|

Broad Specifics

Welp, it was fun while it lasted.

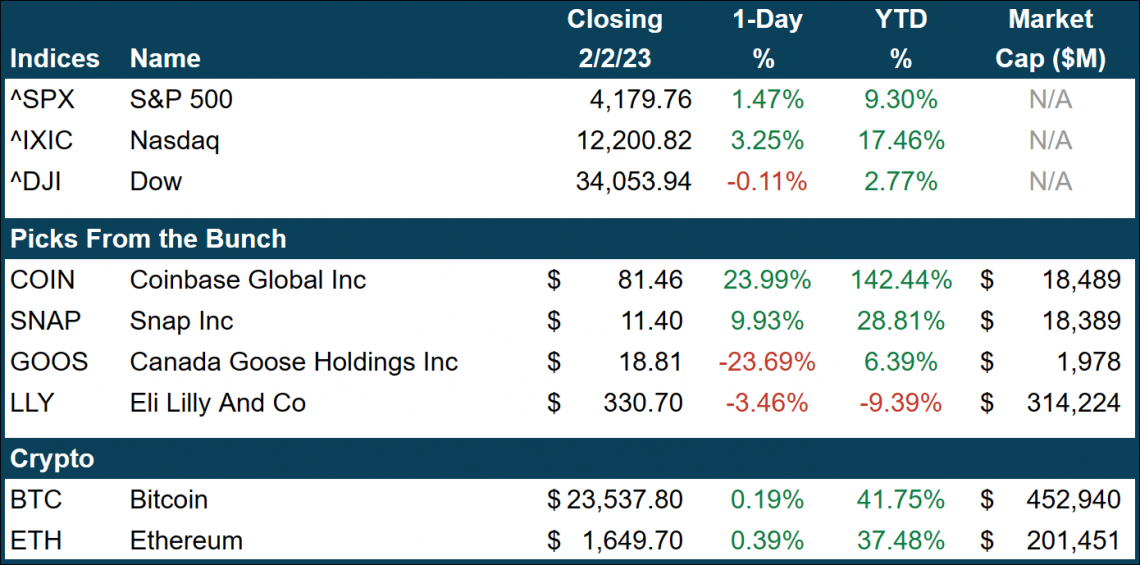

January got us off to a hot start. For the first time in far too long, we could actually check our portfolios without subsequently needing a Safe Space to go cry in. For example, we recently spoke about how January was on track to be (and actually was) the best month ever for Ark’s risk-drunk flagship fund, $ARKK.

Yesterday, the vibe shifted. All day long, everyone was getting pumped for three things; earnings from 1) Amazon, 2) Alphabet, and 3) the biggest dawg of them all, Apple. The numbers are out, and it’s only been after-hours (AH) trading thus far, but it’s an early indication that the fun might be over.

Those three companies alone represent ~$4.95tn in aggregate market cap, and they just so happened to report earnings on the same day. However, not only do these firms basically control US financial markets, but their numbers give us a broadly specific glimpse into the US as well as parts of the global economy. With no further ado, let’s take a look.

Amazon: I was sitting in the office yesterday at 4:04 pm when I saw the CNBC headline “Amazon beats on revenue…” blah blah blah. Great, I thought, until the next headline appeared, along with a flashing red background and an exceedingly disoriented-looking pundit apparently gasping for breath when it said, “Amazon misses on AWS revenue expectations.” I’m pretty sure bombs went off in Seattle.

At the time of writing, shares were off over 4% AH. No one cared that the firm’s top line of $149.2bn beat guesstimates by nearly $5bn, nor did they care that EPS clocked right in line with expectations. All the attention was on the segments themselves.

In particular, cloud is what mattered to investors. AWS sales gained 20% on the year, well below the growth posted by Microsoft’s Azure and just mildly below street estimates.

The other important line item here from a macro perspective is, of course, the online store sales. This segment contracted 2% on the year, contributing heavily to the firm’s slowest annual revenue growth ever as a public company (just 9%). But still, sales at Amazon.com remained ~44% above the same line item in 2019, which, to be fair, is the year we really should be comparing it to.

Alphabet: Never one to let Amazon steal the show, Alphabet joined its fellow quasi-monopoly in reporting some disappointing earnings late yesterday. Its shares were off 3.75% AH at the time of writing, but it’s very much a similar story.

Google Cloud, the current bronze medal holder in the Cloud Olympics, also disappointed on revenue by slightly more than $100mn. Not much compared to the firm’s $76bn in total revenue, but it just so happens that that aggregate sales number managed to miss as well.

Alphabet sits right at the crosshairs of two of the shakiest markets when it comes to economic downturns, cloud and digital advertising. Advertising is widely known to be one of the first costs cut when a company enters tough times. Cloud is nice, but it’s mostly not essential for small/medium businesses. So, it’s no wonder why investors are down so bad right now.

YouTube was the real disappointment, however. Another victim of the volatile digital ad space, sales came up hella short despite the expectation that Shorts would finally stand up to Tiktok’s dominance. Spoiler: it did not.

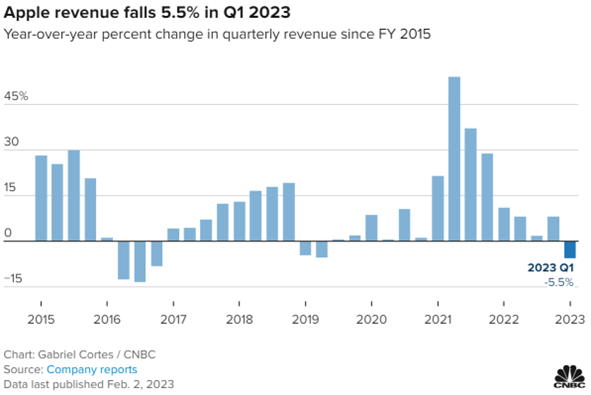

Apple: Meanwhile, Tim Apple and the team managed to miss on both the top and bottom lines. EPS and revenues came up short at the US’s largest company, but it kinda only got worse the closer you looked.

See, Apple sells a little-known product called the “iPhone,” and sales absolutely sucked for this thing over the quarter. Largely due to production delays at its China-reliant factories, the lack of iPhone slingin’ was entirely a supply issue. I’d say that bodes well, as it shows resilient demand for the luxury product, but the key to Apple’s success since the passing of Steve (RIP) has been stellar supply chain management. Timmy boy might’ve dropped the ball on this one.

Almost every line item came up short, except (weirdly) iPad sales. Despite this lone bright spot, guidance from the CFO indicates double-digit declines in this and Mac segments. The firm still isn’t providing numerical guidance, but they did say they expect a “similar declining trend” in Q1’23.

This is a wild one because Apple simply doesn’t miss, but they did this time. Pairing the big dawg’s results with Google and Amazon spells out one thing: demand is slowing down from both businesses and consumers.

We saw from the chipmakers that PC sales were weak AF in Q4, and along with Snapchat and Meta, it looks like digital ad spend from businesses is following a similar trajectory.

Well, JPow, you’ve officially killed demand. I hope you’re happy.

|

Eos et eos voluptatibus consequuntur rerum tempore. Quam nulla voluptatibus similique. Magni est quia fugiat in. In pariatur aut voluptatem necessitatibus earum. Ut corrupti rerum qui aspernatur rerum.

Laboriosam a blanditiis ut quo quia inventore vel. Aut et sed blanditiis id mollitia sit at.

Sit et aut natus saepe architecto. Et consectetur aut perferendis unde ab sint eius in. Ipsam dolores quia ut sit.

Qui totam officia doloremque et dolorem consectetur. Quae consequatur nam qui et iste quia. Velit corrupti adipisci maiores omnis accusantium qui. Sint dolores pariatur et earum dolore. Enim dolorem rem ad maxime libero iste praesentium. Quis assumenda nihil excepturi incidunt error dicta a provident. Quidem iure illum reiciendis explicabo ut ad quis.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...