|

Fighting with Yourself — Sometimes, especially in investing, your biggest enemy can be yourself. Even more especially if you work at JP Morgan. America’s largest bank is currently seeing the square of the century, a heated battle of JP Morgan vs JP Morgan. So what’s going on?

Everyone wants millionaire clients in the financial services industry. Fortunately for JPM adviser Gwenn Campbell, she is really good at getting exactly those. Unfortunately for Gwen, JP Morgan’s private bank is a little jealous and has started ruthlessly soliciting her client roster. Speaking of roster, did I mention that one of her clients is Alex Rodriguez? That’s right, A-Rod is not done being at the center of controversies yet.

Basically, Campbell was recruited by JPM in October 2020 and taken from Bank of America Merrill Lynch (BAML) where she built her book of business. Upon receiving confirmation that no other part of the firm at JPM would try to steal her clients, Campbell left BAML and brought a lot of dough over to JPM. Now, JPM’s private bank is trying to patch a cut of that dough. In response, Campbell has begun arbitration proceedings with the company.

Truthfully, fights like these happen all the time in finance. The stakes aren’t usually as high and the details are almost never this public, so grab some popcorn and enjoy the show while you can.

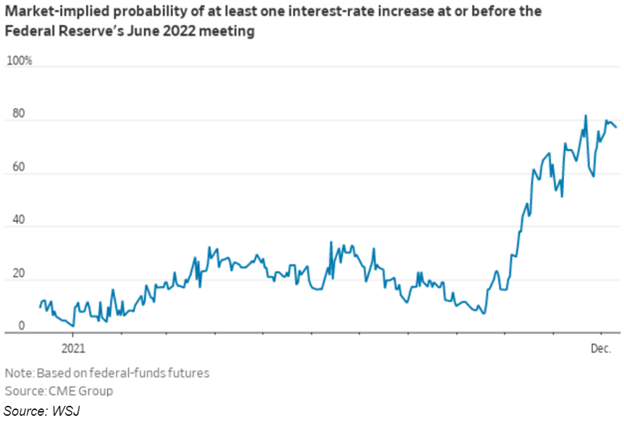

Hi, Hikes — Or maybe it’s high hikes? Who knows…at this point its really only JPow and the economic Gods. But obviously, the market is going to try its damndest to take a guess at future rate levels. As it stands right now, Mr. Market is dancing around 80% odds of at least one interest rate hike before the Fed’s meeting in June of next year.

If you’re putting two and two together and thinking “inflation, Powell retiring the word transitory, etc.”, trust your instincts. If not, allow me to elaborate.

The interest rate set by the Federal Reserve, known as the Fed Funds Rate, is a 25bp range of where the Central Bank believes the base rate should be. Influenced by the formulaic Taylor Rule, JPow and the gang do hold power to change rates on a discretionary basis. This base rate is the interest rate that banks lend to each other at for overnight deposits, and that all other rates in the economy - your car, your mortgage, your student loans, etc. - are set on top of. So, when the Fed believes the economy is overheating, as they appear to believe now, they will raise that base rate.

Why do this? Well, higher rates = more expensive, which disincentives spending and (ideally) slows things down to reign in inflation and get the economy back on course to “equilibrium.” In short, raise rates → slow down economy → lower inflation.

Given recent data on inflation, its no surprise whatsoever that the market is expecting hikes. What is unknown, however, is the timing of rate hikes along with the number and degree of those hikes. A one-time 50bp hike is a lot more rattling than two spaced out 25bp hikes. This may have sounded super boring to you, but trust me, hedge funds get built around this stuff. Run with it, or run from it!

|

Perspiciatis mollitia maiores et harum eum sit. Voluptates beatae rem harum dolor iste. Ipsam deserunt velit perspiciatis aut quasi. Dolor odit adipisci qui ipsam eos aliquam. Aliquid illum magni iure iusto et est rerum possimus. Omnis laudantium rerum eius. Est dolor pariatur hic quia.

Blanditiis rerum id earum explicabo velit. Non et voluptatibus omnis qui. Ut atque odio ea nisi fugiat aut nesciunt. Deserunt autem earum quia molestiae odit hic.

Sit aut est quam sit ipsa maiores sunt. Quis inventore et aperiam aperiam. Cupiditate deserunt expedita repellendus sint voluptatibus autem voluptatum. Molestiae soluta incidunt voluptate quasi doloribus sint nostrum magnam.

Soluta atque facere odit. Consectetur inventore maxime voluptates voluptas quasi quis. Sint qui sunt alias excepturi in qui. Est voluptatem ipsa architecto dignissimos et occaecati.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...