The $10 Billion All-In: Why Bill Ackman’s Portfolio Ignores the Rules of Diversification

The latest Q3 13F filing confirms what market watchers already know: the Bill Ackman Stock Portfolio is not an investment fund—it's a declaration of high-conviction risk. Pershing Square’s highly concentrated structure flies in the face of modern portfolio theory, demanding massive returns from a small basket of names.

The 80% Concentration Paradox

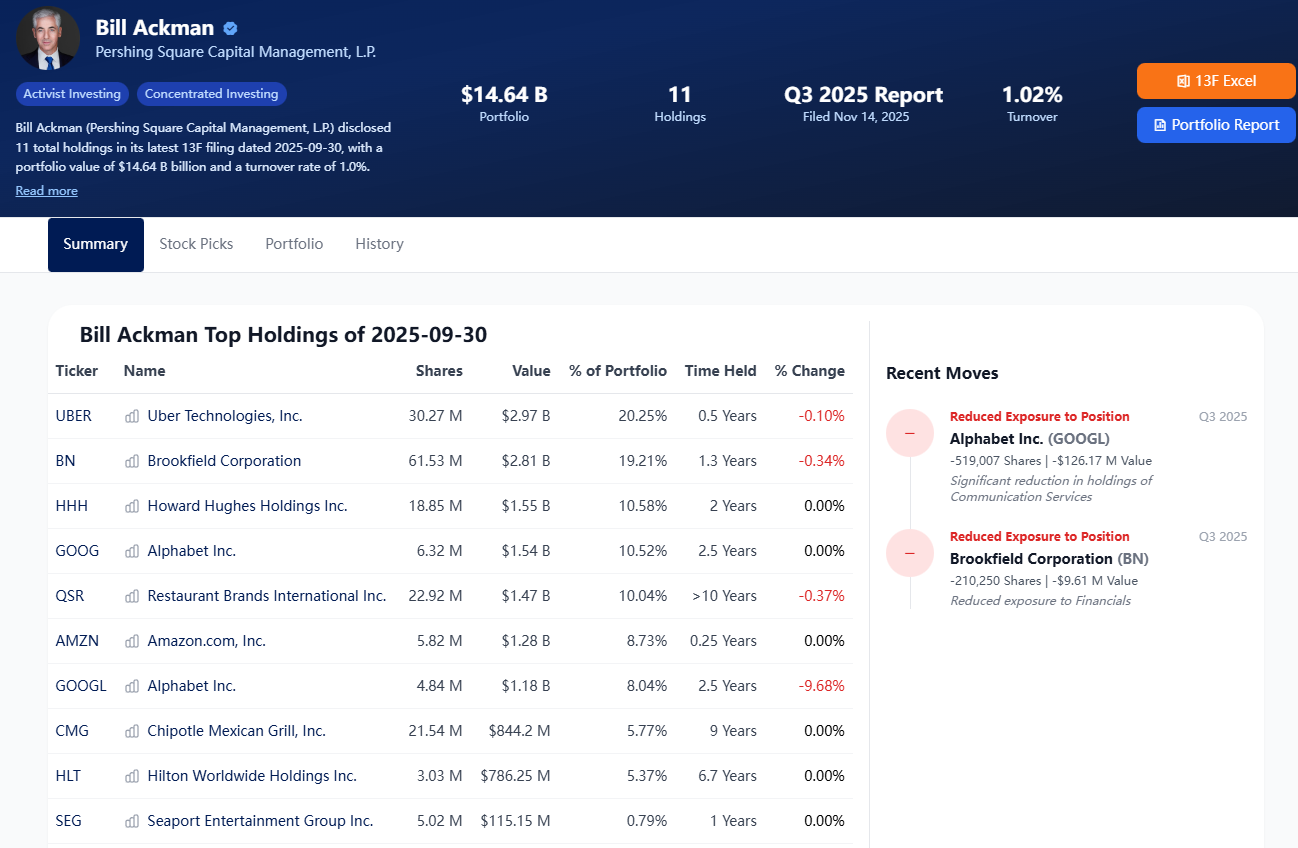

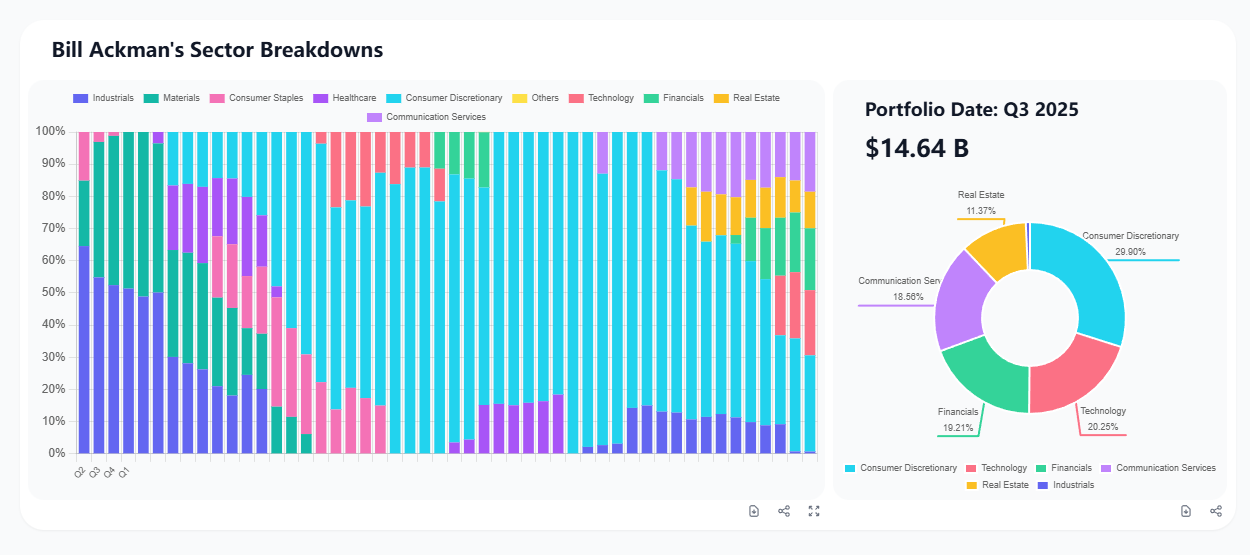

The core data point is staggering: Ackman’s top five holdings currently comprise over 80% of his total public equity value. This concentration proves that his success is tied entirely to the performance of a handful of companies like Chipotle ($CMG) and Restaurant Brands International ($QSR). Investors are paying for a focused, leveraged bet on these specific management teams, not market diversification.

Conviction Over Turnover

In sharp contrast to macro traders like Soros, Ackman’s portfolio turnover remains incredibly low. He buys only when he sees deep, undervalued potential and rarely sells, reflecting a true activist mindset. Q3 saw minimal trading activity within the core group, signaling continued confidence in his current management targets, even amid broader market volatility.

Is This Recklessness or Genius?

Ackman's strategy is undeniably binary. If his small group of high-conviction plays succeeds, the returns are explosive. If they fail, the downside is severe. Analyzing his portfolio provides a masterclass in high-stakes, highly focused activist investing, reminding investors that massive returns often come from rejecting conventional wisdom.

Bill Ackman’s portfolio strategy, as highlighted in the Q3 13F filing, is a bold departure from traditional diversification principles. Here's a breakdown of the key points:

1. Concentration Over Diversification

2. Activist Mindset

3. High-Risk, High-Reward Strategy

4. Rejecting Conventional Wisdom

5. Investor Implications

Ackman’s approach is a masterclass in conviction-driven investing, but it’s a double-edged sword. Success hinges on his ability to consistently identify and execute on undervalued opportunities, making it a high-stakes game that’s not for everyone.

Sources: Howard Hughes - Bill Ackman's Real Estate Empire

great post, what website is this?

Voluptatem nihil cum laudantium modi asperiores velit dolores. Molestiae aliquam sapiente aliquid placeat placeat ratione. Non asperiores enim iusto exercitationem voluptates.

Id sequi nihil quas in nemo non. Iusto veniam consequatur ut voluptas sed quidem libero. Cupiditate fugit unde et optio. Dolores sequi facere nobis praesentium. Itaque voluptas repellendus molestias molestiae voluptatem enim.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Omnis voluptatem non dolores sunt. Voluptatum magnam vel nihil necessitatibus. Et harum inventore et quia quibusdam perferendis quaerat. Corporis minima ipsa delectus facere reprehenderit eaque tempore.

Et et architecto ea ab. Nobis exercitationem quis qui non. Accusamus inventore facere perferendis aliquid. Dignissimos ipsam ipsa nihil quisquam. Tempore corrupti ut dolore. Veniam neque aliquid minus.