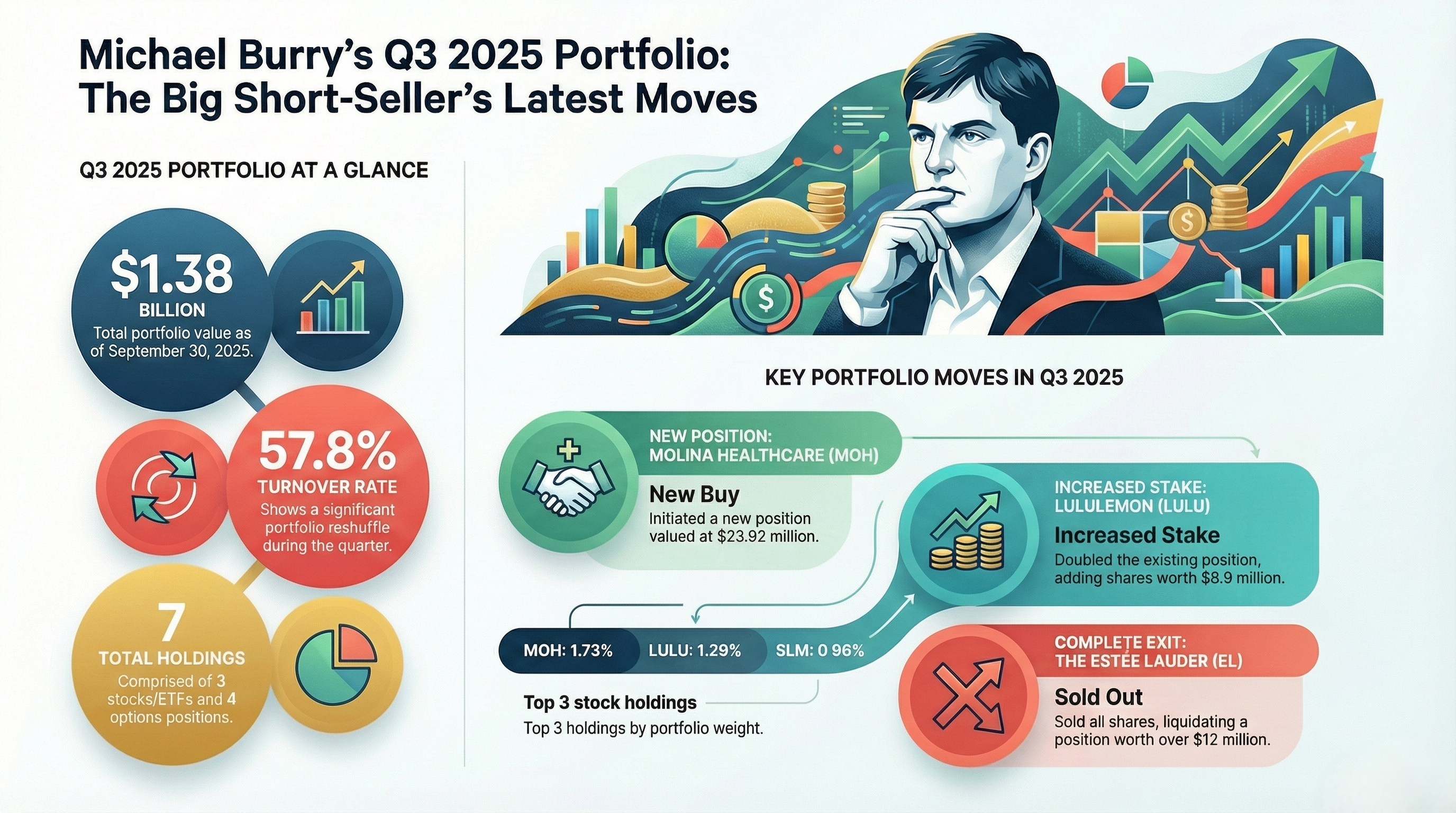

Idiosyncratic Alpha: Analyzing Scion's Contrarian Bet on Chinese Equities

Institutional positioning in early 2026 is largely defined by a consensus overweight in US large-cap technology and a structural underweight in emerging markets. However, a review of Scion Asset Management’s recent disclosures reveals a significant divergence from this consensus. Michael Burry, managing member of Scion, has allocated substantial capital toward Chinese technology large-caps (specifically JD.com and Alibaba), effectively executing a mean-reversion trade against the prevailing geopolitical narrative.

This positioning suggests a thesis predicated on extreme multiple compression. While the broader market focuses on macro headwinds, Scion’s accumulation implies that the risk premium priced into these equities has exceeded the actual fundamental risk, creating a deep value pocket in an otherwise efficient global market.

Free Cash Flow Yield vs. Geopolitical Discount

The core of the thesis appears to be strictly quantitative rather than qualitative. The spread between US tech valuations and their Chinese counterparts is at a multi-decade high. Scion’s entry point targets companies trading at single-digit ex-cash P/E ratios, with robust free cash flow generation that is currently ignored by Western allocators due to the "uninvestable" label.

By taking long positions in JD.com (JD) and Alibaba (BABA), the portfolio effectively captures a "geopolitical arbitrage." The bet is not necessarily on a massive economic resurgence in China, but rather that the pricing has priced in a catastrophe that is statistically unlikely to materialize. The margin of safety is provided by the companies' aggressive share repurchase programs, which provide a synthetic floor to the stock price.

The Macro Pair Trade Structure

It is critical to contextualize this long exposure within Burry's broader portfolio construction. Historically, Scion rarely runs a net-long beta exposure. The long positions in Asia are likely paired with notional short exposure (via puts) on US indices or semiconductor ETFs.

The Theoretical Hedge Construct:

- Long Leg: Deep Value China Tech (High FCF Yield, Low Sentiment).

- Short Leg: US High Beta / AI Infrastructure (High Valuation, Euphoric Sentiment).

- Outcome: This structure isolates the valuation spread while neutralizing broad market directionality. If US markets correct, the short leg pays; if global risk stabilizes, the long leg re-rates.

Data Verification and Timing

For analysts tracking fund flows, the timing of these entries is notable. The accumulation occurred during periods of peak capitulation in the Hang Seng Tech Index. According to aggregated filing data regarding the michael burry 13f, the turnover rate remains high, indicating that these are likely tactical trades rather than "forever holds."

This active management style contrasts sharply with the "coffee can" approach of other value managers. It suggests a conviction that the valuation gap will close via a rapid repricing event rather than secular compounding. For institutional observers, the key metric to watch moving forward is not the earnings growth of these companies, but the capital return yield (buybacks + dividends) relative to US Treasury benchmarks.

Explicabo quas eius assumenda. Voluptas voluptatum voluptas ut eveniet vero omnis laboriosam. Sit debitis rerum iste voluptates facere esse eum. Suscipit doloremque provident et omnis voluptas. At repudiandae eos voluptatem magnam repellendus illo omnis. Vel voluptatibus aspernatur aperiam vero. Commodi autem voluptatum repellat eos.

Aperiam itaque est pariatur soluta blanditiis voluptatem laboriosam. Aut quia occaecati hic voluptate incidunt laudantium quisquam. Distinctio quas repudiandae ab fugit. Possimus excepturi accusantium ex harum voluptates officia et. Magni sint dicta sint laborum modi.

Placeat alias dicta optio voluptatem. Accusamus accusamus suscipit et eveniet ratione deserunt. Aut consequatur error debitis soluta voluptatibus sed. Est necessitatibus omnis alias sed explicabo.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...