The Death of Value is Exaggerated: Analyzing a Legacy Fund's Q4 Defensive Playbook

Every cycle, the industry prematurely declares traditional value investing dead. Yet, as the market wrestles with AI momentum fatigue and shifting interest rate expectations heading deeper into the year, the underlying flows suggest a quiet but massive rotation. Institutional capital is increasingly migrating away from top-heavy tech multiples and seeking refuge in established, cash-flowing equities. For analysts tracking these structural rotations, looking at legacy value funds provides a pure-play look at defensive portfolio construction and macro risk management.

The Institutional Rotation out of High Beta

The transition through the end of the year highlighted a textbook reallocation phase. While retail volumes remained heavily concentrated in semiconductor derivatives and zero-day options, institutional managers were actively locking in profits. When examining the regulatory disclosures of established Graham-Dodd practitioners, the strategy is clearly focused on capital preservation and yielding assets over speculative growth. You don't survive multiple decades of market cycles by chasing the top; you survive by strictly managing the drawdown and avoiding permanent capital impairment.

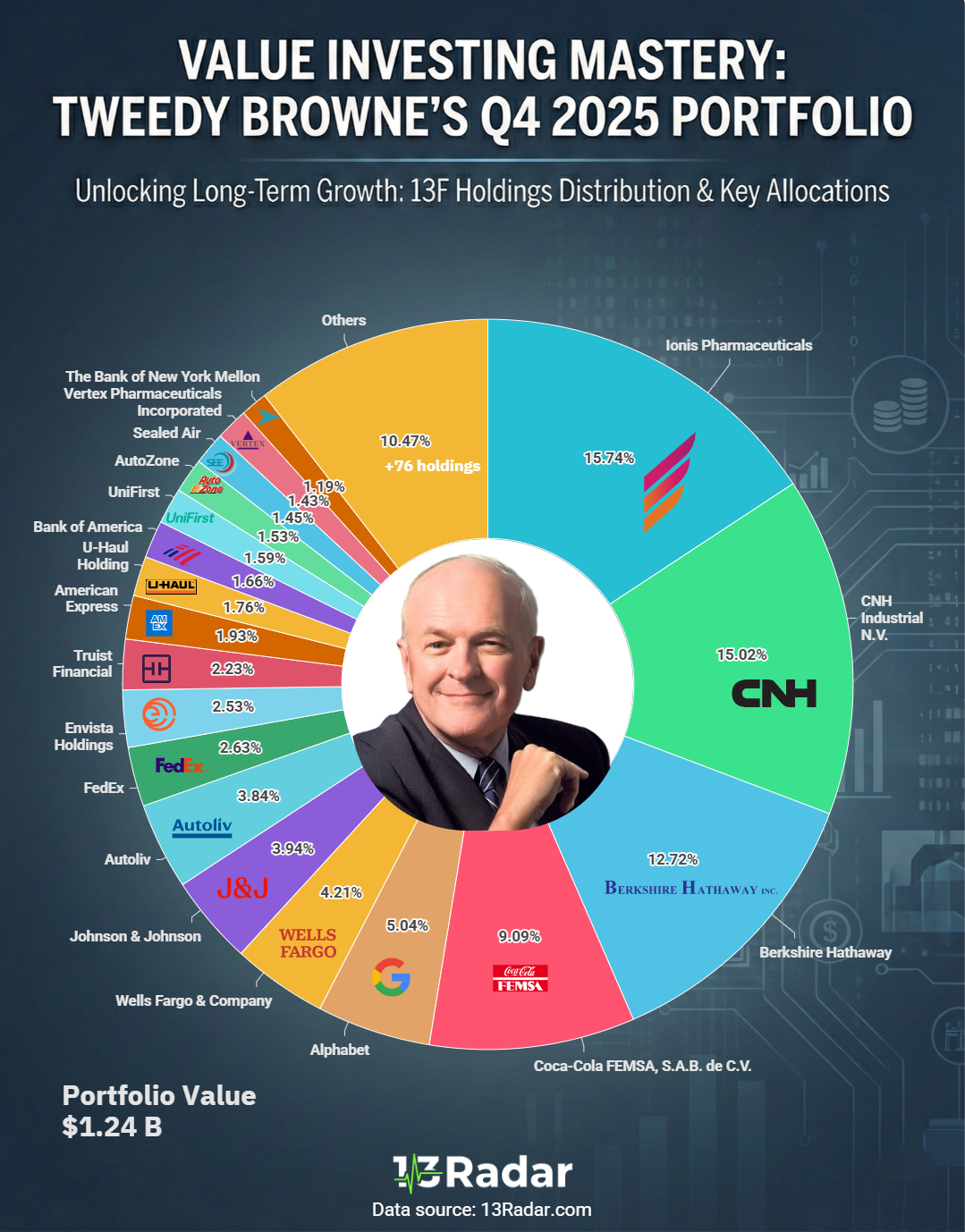

[Data Room] Sector Breakdown and Accumulation

A granular review of the SEC filings illustrates a heavy bias toward businesses with impenetrable pricing power and low debt-to-equity ratios.

For a concrete example of this defensive posturing, one can review the tweedy browne 13f q4 2024 holdings, which serves as a solid benchmark for strict intrinsic-value investing. The Q4 data indicates a sustained accumulation in legacy industrials, aerospace components, and regional financials. These managers are modeling for an environment where operating margins and supply chain dominance will outpace theoretical TAM (Total Addressable Market) expansions.

The Role of International ADRs in Hedging

Another structural takeaway from these filings is the heavy utilization of foreign equities. With the S&P 500 trading at historically stretched forward P/E multiples, legacy value managers are aggressively deploying capital into European consumer staples and international pharmaceuticals via ADRs. This provides a dual benefit: a natural currency hedge against a fluctuating dollar and exposure to regions where equity risk premiums remain highly attractive compared to domestic markets. It's a classic relative value play.

Low Turnover as Alpha Generation

In an industry obsessed with algorithmic trading and high-frequency turnover, the sheer lack of churn in these classic value portfolios is notable. The 13F data reinforces that these funds view their holdings as permanent business partnerships, not short-term trading vehicles. By maintaining multi-year holds on property & casualty insurers and consumer defensive stocks, they aggressively minimize tax drag and transactional friction. In a high-volatility environment, sitting on your hands and letting underlying free cash flow compound is often the most reliable way to generate alpha.

Vitae nobis atque tenetur deleniti consequatur laboriosam. Iusto delectus harum libero voluptas quod. Asperiores et expedita eum non. Sapiente quo aliquam veniam quod. Rem aut dolorem qui aut neque consequuntur. Iure tempore quos distinctio et.

Et nemo rem voluptatum inventore laborum quo. Explicabo est ex est consequatur laborum velit.

Vitae pariatur reprehenderit omnis eaque. Consequatur cupiditate id sed excepturi non. Aut qui et aut eaque.

Corrupti beatae error est ipsa debitis. Id nihil voluptatem ut cupiditate. Eos ut sed dolorum aperiam maiores aliquid. Ea voluptatem officia est non laborum dolores. Ut nihil quibusdam aut et qui tempora in. Sunt sit ut beatae mollitia quaerat.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...