Case Study: The "Zurich Model" – Structural Alpha via Environmental Design

In the high-velocity world of Long/Short equity, "edge" is typically associated with information speed—proprietary data feeds, expert networks, and sub-second execution. Guy Spier’s Aquamarine Fund offers a contrarian case study: the generation of alpha through the deliberate removal of market noise.

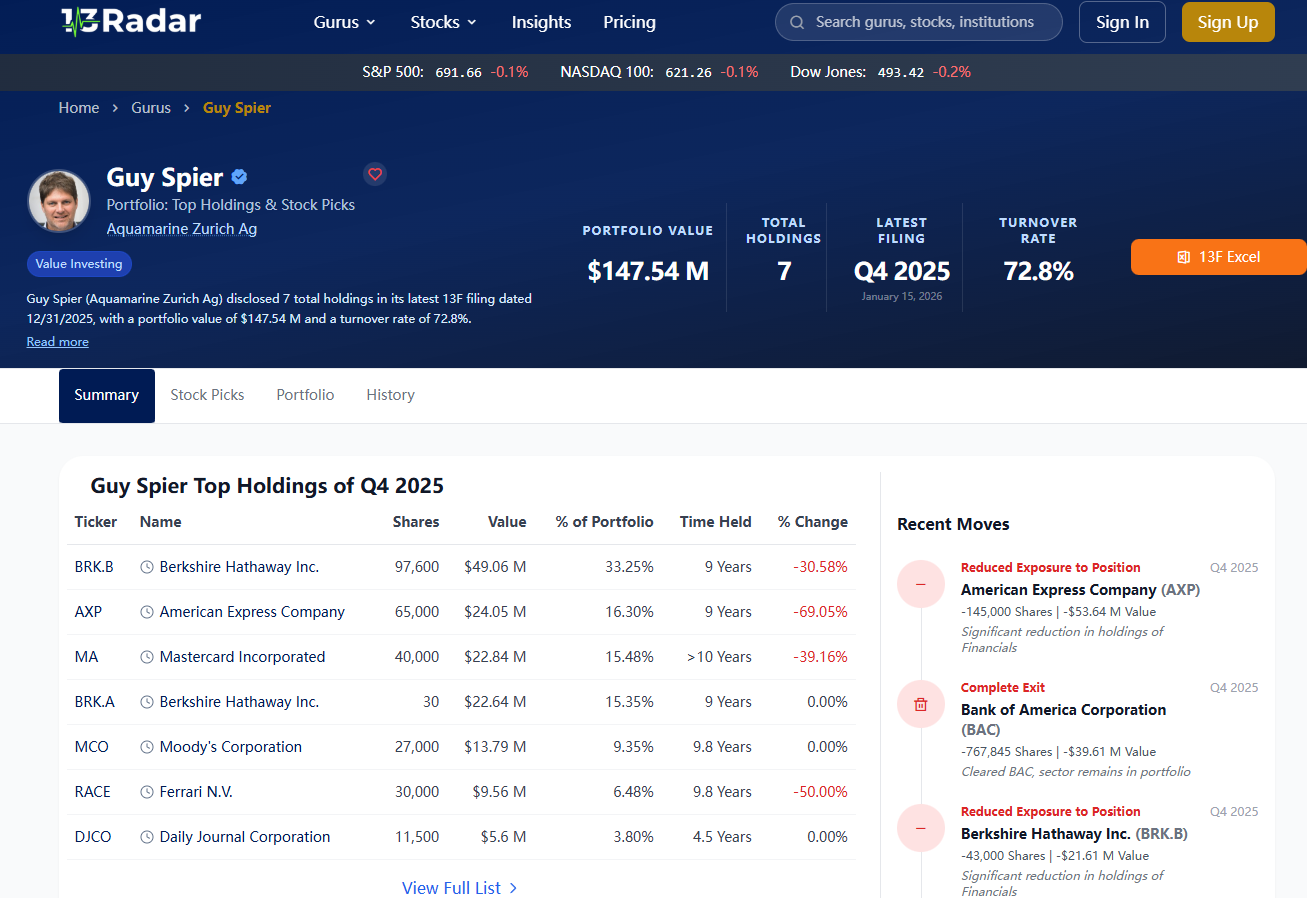

Operating out of Zurich, far from the feedback loops of New York or London, Spier has constructed a portfolio that prioritizes low turnover and high Return on Invested Capital (ROIC). An examination of the current guy spier portfolio reveals a strategy that is less about stock picking and more about "environment design" to mitigate cognitive bias.

1. Portfolio Concentration and the "Inevitable" Moat

Unlike diversified mutual funds that hug the index, Spier’s allocation is characterized by extreme concentration in businesses with duopolistic characteristics. The distinct preference for credit rating agencies (Moody’s/S&P) and luxury stalwarts (Ferrari) highlights a focus on pricing power.

From a portfolio construction perspective, this is a bet on inevitability over probability. In a high-inflation regime, the credit rating agencies possess a natural hedge—their revenues scale with nominal debt issuance volumes without requiring incremental capital investment. This "capital-light compounder" thesis allows the fund to maintain multi-year holding periods, effectively reducing the tax drag that typically erodes net returns in high-turnover funds.

🛑 The "Checklist" Protocol

Spier’s methodology (influenced by Munger and Gawande) relies on a pre-trade checklist designed to bypass emotional triggers. Key constraints include:

- No Management Access: Rejecting the standard industry practice of meeting CEOs to avoid "liking" biases.

- Market Hours Blackout: Avoiding price checking during trading hours to prevent reactive decision-making.

- Post-Event Analysis: Analyzing 13F data only after a significant time lag to filter out herd behavior.

2. Berkshire Hathaway: The Cash Proxy Thesis

A notable anomaly in the fund's structure is the significant allocation to Berkshire Hathaway (BRK.B). For institutional allocators, paying fees to a manager who simply holds another conglomerate is often a point of contention.

However, within Spier’s framework, Berkshire appears to function not as a high-beta equity, but as a yield-bearing cash substitute. It provides a floor to the portfolio’s volatility while retaining optionality on capital deployment. This structural decision allows the fund to remain fully invested rather than holding fiat cash, which suffers from negative real yields. It challenges the traditional 60/40 allocation model by using a conglomerate balance sheet as the defensive anchor.

3. The Valuation of "Inactivity"

The industry standard for measuring productivity is often activity—trades per day, meetings per week. Spier’s track record suggests that inactivity, when applied to high-quality assets, can be a source of outperformance.

By removing himself from the "Bloomberg Terminal culture," the strategy minimizes unforced errors caused by short-term volatility. The portfolio turnover rate remains exceptionally low, aligning with the philosophy that the bulk of investment returns are generated by the asset's internal compounding, not by the timing of the entry or exit. This "Zurich Model" stands as a distinct alternative to the operational intensity typical of modern hedge funds.