|

JPow Speaks

The day of days has come, apes. Yesterday at 2 pm, the Federal Reserve raised interest rates by 50bps, establishing a new target range of 4.25-4.5%. Base rates are now at their highest level since the pre-GFC days, and somehow, we’re still here.

That brings the YTD increase in the effective fed funds rate to 4,900% at a minimum. We won’t know the official EFFR until, well, today due to the fact that the metric is calculated based on overnight activity in short-term lending markets. So, stay tuned.

But for now, let’s take a look at what happened today. JPow said a lot, moved a lot, and dropped the mic around 3:30 pm, but that hour-and-a-half was a game changer.

For starters, Mr. Market had no clue what to do. Everyone was anticipating a 50bp hike, yet the news finally hit public wires, and markets sold off as if they had never heard of a central bank. Still, the selloff didn’t last long, and indices broadly finished only slightly lower.

But markets, of course, are reacting to far more than a simple move in the economy’s base rate. The words JPow and the FOMC used, along with their perceived tone, matter way too much as well. Like the SC Top 10, let’s check out some highlights:

- “I just don’t think anyone knows whether we’re going to have a recession or not. And if we do, whether it’s going to be a deep one or not ... it’s not knowable”

- “Even though we may be approaching the finish line, we aren’t there yet”

- “Historical experience cautions strongly against prematurely loosening policy. I wouldn’t see us considering rate cuts until the committee is confident that inflation is moving down to 2% in a sustained way”

- “There’s an expectation really that the services inflation will not move down so quickly so that we’ll have to stay at it. So we may have to raise rates higher to get to where we want to go and that’s really why we’re writing down those high rates and why we’re expecting that they will have to remain high for a time”

- “I think we’ll make the February decision based on the incoming data”

Apologies, I know some of those were long af, and reading is hard, but glad you made it through.

Anyway, a few things are clear, and from the FOMC statement, the SEP, and JPow’s comments, we can start to garner a few takeaways:

- Services inflation has taken center stage as the biggest problem in the room (it’s your fault; stop asking for a raise)

- JPow, like your parents due to their haircuts, is terrified of a repeat of the 70s. Hence, the boy will NOT be too quick to loosen policy. If anything, he’s begging us to get used to rates in the +4% neighborhood

- The longevity of elevated rates matters more than the speed at which they are raised

- 17 of 19 FOMC members indicated on their personal SEP that they see rates maxing out at least above 5%, suggesting more 25-50bp hikes are possible

- We might, just might, actually achieve a soft landing. But also, we might not…

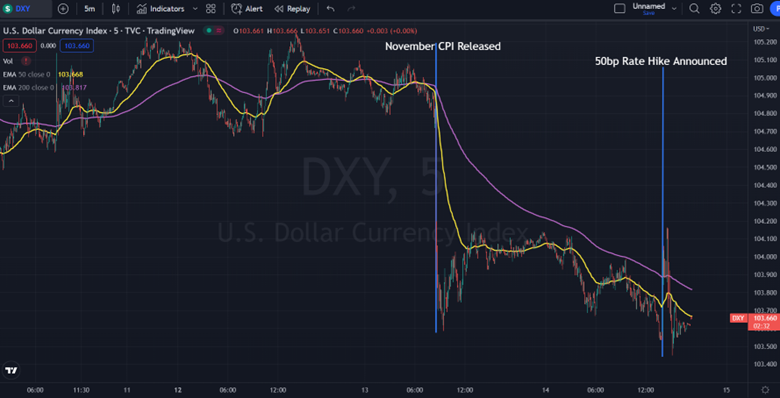

There was, however, a massive elephant in the room. JPow didn’t once mention yesterday’s cooler-than-expected inflation report, indicating the Fed could be basing its decision more on future expectations than past data. Pay attention to the dot plot.

Ever since Bernanke instituted forward guidance as a policy tool during the GFC, the most important rate move has always been the next one. After the hike, all eyes immediately turned towards February 1, 2023, which will be the next day of days for investors.

Finally, yields had a strong-arm reaction, gaining big on the day as investors sold off existing positions in hopes of snatching up higher-coupon issues now set to emerge in the coming days. Meanwhile, the dollar rallied sharply immediately post-announcement, only to end lower than the start of the day (currencies tend to rise with stricter monetary policy…so the 5-day chart below is just a bit…weird…).

|

Fuga animi mollitia ipsum tempora. Autem quo natus accusamus optio commodi. Alias tempore modi sit eos. Tempore possimus enim est nostrum hic.

Architecto quia debitis perspiciatis iste modi error quod. Velit eum molestias est aut tempora. Totam doloribus quam odio ipsa et.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...