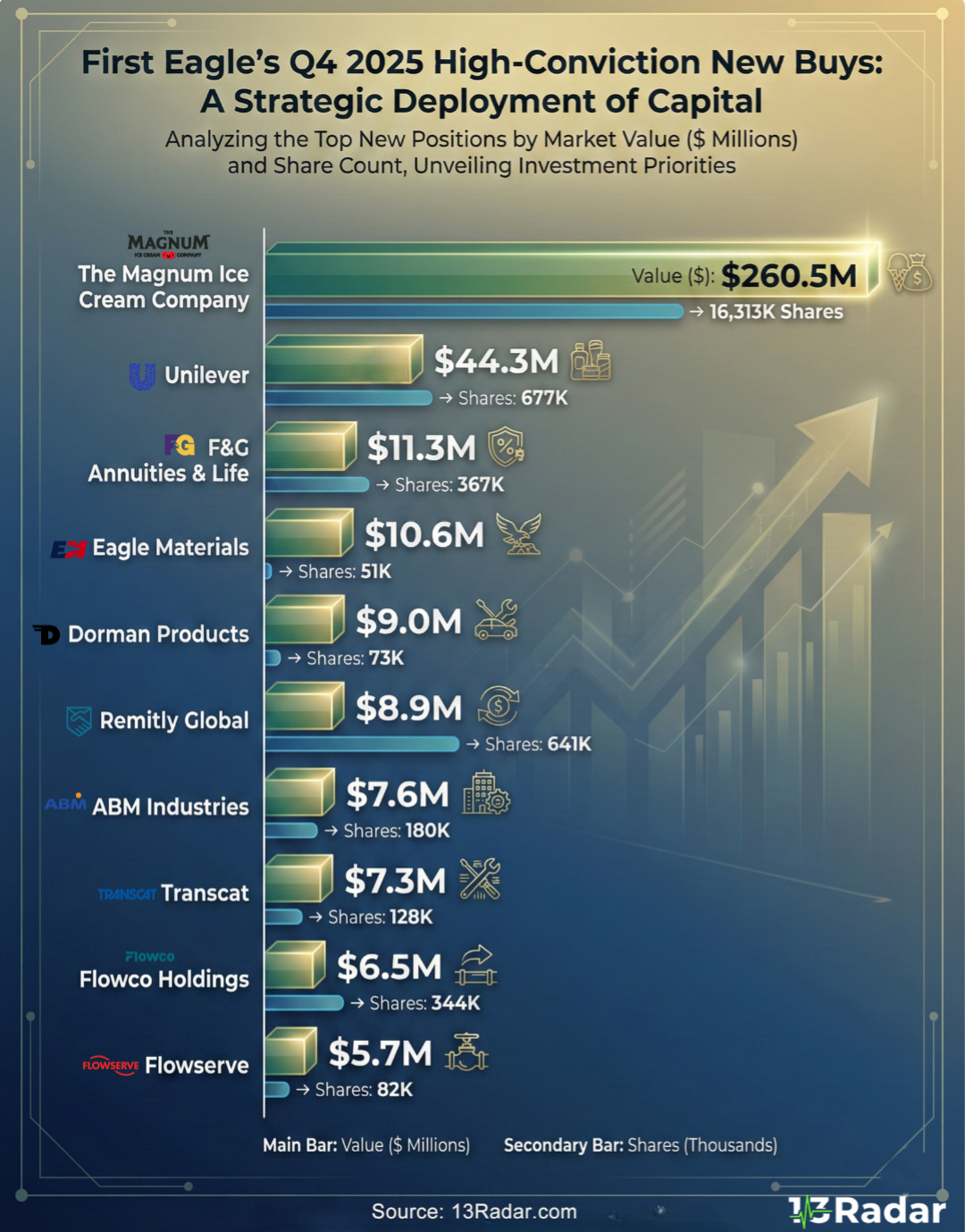

Deconstructing First Eagle’s Value Factor Exposure in Q4

For those tracking institutional capital flows, the divergence between growth and value factors has been the defining narrative of early 2026. While momentum strategies have dominated recent headlines, a look at the fundamental positioning of long-standing value shops offers a different perspective on the current cycle. Specifically, First Eagle Investment Management’s latest filing provides a case study in defensive portfolio construction amidst elevated valuations.

First Eagle has historically operated with a mandate focused on absolute returns and capital preservation rather than strictly tracking relative benchmarks. Their Q4 activity appears to double down on this philosophy, prioritizing margin of safety over beta expansion.

Sector Allocations: A Hedge Against Inflation Stickiness

The institutional consensus has largely priced in a "soft landing," but First Eagle’s allocation suggests a hedging strategy against potential stagflationary pressures. Unlike pure-play equity funds, their mandate allows for significant exposure to real assets, specifically gold and precious metals, as a proxy for currency debasement protection.

Analyzing the data from the First Eagle Investment portfolio Q4 2025, we observe a distinct preference for businesses with tangible assets and pricing power. The rotation is less about "sector picking" and more about identifying companies with durable Free Cash Flow (FCF) yields that can withstand a higher-for-longer rate environment. This contrasts sharply with the duration risk currently embedded in many tech-heavy portfolios.

⚡ VALUATION DISCIPLINE: Intrinsic Value vs. Market Price

First Eagle’s methodology, deeply rooted in the Eveillard tradition, relies on a strict discount-to-intrinsic-value framework. In the current market, where the S&P 500 implies significant earnings growth, their 13F filings often reveal where they believe the market has mispriced risk.

Notable observations in their recent activity include:

- Cash Accumulation: Monitoring their cash weighting is critical. An increase in cash reserves typically signals a lack of qualifying investment opportunities offering a sufficient margin of safety.

- International Arbitrage: A continued overweighting of non-US equities, suggesting they see better risk-adjusted returns in European or Asian markets compared to domestic large-caps.

- Trimming Winners: Evidence of selling into strength, adhering to sell disciplines when price converges with their calculated intrinsic value.

Distinguishing "Temporary Impairment" from Structural Decline

One of the more technical aspects of observing First Eagle’s 13F is their entry points into distressed names. The fund has a history of stepping into equities suffering from what they deem "temporary impairment" rather than permanent capital destruction.

This approach requires distinguishing between cyclical headwinds and structural obsolescence. Their Q4 positions likely reflect a contrarian view on specific industries that the broader market has discarded. For analysts, these moves provide data points on which sectors may be nearing a cyclical bottom based on institutional valuation models.

Rerum dolor blanditiis dolore enim architecto aliquam quo necessitatibus. Praesentium expedita harum explicabo voluptatem esse labore. Et aperiam quaerat maxime aliquid a sunt. Doloremque excepturi quam neque consequatur mollitia non odit. Consequatur facere omnis dignissimos cupiditate ad ad. Ad nesciunt aliquam quasi.

Voluptatibus sunt iusto dicta quam. Et modi nulla exercitationem ad quia aliquam necessitatibus nesciunt. Minima aut earum quod repellat. Eligendi architecto molestiae et illo id. Consequatur atque omnis perspiciatis rem commodi et magni.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...