to pay in 5 days. More customers will be incentivized to pay the bill within 5 days by taking advantage of the offered discount.

- Give penalties for late payment: Besides giving discounts for early payments, impose penalties for customers who pay later than a specified period, such as adding a 30% penalty to the overdue amount.

- Use collection service: Instead of daily follow-ups for overdue payments, the company can employ a collection service to contact the customer and manage reminders for overdue payments on your behalf.

- Establish a line of credit from the bank: While waiting for payment, the company can secure a line of credit to enhance financial stability and address short-term cash flow needs.

While having a large customer base is beneficial, slow or non-payments from some customers can adversely affect your business's cash flow and financial health. One of the main causes of cash flow or liquidity issues for businesses is slow consumer payments.

Recording Accounts Receivable

After understanding the theory behind AR, we should learn how to record them. But first, we should know two different accounting methods: accrual-based accounting and cash-based accounting.

Accrual basis accounting is an accounting method based on revenue recognition principles and expense recognition principles.

- Revenues are recorded when earned

- Expenses are recorded when they are incurred to generate revenue

- Regardless of when cash is received or paid

Unlike the accrual basis accounting method, cash-basis accounting is based on cash flow.

- Revenues are recorded when cash is received

- Expenses are recorded when cash is paid

- Regardless of when the revenue is earned or the costs are incurred

Let's get to record in journal entries:

1. Record sales of services on a credit

When selling a service to the customer, the seller typically creates an invoice in the accounting system. It creates an entry into that credit sales account and debit AR account. The system will credit AR and debit cash when the customer pays the invoice.

For example, Company A buys equipment from Company B on credit for $ 1 million and promises to pay in 10 days. The journal entry is like the following:

| Debit | Credit | |

|---|---|---|

| Accounts Receivable | 1,000,000 | |

| Sales | 1,000,000 |

After Company A pays the bill, the journal entries are like this:

| Debit | Credit | |

|---|---|---|

| Cash | 1,000,000 | |

| Accounts Receivable | 1,000,000 |

2. Record sales of goods on credit

While selling goods to the customer, the seller will not only record sales on a journal entry but also record credit in inventory, which is on the assets of the balance sheet, and debit in cost of goods sold while it is on the expense of income statement.

For example, Company B sells a machine that costs $500,000 to Company A for $1 million. The journal entry is like this:

| Debit | Credit | |

|---|---|---|

| Accounts Receivable | 1,000,000 | |

| Cost of Goods Sold | 500,000 | |

| Sales | 1,000,000 | |

| Inventory | 500,000 |

After Company A pays the bill, the journal entry is like this:

| Debit | Credit | |

|---|---|---|

| Cash | 1,000,000 | |

| Accounts Receivable | 1,000,000 |

3. Record the discounts for early payment

As we mentioned before, a company can use a discount for early payment as an incentive to make customers pay earlier.

For example, Company ABC sells a machine to Company DEF for $ 1 million, and Company DEF promises to pay in 20 days. Company ABC offers a discount of 3% to pay in 5 days.

In 5 days, Company DEF will pay the full amount. We should record the following for Company ABC:

| Debit | Credit | |

|---|---|---|

| Cash | 970,000 | |

| Sales discount | 30,000 | |

| Accounts Receivable | 1,000,000 |

Researched and authored by Bill Tang | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?