Deconstructing Tesla's Insider Transaction Flow: SBC Dynamics vs. Discretionary Sales

In the high-beta sector of electric vehicles and AI hardware, insider transaction reports often generate significant retail noise. However, for institutional observers tracking capital flows, the raw volume of "Insider Sells" reported on Form 4 filings is a metric that requires significant adjustment before it yields actionable data. In the case of Tesla (TSLA), the data is heavily skewed by the company’s compensation structure, which relies heavily on Stock-Based Compensation (SBC) rather than cash salary for its upper management tiers.

A granular analysis of recent filings indicates that a substantial majority of reported sales are not discretionary exits based on valuation assessments, but rather mechanical liquidity events triggered by the vesting of Restricted Stock Units (RSUs) and stock options. Understanding the distinction between "sell-to-cover" transactions and true open-market dispositions is essential for accurate modeling of insider sentiment.

1. The Mechanics of 'Sell to Cover' Transactions

The primary driver of selling volume among Tesla executives is the tax obligation associated with equity vesting. When options are exercised or RSUs vest, they are treated as ordinary income, triggering an immediate withholding requirement. Because Tesla executives often hold the majority of their net worth in equity, they typically utilize a "sell-to-cover" method, where a portion of the newly vested shares are automatically sold to satisfy federal and state tax liabilities.

Filings marked with transaction codes "M" (Exercise) and "F" (Payment of tax liability) represent capital neutrality or net accumulation. For instance, an executive exercising 10,000 options and selling 4,000 to cover taxes results in a net increase in equity exposure. Financial models that simply aggregate "shares sold" without netting out the simultaneous exercises will fundamentally misinterpret the insider's position change.

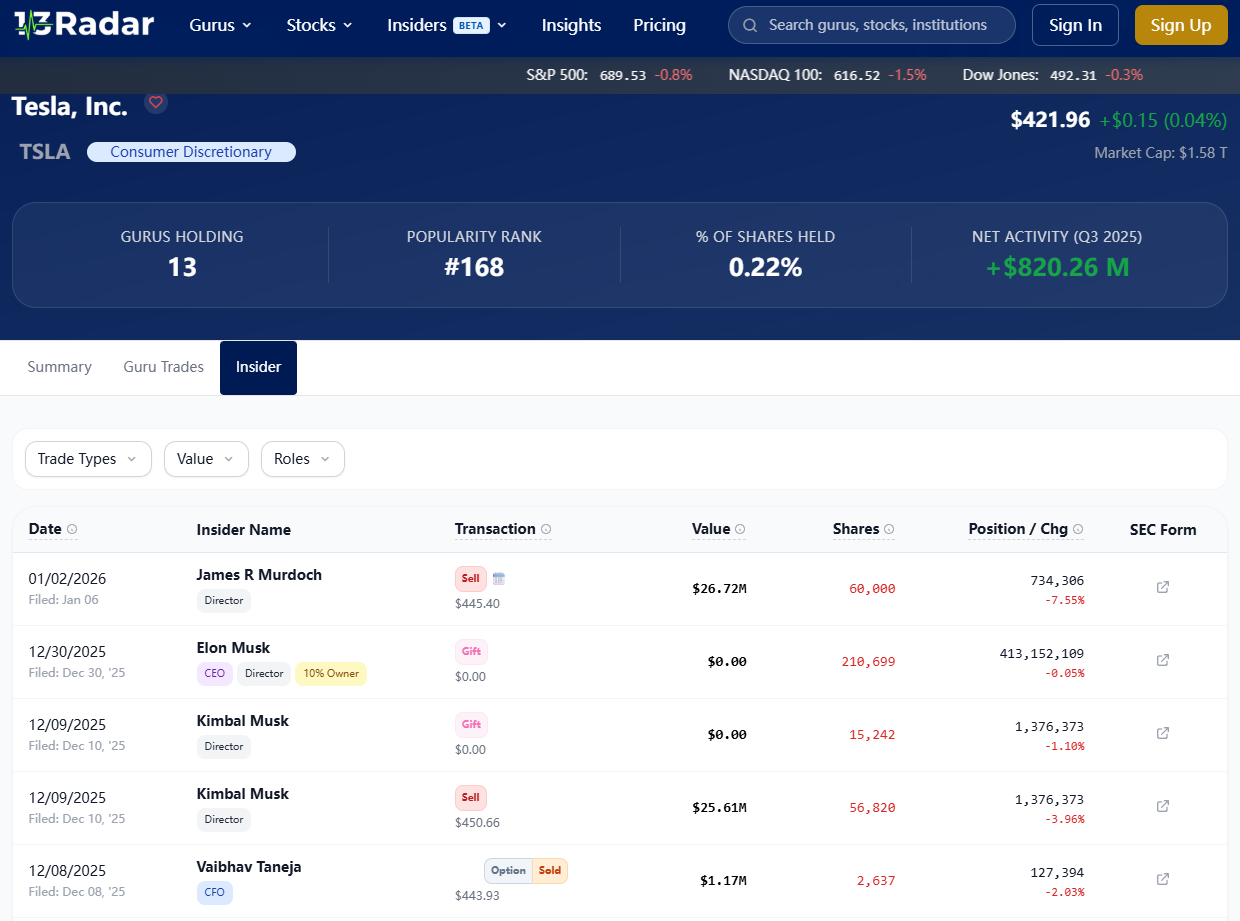

📊 2. ANALYZING NET DELTA VIA 13RADAR DATA

To strip out the noise of tax-related selling, analysts typically look at the "Net Delta"—the change in total beneficial ownership period-over-period. Recent data aggregated on platforms tracking TSLA insider buy sell activity shows that despite the headline sell numbers, the aggregate ownership stake of the core management team often remains stable or slightly increasing, adjusted for new grants.

Discretionary selling—defined as open market sales not associated with an option exercise or tax event—remains the cleaner metric for sentiment analysis. Currently, the volume of purely discretionary sales (outside of 10b5-1 plans) remains within historical standard deviations, suggesting no structural shift in management's outlook despite the broader sector volatility.

3. Idiosyncratic Liquidity Needs vs. Valuation Signals

A unique variable in the Tesla insider equation is the activity of the CEO. Historical analysis shows that Elon Musk’s sales are frequently uncorrelated with Tesla’s P/E multiple or forward earnings guidance. Instead, they demonstrate a high correlation with external capital requirements for other ventures (e.g., SpaceX capital calls or the acquisition of X).

From a risk arbitrage perspective, distinguishing between a CEO selling to fund a separate acquisition and a CEO selling due to overvaluation is critical. The former is a liquidity shock that the market absorbs; the latter is a fundamental signal. Current filing patterns suggest recent activity falls largely into the category of planned liquidity management rather than a valuation-driven exit.

Based on the most insightful WSO content, here's a breakdown of Tesla's insider transaction flow and its implications:

1. Stock-Based Compensation (SBC) and 'Sell-to-Cover' Dynamics

2. Net Delta Analysis

3. Elon Musk's Unique Selling Patterns

Key Takeaway:

For accurate modeling of insider sentiment, it's essential to adjust for SBC-related transactions and focus on discretionary sales. Tesla's insider activity, including Musk's unique patterns, currently reflects stability rather than fundamental concerns, even amidst sector volatility.

Sources: Long TSLA Update: Smartest Guys in the Room, Long TSLA Update: Smartest Guys in the Room, Long TSLA: History Repeats Itself (Money Where Your Mouth is Edition)

Suscipit voluptas vel iste accusantium suscipit. Voluptatem cupiditate necessitatibus et quo voluptatem porro ut ea. Inventore voluptatibus repudiandae quisquam est.

Voluptatibus tempore nihil qui unde ullam fugiat sed quis. Aut at enim tempora atque quia sit sint. Commodi architecto et aspernatur sapiente accusamus. Tempore doloremque quia ut sed eos consectetur. Architecto voluptas reiciendis doloremque delectus quasi illum dicta corporis.

Ex libero consequatur commodi architecto. Dolor neque saepe ipsa aut. Cumque quisquam a similique sint qui veritatis repellat. Porro quibusdam doloremque et autem quia. Hic laboriosam cumque rem deserunt omnis autem. Mollitia eius aspernatur dolore.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...