Bank Corporate Divisions

Banks provide many services, each of which is targeted to a certain clientele

What Are Bank Corporate Divisions?

Bank corporate divisions refer to specialized units within a bank, each focusing on specific functions such as retail banking, investment banking, risk management, or compliance.

These divisions ensure efficient operations, manage risks, comply with regulations, and provide diverse financial services to customers, contributing to the overall functioning and profitability of the bank.

Banks are the center of economies. A nation can thrive or perish by the way it operates its banks. Banks provide many services, each of which is targeted to a certain clientele, including:

- Keeping our money secure

- Insurance

- Investment

- Loan issuance

- Many more

The lines between the different banking divisions can blur in our digital world as we have everything in our online banking application. Nevertheless, it is important to distinguish between the various banking segments to build a career in finance.

An investment banker's tasks can be very different from a retail banker's; the former will be dealing with a small number of clients, who are usually very specialized in sizable transactions, while the latter will have small transactions in large volumes.

There are other parts of banking that most of us have never dealt with because their services are focused on a niche client base, like private banking for high net-worth individuals or corporate banking for businesses.

While this article will focus on a bank's operating segments, you should also know that most big banks have quality management departments like human resources, internal audits, legal departments, etc.

- Banks have many divisions, each specializing in offering specific services to their clientele.

- Retail banks are the division the average individual uses daily for services like credit card issuance.

- Commercial banks offer similar services to retail banks, except they focus on businesses instead.

- Global banking is the division that facilitates cross-border transactions.

- Private banks exclusively serve high-net-worth individuals.

- Investment banks are the middlemen of high-level transactions between businesses

Retail banking

Retail Banking is the division we interact with on a day-to-day basis when we need checking or savings accounts, credit card issuance, mortgage loans, lines of credit, etc.

Retail banks usually compete with other banks in customer service and advertisements. However, since most retail banks provide similar services with very small differences between their products, customer service is the driving factor of success.

Somebody working for this segment should expect repetitiveness in what they provide. Additionally, one's interactions would not be personalized because of the big client base.

While most retail banks provide the same services as previously mentioned, big banks have an advantage because they are perceived as "too big to fail." This leads many to believe their money is more secure there.

However, regional banks can be more interpersonal and flexible with their services because it is easier to access the upper management.

The retail section of a bank is monetized in different ways. The most common ways are through:

- Interest on loans

- Fees for services

- Points programs (mainly used in credit cards)

An important thing for aspiring retail bankers to know is that this segment is quickly being automated and digitized as customers are more likely to use online banking and ATMs. In some banks, even the customer service lines are automated by a virtual assistant.

Commercial Banking

Commercial banks offer services like the ones provided by retail banks, only more tailored toward enterprises. The clients can range from big companies like Apple to small companies like the local bakery.

The services provided by the commercial banking division include:

- Business accounts

- Credit cards

- Loans

- Payments

- Advisory services

These services are monetized by interest on loans and fees.

The number of clients in commercial banking is smaller than in retail, making it more focused on relationship building with existing customers and marketing to businesses and business owners.

Businesses usually need their employees to have access to the business account, but they also need to control that access for each employee.

Also, the bank's statements need to be sent to certain people. Therefore, many people will be involved in the account, and the bank will have to control that access per the business's needs.

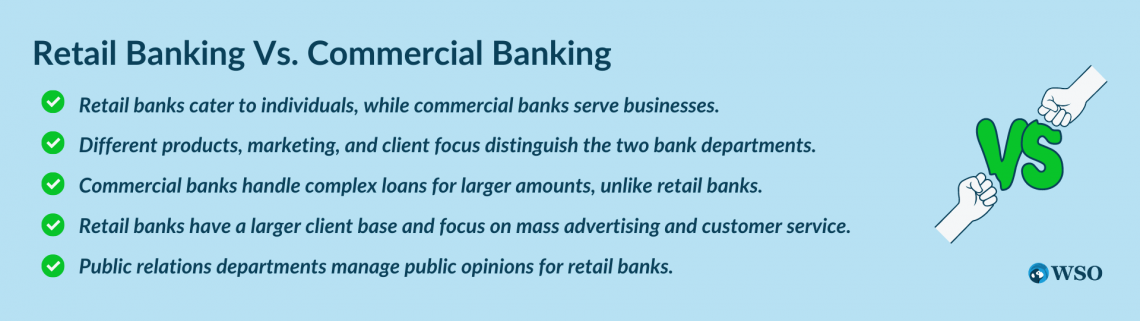

Retail Banking Vs. Commercial Banking

Like any other business, banks need to adapt their products to satisfy their customer's needs, and an individual's needs can be very different from that of a business. Big banks are solving this issue by creating separate departments (retail and commercial), each specializing in one type of clientele.

On the other hand, small banks do not have the means to operate several departments, resulting in either having a bank specialized in retail or commercial services.

Despite retail and commercial banks providing similar services, retail banks target the individual while commercial banks target businesses. As a result, the products, marketing strategies, and employee qualifications are different between the two bank departments.

The loan issuance process is more extensive in commercial banks than for individuals because of the many variables attached to a business, and the loans issued are usually much larger than the ones issued in retail banks.

The number of clients in retail banks is much larger than in commercial banks, making them more focused on mass advertising and customer service initiatives.

Retail banks are also exposed to the public more than their commercial counterparts, so they usually have a public relations department to manage the public's opinions.

Global Banking

Global banking is an essential part of the global economy as it is the middleman that connects the world economies. In addition, this segment of a bank helps people with cross-border transactions.

Clients of this division can be companies operating in different regions, investors looking to invest abroad, or individual travelers who need to spend their money abroad.

One of the most significant global banking divisions is HSBC international banking. This division of the bank provides services to ease cross-border transactions. Some of these services include:

- Transborder advisory management

- Foreign currency accounts (like US Dollar accounts in Canada)

- Foreign currency credit cards

- Global liquidity and cash management

The services provided by global banking include overseas investing, transfer of assets abroad, liquidating global assets, advisory services, and research. In addition, those banks usually have branches worldwide with employees who are knowledgeable in the markets and regulations of the economies.

Advertising for global banks usually happens by pitching to potential clients. Therefore, you will commonly find advertisements for these banks in airports since they have a concentration of clients, as seen in the picture below with the HSBC ads.

Private banking

This bank division mainly services high-net-worth individuals (HNWI) or families with their investments, insurance, and loan issuance.

Because of their small number of clients, private banks are focused on relationship-building with their clients, and their services are tailored for each client individually.

Working in private banking is the most interpersonal among all the other banking divisions. The idea behind private banking is to have all wealth management services in one place. High net-worth individuals can find services like:

- Portfolio management

- Insurance

- Estate planning

- Trusts

- Tax services

Wealth management or private banks sometimes have a benchmark of investable assets a client must have to be accepted into these banks.

While some private banks will accept individuals with $50,000, that benchmark can go up to $1 million to be accepted as a client in these banks.

One advantage that Private banks enjoy is the stickiness of their customers, as many families tend to use a bank’s services for generations as a means to transfer wealth and financial knowledge.

One of the interesting private banks is Union Bank Privee, one of the biggest specialized wealth management firms in Switzerland. It exclusively deals with HNWI and has many connections with some of the most exclusive funds, including the infamous Bernie Madoff fund.

The Advantages of Private Banking

The advantages of private banking include better pricing and a more personalized product offering. In addition, it is useful for HNWIs to use those banks as a means to transfer wealth to their offspring.

Privacy is also an advantage of private banking as it is in banks’ best interest to keep customer dealings private to deflect competitors from offering similar products and poaching their clients.

Access to alternative investments is yet another advantage for wealth management firms. For example, some hedge funds and private equity firms only accept assets from individuals with a high net worth, and private banking is one way to get into these funds.

For business owners, juggling their business finances can be very difficult. Private banks are a convenient way to delegate the management of their finances to the bank while focusing on building their business.

What further helps, business owners get one point of contact with private banks that are very knowledgeable about their financial situation.

While private banks have many advantages, they also have disadvantages, like:

- A possible conflict of interest for employees

- A high employee turnover

- High management fees

- Heavy regulations that limit their offerings

Investment banking

Investment banks are institutions that help manage and execute big and complex transactions.

These include:

- Mergers and Acquisitions (M&A)

- Initial Public Offering (IPO)

- Underwriting debt offerings (e.g., bonds)

- Restructuring

- Broker trades between institutions and/or individual

Although they offer many services, an investment bank’s main focus is to raise capital. They operate as middlemen between companies, investors, and creditors. These banks also raise capital for government entities and non-profit organizations.

This banking division is considered the most prestigious because of its high salaries and high-level clientele. That fact leads investment banks to have a very competitive nature between one another and their employees.

Clients commonly go to investment banks to seek advice on structuring a deal. The recommendations are made by financial field experts and tailored to the current financial environment.

The most popular investment banks are usually subsidiaries of a bigger banking group. For instance, some of the biggest investment banks are Goldman Sachs, JPMorgan Chase, Bank of America Securities, and Morgan Stanley.

Working in investment banks is known to be very intense. Some interns work up to 100 hours a week. However, the workload becomes more manageable as you rise through the ranks as Managing Directors work 50-60 hours weekly.

While the work is very demanding, it is also known that investment bankers get paid handsomely for their efforts.

Researched and authored by Mohammed Al-Maskari | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?