Analyzing Berkshire’s Q4 Value Rotation: Energy, P&C Insurance, and Consumer Staples

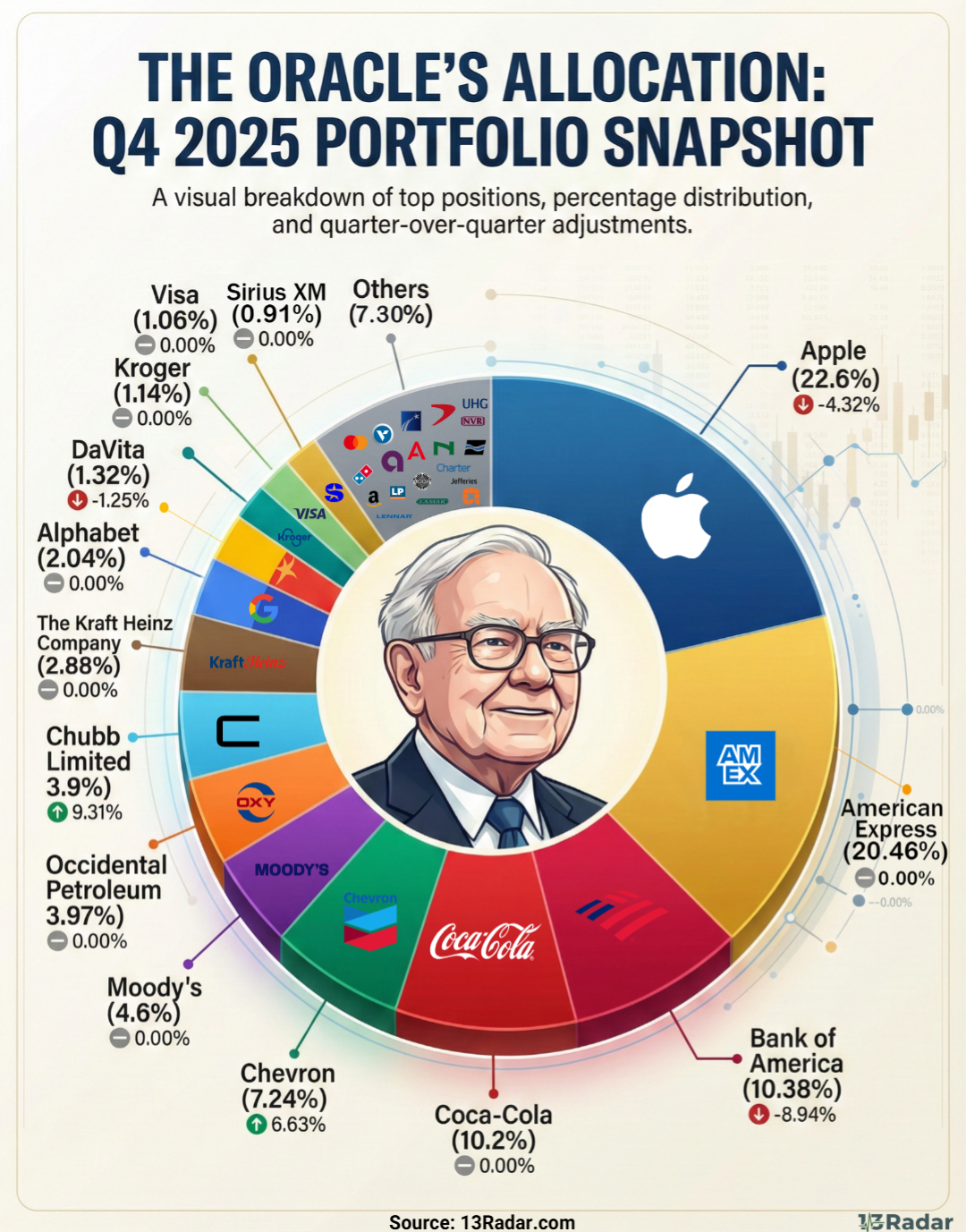

The Q4 2025 13F filings are out, and analyzing Berkshire Hathaway's recent capital deployment reveals a clear preference for tangible cash flows over high-beta tech multiples. While much of the broader market focus has remained fixed on hyperscalers and AI infrastructure, Berkshire spent the fourth quarter quietly allocating capital toward energy producers, property and casualty (P&C) insurers, and highly franchised consumer models. From a fundamental perspective, this marks a distinct rotation toward traditional value metrics and balance sheet resilience.

The Franchise Model Moat: Domino's Pizza (DPZ)

Berkshire has systematically built its position in Domino's Pizza over six consecutive quarters, adding another 12.3% in Q4 to bring the stake to over 3.3 million shares. Rather than a bet on consumer dining trends, this is a textbook capital-light franchise play. DPZ offers robust pricing power and an internal supply chain logistics network that generates highly predictable free cash flow (FCF). This allows for consistent share repurchases and dividend growth, insulating the equity from broader macroeconomic volatility and consumer softening.

Energy and Insurance: Bolstering Chevron (CVX) and Chubb (CB)

On the heavy industry and financials side, the institutional accumulation continued. The firm increased its Chevron (CVX) position by 6.6% (adding over 8 million shares), reinforcing energy as a core portfolio pillar with a weight exceeding 7%. Concurrently, Berkshire expanded its stake in property and casualty insurer Chubb (CB) by 9.3%. The strategic rationale here is straightforward: both operate in heavily consolidated industries with steep barriers to entry. More importantly, Chubb's P&C float provides Berkshire with structural advantages in a prolonged elevated interest rate environment, while CVX offers a strong dividend yield and structural inflation protection.

[ DATA HIGHLIGHT ] Portfolio Concentration and Defensive Positioning

Looking at the macro allocation strategy, the reliance on stable, cash-generating businesses is stark. A structural review of the Warren Buffett portfolio Q4 2025 illustrates that approximately 88% of the massive $274 billion public equity portfolio remains highly concentrated in just ten core holdings.

Key structural takeaways from the Q4 allocation:

- Float Monetization: The continued expansion into insurance underlines a preference for businesses that generate investable float at zero or negative cost.

- Yield Over Multiple Expansion: Capital is actively flowing away from high P/E tech names toward sectors that aggressively return capital to shareholders via buybacks.

- Inflation Resilience: Heavy allocations in energy and consumer staples highlight a defensive posture against sticky inflation data.

This Q4 rotation is a clear indicator that institutional capital is prioritizing earnings visibility and downside protection over speculative growth narratives heading into 2026.

Pariatur ad est voluptas commodi quo. Placeat blanditiis ratione corporis voluptatem ut. Amet at consequatur non similique in.

Error ipsam natus asperiores voluptatem consequatur. Ex accusantium voluptatum laudantium voluptatum placeat libero. Rerum quisquam qui non ipsa delectus commodi. Veniam hic temporibus debitis ut dolores. Consequatur voluptatum doloremque fugit quo esse dolor voluptas.

Omnis maxime ipsa et. At vel sed et dicta esse omnis. Odio quo numquam accusamus.

A ex voluptatem ea ad amet expedita. Repellendus doloribus et consequatur et sit molestiae tempora. Et quod aspernatur rerum voluptate. Natus velit totam est repellat dolore occaecati accusantium. Nostrum amet ut quos eligendi excepturi aut.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...