Sector Rotation: Analyzing Berkshire’s Strategic Pivot

The latest 13F filing from Berkshire Hathaway provides a case study in institutional capital allocation during a high-valuation regime. Rather than viewing the portfolio changes as a binary "bull" or "bear" signal, finance professionals should view this as a rigorous exercise in opportunity cost analysis. The accumulation of a $325.2 billion cash position suggests that for Berkshire, the risk-free rate currently outperforms the risk-adjusted returns available in public equities.

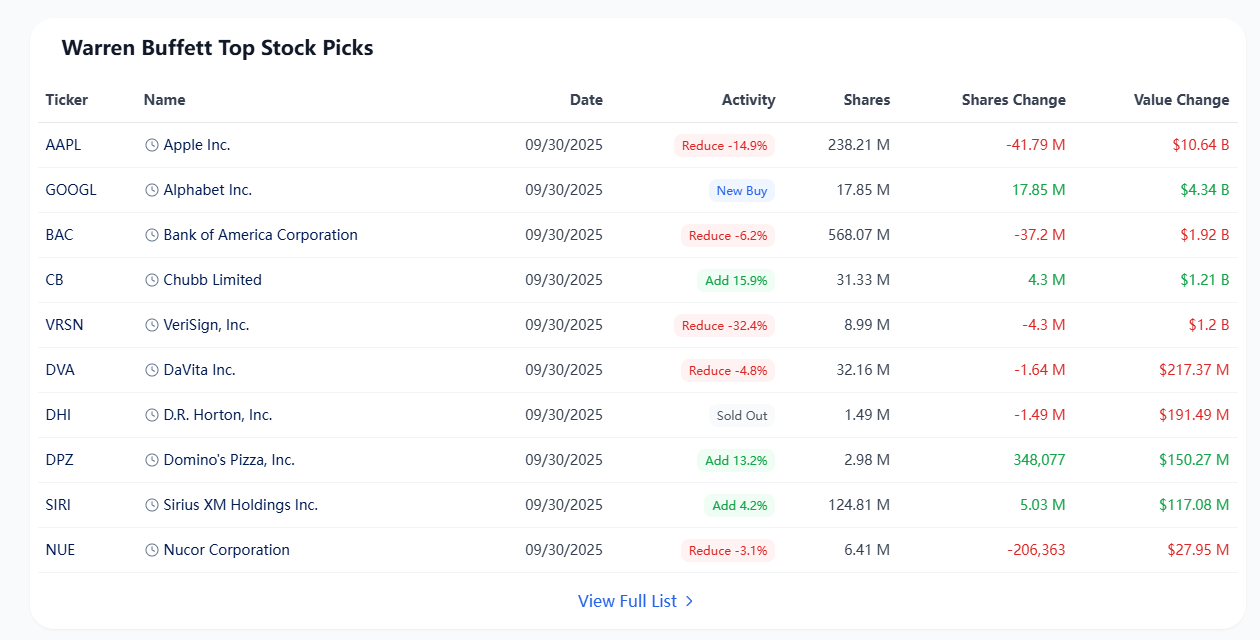

A granular look at the berkshire hathaway top holdings november 2025 before:2025-11-22 reveals a systematic unwinding of the concentration trades that defined the last cycle. The focus has shifted from aggressive equity beta to balance sheet optionality.

Unwinding the Concentration Discount

For years, analysts applied a "concentration discount" to Berkshire due to its outsized exposure to Apple (AAPL). The recent trimming—selling approximately 100 million shares—aligns with standard portfolio rebalancing mechanics. It reduces single-asset exposure while crystallizing gains for tax efficiency. This isn't necessarily a negative view on Apple’s fundamentals, but rather a mathematical necessity to maintain portfolio hygiene as the position grew disproportionately large.

The Financials Trade: Spread vs. Float

The most notable structural shift is the divergence between banking and insurance holdings. Berkshire has aggressively reduced its stake in Bank of America (BAC) while increasing exposure to Chubb (CB). From a macro perspective, this is a preference for "Float" (insurance premiums) over "Spread" (net interest margin). In a fluctuating rate environment, insurance underwriting income offers a non-correlated cash flow stream that is structurally different from traditional banking leverage.

The Hurdle Rate Implications

The implication of the cash pile is that the "hurdle rate" for new acquisitions has risen significantly. With short-term Treasuries offering competitive yields with zero volatility, the bar for equity entry is higher than it has been in a decade. Berkshire is essentially running a carry trade: earning interest on cash while waiting for valuation compression in the private or public markets.

Preparing for Transition

Finally, these moves must be viewed through the lens of succession. The portfolio is being simplified. By reducing complex banking relationships and concentrating on core industrial and insurance assets, the portfolio is being optimized for the incoming leadership. It represents a shift from a founder-led, high-conviction style to a more diversified, institutional-grade allocation strategy.

Sit quasi suscipit ea recusandae officiis est. Beatae maiores inventore omnis.

Quisquam quas porro non et. Nobis sit laudantium voluptate assumenda. Id sunt maiores eveniet rerum.

Laboriosam numquam ex doloribus pariatur optio incidunt. Est est amet quisquam velit. Eos laudantium consequatur atque reprehenderit placeat consequatur officiis. Cumque voluptates animi ex facere.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...