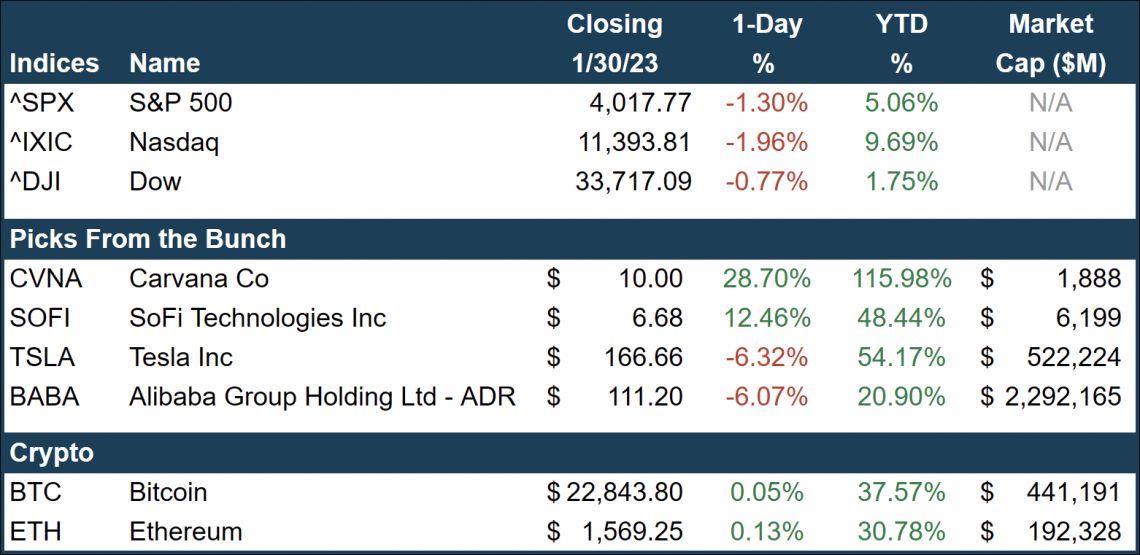

|

PCE Says PeaCE to Inflation

Fingers crossed, I don’t deeply regret that section title a few months (or weeks) from now…

But hey, we’ll run with it. JPow and the gang begin their first of 8 FOMC meetings of 2023 later today, and you better believe this is THE most important one ever (until the next one, of course).

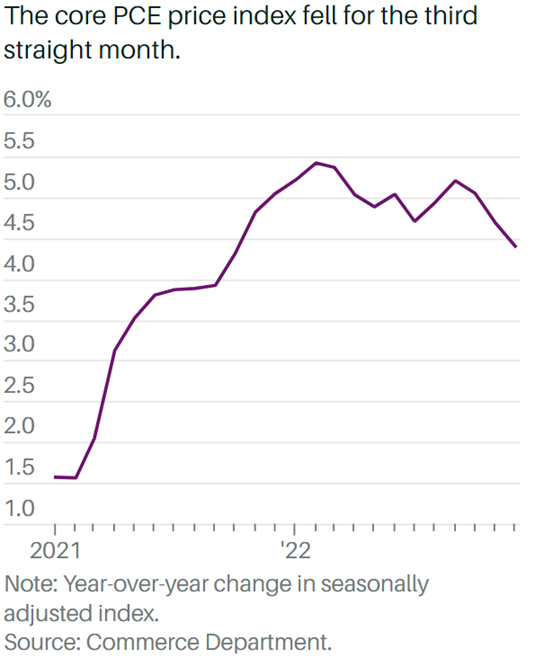

To celebrate the first macro Holiday of 2023, let’s check in on inflation. To close out last week, the Bureau of Economic Analysis blessed us with the Fed’s preferred measure of inflation, known as the Core Personal Consumption Expenditure (PCE) Price Index, or Core PCE deflator if you want to sound cool and smart.

To sum it up / dumb it down (whichever you prefer), it’s basically CPI stripped of the volatility of energy and food commodity prices. Yes, those are arguably the two most important expenses to Americans, but they also just so happen to be among the most volatile. After all, we’re not here to make sense; we’re here to make cents.

Core PCE came in smack-dab in line with economists’ expectations, posting price accelerations of 4.4% annually for the month of December. That’s the lowest level since wayyyy back in October 2021 and a 0.3% fall from November’s 4.7%. December’s numbers also mark 3-months in a row of decline. That’s officially a streak, baby!!

Unlike your career, we appear to be moving in the right direction. Following the reports, CME’s goated Fed Watch tool, which tracks market-implied probabilities for the size of the next rate hike, spiked to nearly 100% odds of a measly little 25 bps hike. This is almost definitely what was already priced in any way, but it’s nice to see the confirmation.

But as always, Mr. Market still has something to be afraid of. Just as we get inflation to maybe, hopefully, start to subside, investors became trepidatious over the now suddenly increased likelihood of a 2023 recession. Seemingly on a daily basis, depending on the data released from D.C., the market flip-flops between soft landing and outright recession as the year’s baseline expectation. Isn’t investing fun?

As your net worth hangs in the balance, the world will be hanging on every last syllable and its associated tone coming from the old, gray mouth of Jerome Powell. Driving this heightened fear is something we’ve touched on before: monetary policy lags.

The Fed’s tools to regulate the economy are okay, but they’re not the best. It’s like hanging drywall with nails rather than screws…it kinda works, but we can do better.

Raising rates is no different. The cost of money becomes elevated, drying up liquidity, which acts almost like a Butterfly effect and takes its sweet time to spread throughout the economy.

Repo rates feel the effects immediately, but a home remodeler in South Dakota feels the effects much slower as his customers slowly become more and more apprehensive about renovations as their borrowing rates rise.

The elasticity of the cost of money causes a chain reaction that slows growth like an airplane after landing rather than you slamming on the brakes inches in front of a red light.

This is the real trickle-down economics, and it’s scaring Mr. Market. The worst part is we can’t know if we’ve gone too far until we do. But 2022 saw the fastest rise in rates in US history, so maybe Mr. Market is right to be a bit skittish.

|

Voluptas eaque voluptas sapiente consequatur. Placeat soluta voluptas maiores quis.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...