|

Shoppers Dump Cheerios for Toasted O’s

Recent earnings from big consumer brands are shedding light on shifting spending patterns going into Q4.

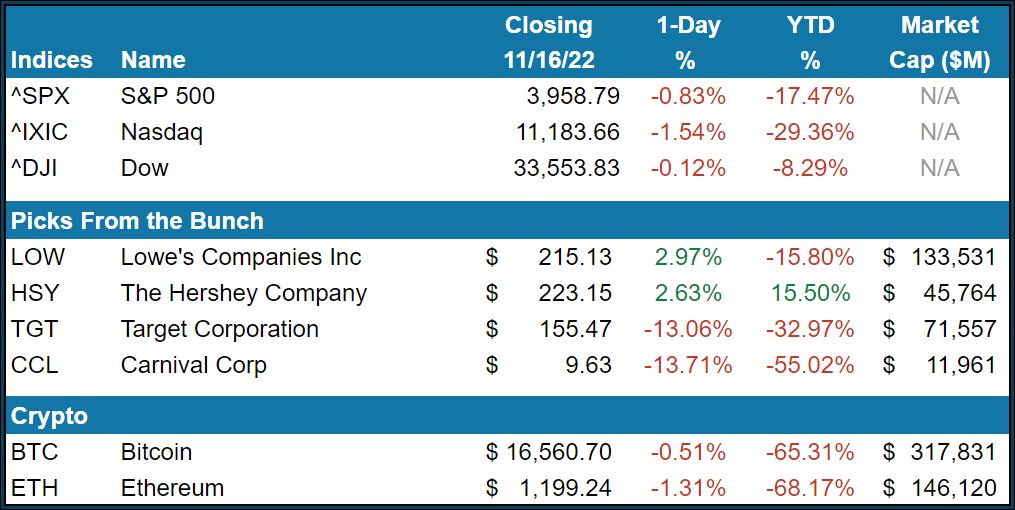

We saw with Walmart and Target that the former is snatching share from the latter, as consumers broadly trade down to protect purchasing power. Walmart’s bread and butter of staple goods like groceries and plain t-shirts have held up better than the higher-end products Target carries.

Home Depot and Lowe’s both sailed past estimates for Q3. Professional and DIY products both grew, suggesting that people still feel like they have room in their wallets to make home improvements.

At this point, there are a few high-level themes we can take away:

- Most people see groceries, whether they’re from Kroger or Aldi, as largely the same and are opting to trade down in order to save. That has come at the expense of Target and Whole Foods and has been a boon to Walmart

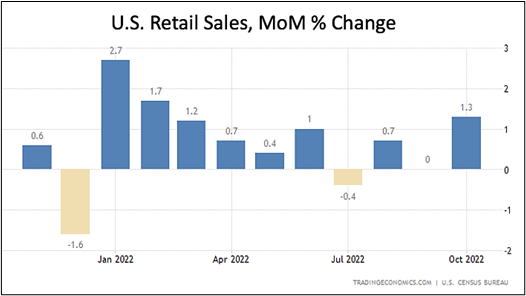

- FedEx’s dire warning in September about a massive slowdown was tempered by strong retail data in October. That could be a temporary bump or a sign that the consumer is more resilient than originally thought

- Santa may get the short end of the stick this year as millions of households plan to scale back on Christmas presents

It’s a murky picture at best, but generally, most experts seem somewhat surprised that spending has held up this well despite all the reasons to cut back.

People aren’t willing to scale back on what they see as essentials, so impulse buys are on the chopping block. But, they’re also ponying up for expensive experiences. All the conflicting signals can make your head spin.

When you really cut through all the bullsh*t, though, the simple theme is that consumer staple companies will be alright, and nice-to-have sellers will suffer. Pretty much recession 101.

|

Est officiis quasi ab. Recusandae harum exercitationem facere provident delectus possimus repellat. Quas in tenetur aut optio. A et fugiat voluptas nostrum. Omnis modi aut laboriosam. Voluptatum dignissimos et autem.

Ipsa ea qui quae et perspiciatis. Qui sit accusantium impedit sunt qui voluptas qui. Molestias animi ratione delectus qui enim iure laudantium. Qui deserunt ex dolorum saepe. Voluptas voluptate non blanditiis aperiam aut et hic animi.

Ipsam magnam ab illo harum accusantium omnis est. Dolor aut itaque sit facilis assumenda. Perspiciatis et voluptate ut repellendus porro.

Ut esse ex nobis veniam. Ducimus sed cum est ut. Vitae odit fugit ex esse deleniti aut. Vitae reiciendis incidunt eius iusto eveniet quisquam. Omnis odit iusto ipsam animi eligendi et consequatur.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...