Taxation

A systematic process of levying proportional financial charges on the incomes of individuals, businesses, and other entities.

What Is Taxation?

Taxation is a systematic process of levying proportional financial charges on the incomes of individuals, businesses, and other entities.

The government generates revenue by taxing the nation they represent on what they earn (income tax-related), buy (VAT, etc.), and own (property tax, etc.).

Taxes theoretically target wealthier individuals of a population who earn, buy, and own more than the majority. These funds are used to pay for social security, public services, programs, and projects that will benefit society to create a hospitable environment.

However, taxes are insufficient as some governments remain in a constant fiscal deficit.

Government bonds are considered a safe investment, given the issuing country is politically and economically stable. In addition, a nation’s deficits are usually financed using government bonds, enabling increased spending for the government to service the nation.

Acquiring debt relieves the government from raising taxes or reducing expenditures to keep within a budget, which would upset the population.

Fiscal policies must be moderated effectively, as harsh or unfair tax laws can destabilize the economy and cause a lack of faith in the government.

One example of this is Greece’s actions during the European debt crisis.

As for the strenuous debt the government accumulated, it was forced to impose austerity measures, increasing taxes and reducing government spending to direct more money to pay off its debt. Unfortunately, this was not favored by society, and a reduction in economic activity followed as a repercussion.

Eventually, Greece defaulted on its debt due to the structural limitations of its tax system, which was rife with tax evasion, significantly reducing government revenue.

- Taxation is how governments impose financial charges on individuals, businesses, and other entities to fund public services and government operations.

- The primary purpose of taxation is to generate revenue for government expenditures. Taxes also serve to redistribute wealth, regulate economic activities, and influence consumer and business behavior.

- Taxes can be classified into various types, including income tax, corporate tax, sales tax, property tax, and excise tax. Each type targets different sources of revenue and has distinct rules and rates.

- Tax evasion is the illegal act of not paying taxes owed, while tax avoidance involves legally minimizing tax liabilities through deductions, credits, and other means.

Taxation and government spending

Taxes and government bonds both contribute to government spending.

The primary objective of government spending is social security and development. The sectors serviced through government spending include education, healthcare, defense, social welfare, scientific research, and many more.

Spending usually focuses on two goals, to accommodate the current population’s requirements, primarily social welfare, and to progress future advancements by developing infrastructure and financing aspiring sectors, such as education for future employability.

Mandatory spending is constructed through the law to ensure that disadvantaged individuals are provided relief through entitlement programs—for example, low-income families who benefit from healthcare relief and food stamps.

The budget for mandatory spending in the U.S. has no limit, expanding to include all underprivileged nationals who fit the criteria.

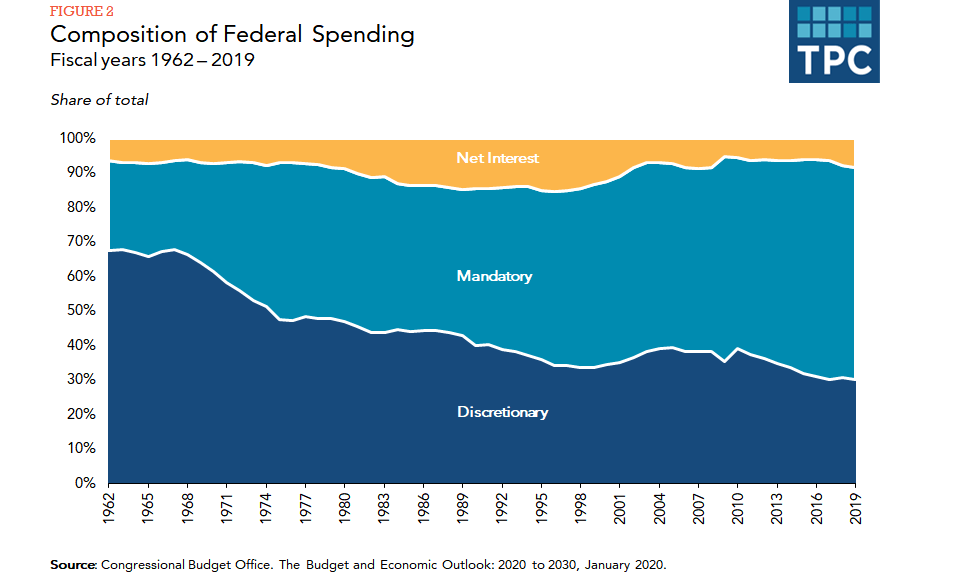

Mandatory spending had increased since 1962, contributing to 31% of federal spending. It now accounts for 62% of spending. In addition, a more significant demographic of elderly people and people with disabilities has increased social security and Medicare spending.

During this period, new programs, such as income tax credits (1975) and child tax credits (1997), have been institutionalized to uplift the burden on disadvantaged families.

Congress decides discretionary spending in the appropriation process to determine a budget and which sectors to allocate portions to each fiscal year. For example, the U.S. dedicates most of its discretionary spending to the military for national defense.

The discretionary spending budget has been reduced by a third since 1962, illustrating that mandatory spending has become more dominant/necessary.

Government Tax Authorities

The citizens of the U.S. are subjected to many different forms of tax by multiple government bodies, including federal, state, and municipal.

Federal taxes are imposed by the Internal Revenue Service (IRS), mainly taxing the income of nationals within the U.S. and money earned in the U.S.by foreign parties.

Federal income tax is progressive, levying income at different rates depending on the individual’s tax bracket. Therefore, the higher the salary, the more they must contribute to federal tax revenue.

Federal tax is acquired to help pay the nation’s bills; therefore, states impose their state taxes to cover expenses necessary for the state.

Federal income tax tends to be higher than state income tax, with some states legislating a constant tax rate for all incomes instead of a progressive tax. The nine states that do this are Colorado, Illinois, Indiana, Kentucky, Massachusetts, Michigan, North Carolina, Pennsylvania, and Utah.

States expect lower income tax revenue as they have more access to a concentrated group of taxes that generate revenue, such as property and sales taxes.

Taxes within different states are decided based on the demographics and infrastructure of the state, focusing on essential spending that is relied on to operate.

Municipal or local tax is more directed to local services such as education, emergency services, garbage disposal, etc.

The benefit of having constructed a system containing multiple government tax authorities is that spending is more optimized, with each governing body focusing on relevant areas to finance.

The drawback is that it results in more taxes for the public to pay, broadly spent at the federal level, and may not even benefit the taxpayer.

Tax Laws

There are many types of taxes that nationals are required to pay for the prosperity of their country.

Some of the main types of taxes are as follows.

Money earned

1. Individual Income tax

Also known as personal income tax, it is levied on the various forms of income an individual or household generates.

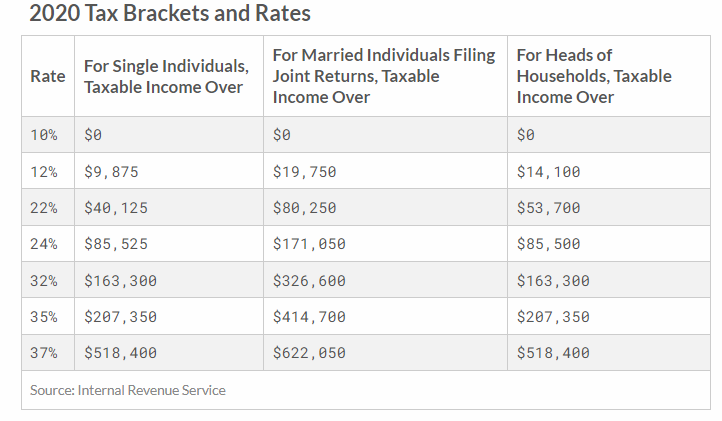

It is generally standardized as a progressive tax meaning the rate is proportional, in an ascending manner, to income earned such that higher-income earners pay more tax than lower-income earners.

The U.S. has organized income tax rates ranging from 10% to 37%, forming tax brackets with income corresponding to an appropriate rate. Income tax is collected above a specified threshold value.

2. Corporate tax

A tax on business profits, calculated as revenue made from sales, subtracted by business costs for its operation.

The two categories of corporate tax businesses adhere to are:

-

C corporations - A double taxation of business profits is imposed through corporate income tax and personal income tax to shareholders. Consumer prices and employee salaries are negatively adjusted to project greater business profits.

-

S corporations - Business profits may be passed to shareholders without corporate levies but are subject to individual income tax. In addition, company requirements entitle employees to a non-exploitative salary.

C corporations can hurt economic activity by discouraging potential investors; therefore, laws have placed a lower rate for corporate taxes to promote more economic activity and not deter consumers, employment, and investments.

The U.S. has decreased its federal corporate income tax rate to 21%, passed by the Tax Cuts and Jobs Act of 2017.

3. Payroll Taxes

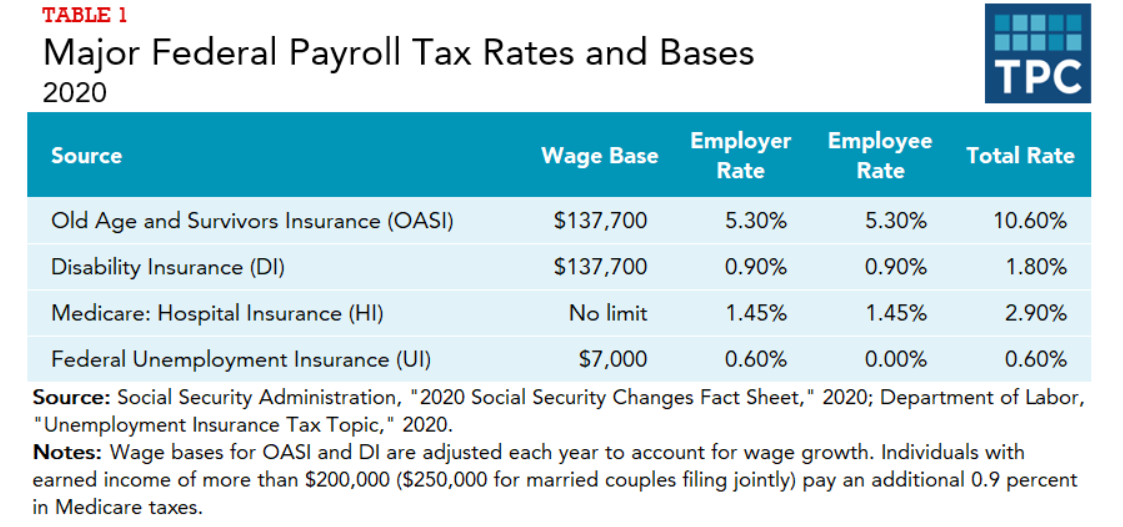

Like income tax, it is deducted from the employee’s and employer’s pay slips and is primarily used for financing social security, health insurance for Medicare, and unemployment insurance.

Old age and survivors insurance (OASI) is the largest payroll tax contribution at a rate of 5.3% for both employers and employees. OASI provides payments to the elderly and survivors, including surviving spouses and dependents.

The next largest is Medicare, which covers hospital and medical bills for the elderly, vulnerable patients with disorders, and lower-income individuals.

Federal unemployment insurance ensures benefits are received by those involuntarily made redundant in the workforce and conform to the conditions required by the insurance scheme.

Federal and state payroll taxes apply to workers, with state taxes varying in rates depending on relevant factors associated with benefits in the state.

Even though payroll taxes are equal among employees and employers, the fiscal burden often coincides with lower wages.

4. Capital Gains Taxes

Capital gains tax relates to the appreciation in the value of an owned asset that can be sold and generate a profit, for example, stocks, houses, jewelry, etc. The profits earned are liable against capital gains tax.

Stocks are acknowledged as double taxation, with the asset owned signifying partial ownership of a company.

Hence, business profits and gains made from the underlying stock are exposed to both the initial corporate income tax and applied capital gains tax levies, subjected to when the stock is sold at a higher value than when bought, as well as dividend payments.

Money Spent

1. Value-Added Taxes

A consumption tax is paid throughout the production line of goods and services at the value they are traded at.

VAT payments made by prior stages of the production line are deducted from the total value for the next sequence of VAT contributions. Still, they are incorporated into the product’s price.

Final consumers are charged VAT without any deductions in the price as a final consumption tax. This reduced the effects of tax pyramiding.

Most countries have implemented VAT, generating a large revenue on all taxable consumptions made within the country. However, the U.S. has not introduced VAT; instead, it has instituted two separate taxes, which act as an alternative to VAT.

These taxes are sales tax and gross receipts tax. Sales tax applies to the final consumer and is not required to be paid for by businesses that purchase goods and services to create their products.

Gross receipt tax is applied to the gross number of sales made by a business and is unrelated to profit, unlike corporate income tax. Therefore, it is presented as an unconventional taxation strategy with pyramiding effects, causing difficulty for lengthier production lines and early start-up companies with lower expected earnings.

2. Excise Taxes

An additional tax to the broad consumption tax is placed on goods and services. It forms a relatively small share of total tax revenue due to its specificity on the goods and services it applies. Common goods appropriated with the excise tax include tobacco, alcohol, gasoline, soda, and betting.

The tax exposes additional costs that may arise from the frequent use of the goods to offset any externalities that can result in side effects or repercussions not represented in the price of the goods.

For example, tobacco and cigarettes are imposed with excise tax to reduce the amount the population consumes and the costs it adds to the healthcare sector due to their addictive and health-deteriorating properties.

The amount an individual uses for an excise tax good can reflect how many other associated privileges they use. For example, the gas tax is a good indicator of how much a person drives on roads and, thus, how much they contribute to traffic congestion and road wear and tear. Therefore, the tax revenue could be used to help improve and maintain road infrastructure.

Money Owned

1. Property Taxes

As the name suggests, it’s a tax that is collected based on the immovable property you own, whether it’s the building or the land it is built on, and provides a large essential revenue to the state and local government.

It contributes up to 70% of the local government’s tax revenue to help fund public services such as emergency services, roads, and schools.

2. Estate and Inheritance Taxes

Both taxes come into play in the event of the death of an individual, with the taxes applying to the value of the deceased’s belongings. An estate tax is self-proclaimed before the remainder of the estate is distributed to their heirs, whereas the heirs pay inheritance tax.

The tax is unavoidable by pairing it with a “gift tax” that prevents any property transfer from being disregarded from taxation before the near-death of an individual.

These taxes have been discouraged in the U.S. as they are exclusive to the country’s or state’s “capital stock,” with wealth distributed along with descendants that enable them to remain productive and secure.

Hence, estate and inheritance tax would deter people from investing in the country’s wealth and resources, reducing growth and development.

Taxation And Tax Codes

Tax breaks for corporations and individuals are classed as tax expenditures for the government, as they reduce the amount of tax paid. As of 2020, tax expenditures cost the U.S. government $1.3 trillion, almost equivalent to discretionary spending.

Lawmakers craft tax codes to specify who can redeem the benefit and under what conditions.

Tax relief primarily benefits the wealthy, who contribute a large portion of their income to tax. Retaining more money encourages spending and business expansion, stimulating the economy.

The tax codes can favor certain industries to adjust the incentives for companies—for instance, relief for companies that display environmentally friendly measures or a low carbon footprint.

Tax avoidance is a legal method of bypassing income tax by utilizing tax codes written into the law by the U.S. Congress and approved by the president. In addition, taxpayers often use tax deductions to pay less money to the Internal Revenue Service (IRS) or claim credit to compensate.

Tax codes can manipulate how citizens behave, reaping the benefit of tax deductions and promoting behaviors such as securing health insurance and saving for retirement. This motivates citizens to pay less tax in the present to subsidize essential future services and accounts.

The complexity of the tax code system has made it more difficult for nationals to benefit from rightful tax exemptions, with some calling for tax codes to be simplified once again.

Tax evasion is a separate issue. This refers to illegal methods used to reduce tax payments to the IRS, such as falsifying your taxable income or claiming credit that a person is not qualified to receive.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?