Levered Free Cash Flow (LFCF)

Used to value equity in financial modeling

Levered free cash flow is the amount of cash that a company has remaining after accounting for payments to settle financial obligations (short and long term), including principal repayments. It is also referred to as levered cash flow and abbreviated as LFCF.

Investors perceive businesses with positive LFCF as financially healthy.

LFCF is important as it is the amount that can be used to pay back equity investors (through dividends or share buybacks) and reinvest into the business and grow. Thus, a positive LFCF illustrates a company’s ability to cover all financial obligations, distribute dividends, and grow.

On the other hand, unlevered free cash flow (UFCF) is the sum available before debt payments are made.

The difference between UFCF and LFCF is the financial obligations (interest and principal). LFCF is usually given more importance by equity investors as they consider it a better indicator of a company’s profitability.

The two figures together tell us whether a company is functioning with a reasonably healthy amount of debt on its books.

In addition, by gauging the current level of debt, users can ascertain a company’s ability to raise additional funds through external financing.

- Levered Free Cash Flow (LFCF) represents the cash available after settling all financial obligations and is vital for assessing a company's financial health.

- Positive LFCF indicates a company's ability to pay dividends, reinvest, and grow, making it attractive to investors.

- Negative LFCF may not be alarming if it results from strategic investments for future growth, but companies should ensure they can sustain operations until LFCF turns positive.

- LFCF is preferred by equity investors as it considers debt payments, providing a more accurate picture of a company's profitability compared to Unlevered Free Cash Flow (UFCF).

- Managing LFCF involves controlling expenses, increasing revenue, optimizing working capital, and making strategic decisions on debt levels to influence a company's growth prospects positively.

Formula and Calculation of Levered Free Cash Flow (LFCF)

There is more than one way of calculating LFCF. Users can arrive at LFCF from EBITDA, net income, or UFCF.

- Calculating LFCF from EBITDA

LFCF = EBITDA - Taxes paid - Capex - Changes in Working Capital - Mandatory Debt Payments

The EBITDA is reduced by taxes, capital structure (CapEx), changes in working capital, and mandatory debt payments. These debt payments include interest expenses and principal repayments.

- Calculating LFCF from net income

LFCF = Net income + Depreciation and Amortization - Capex - Changes in Working Capital - Mandatory Debt Payments

What can Levered Free Cash Flow (LFCF) Tell us?

The benefits of using levered free cash flow (LFCF) go beyond its predictive power in the short term.

Here are a few things that it tells us about a company.

1. Ability to expand and pay returns

Levered cash flow indicates how much money a company can put towards reinvesting into new opportunities or delivering returns to its shareholders.

2. Ability to raise funds through debt

The higher the LFCF, the higher the capacity to raise additional funds through debt due to a better ability to pay it back. Therefore, the difference between UFCF and LFCF can tell users whether a company has a healthy amount of debt.

If there is excessive existing debt on a company’s balance sheet there won't be enough LFCF to pay back additional debt, which can make it difficult to raise more capital through debt.

In addition, it could be that equity investors also perceive the company to be risky, making it tough to raise funds through equity.

3. Negative LFCF

A company can have a negative LFCF. However, it does not always spell doom. It is a possibility that the company has made significant capital investments to grow further that are yet to pay off.

It is acceptable to have negative LFCF temporarily if the it can be turned positive in the future. The company needs to ensure that it can secure cash to operate until it generates positive LFCF.

4. Choice of utilization

A company may choose to pay returns to its shareholders through dividends or share buybacks if it believes that:

- There are no new opportunities to expand.

- The opportunities are not so attractive, meaning that the opportunity costs to shareholders are higher than the expected returns.

The shareholders can then generate better returns if they invest their capital elsewhere.

Alternatively, if there are good opportunities on the horizon, a company would ideally choose not to distribute money to its shareholders. Instead, the cash would be retained to meet the capital requirements for the new projects.

Therefore, how a company manages its LFCF says a lot about its growth prospects.

Levered Free Cash Flow (LFCF) vs. Unlevered Free Cash Flow (UFCF)

Levered free cash flow (LFCF) is the amount of money a company has after deducting the amounts payable towards all its financial obligations. Interest expense, as well as principal payments, are considered financial obligations. However, prepayments are not considered because a company is not obligated to pre-pay its debt.

A positive LFCF illustrates a company’s ability to cover all financial obligations, distribute dividends, and grow. Use of debt is called leverage, so cash flow is said to be levered when adjusted for debt payment obligations and unlevered when not.

Unlevered free cash flow (UFCF) is the cash flow available to owners of all sources of capital (equity-holders, mezzanine financing owners, and debtholders). It represents the cash available to grow a company’s revenue-generating capacity using all sources of funds.

The difference between UFCF and LFCF is what financial costs they account for. While LFCF is the cash available to pay to shareholders, UFCF is the cash available to pay shareholders and debtholders of a company.

LFCF tends to attract more attention from equity holders as it accounts for all financing obligations. As a result, it presents a more accurate picture of a company.

On the other hand, UFCF paints a rosier picture as it shows higher cash available even when the financing obligations are enormous. Thus, equity investors use LFCF as a better indicator of a company’s profitability.

The video below, taken from the DCF Fundamentals section of our DCF Modeling Course, walks you through the differences between UFCF and LFCF.

Negative levered free cash flow (LFCF)

Negative levered free cash flow occurs when a company does not have enough cash to pay its debt obligations and must borrow from other entities to stay in business. However, it is not always a bad scenario.

One possibility is that significant recent investments were made that are yet to pay off. In that case, negative LFCF levels may be temporary. Negative LFCF is acceptable as long as the negative numbers can be turned positive in the future.

Then all a company has to do is secure enough cash to operate until it starts generating positive LFCF. Very often, this is easier said than done.

Levered free cash flow is a vital metric for companies to monitor. It gives them information on how much money they can use freely. It also allows them to observe their debt obligations when compared with UFCF.

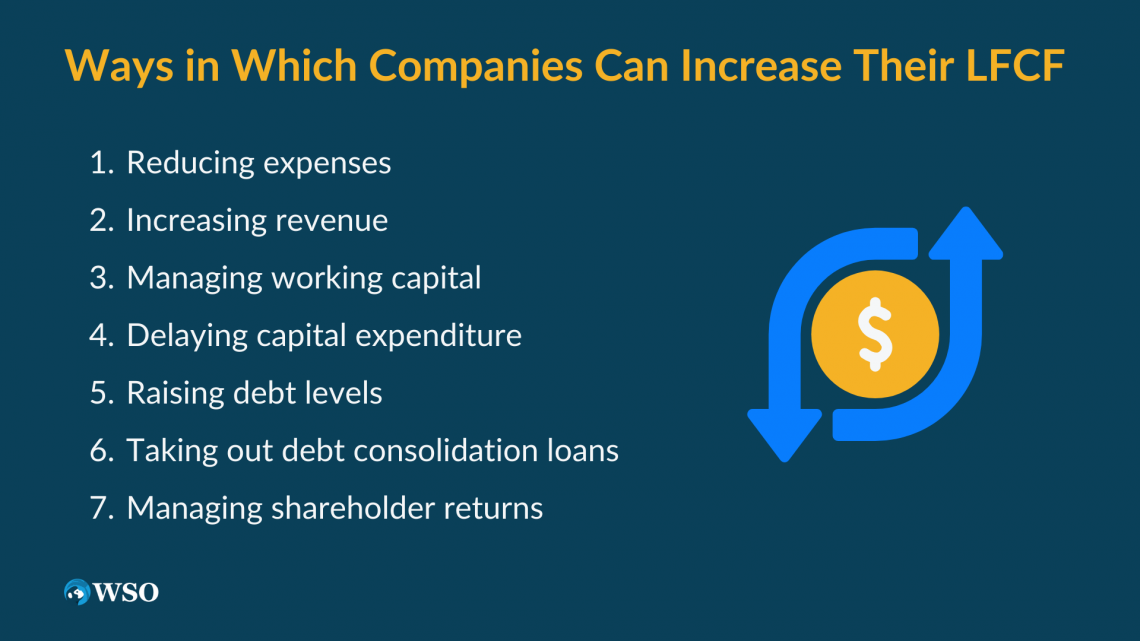

Below, we explore different ways in which companies can increase their LFCF.

1. Reduce expenses

When businesses lower costs, they have more money left over to invest in other aspects of the company, which means that they can grow faster, increase their profits, or reduce their losses.

2. Increase revenue

An increase in revenue results in an increase in EBITDA, which boosts LFCF. However, the increase in revenue should be accompanied by an increase in cash flow from operating activities rather than an increase in accounts receivables.

When calculating LFCF, an increase in accounts receivables would offset any increases in EBITDA by increasing the working capital requirements.

3. Managing working capital

Reducing working capital needs also helps increase LFCF. For example, companies may reduce working capital requirements by negotiating favorable credit terms with creditors and debtors, optimizing the workforce, and managing inventory effectively.

4. Capital expenditure

Like changes in working capital, UFCF is reduced by the amount put aside for CapEx. By delaying capital investments, companies may improve UFCF and LFCF in the short term.

5. Raise debt levels

It might seem counterintuitive at first glance to raise debt as a way to increase LFCF because debt obligations are deducted to arrive at it. However, while repaying debt might be a fix in the short run, it will reduce its capital and earning capacity.

On the other hand, raising debt should increase the company’s earning capacity. Therefore, it is helpful for companies operating with healthy debt levels to raise more debt at reasonable financing costs.

6. Debt consolidation loans

If a company needs more money but doesn’t want to borrow too much, they can take out a debt consolidation loan at favorable rates, which will allow them to access funds without having too much debt on the books.

7. Managing shareholder returns

Companies with low levels of LFCF or with negative LFCF should hold back on paying dividends and share buybacks. Instead, this money should be reinvested into the business to increase its earning capacity.

Some of these solutions may prove to be temporary fixes, while others might improve LFCF in the long run. It is up to the investors to analyze how a company’s management manages cash.

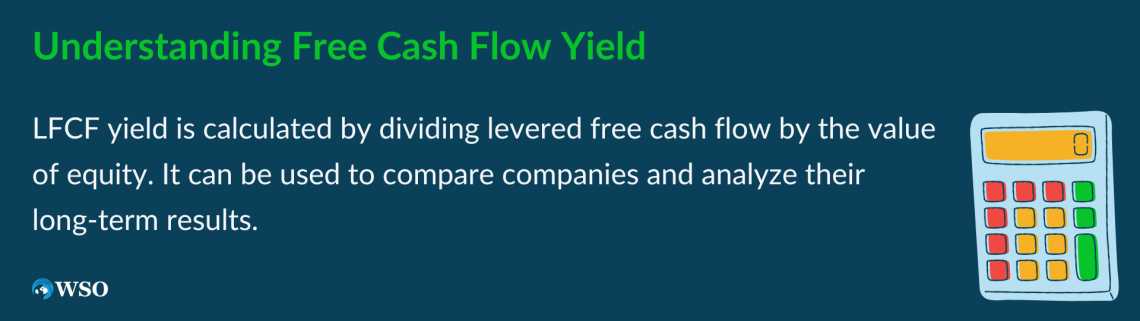

Levered free cash flow yield

Free cash flow yield measures a company’s cash generation ability. It compares the amount of cash a company generates from its operations with the funds employed to generate it (value of equity for LFCF and enterprise value for UFCF).

A higher LFCF yield means that the company generates more cash from the equity funds it employs.

LFCF yield is calculated as levered free cash flow divided by the value of equity. Free cash flow yield is meant to show investors how much free cash flow a company generates relative to the value of its sources of funds. LFCF yield measures LFCF against the value of equity, while UFCF yield measures UFCF against enterprise value.

LFCF yield = LFCF / Value of equity

LFCF yield can be calculated for any period but is mainly used when calculating the company’s long-term results.

In addition, because it standardizes the cash flow relative to a company’s valuation, it can be used to compare one company to another or to analyze how well one business is doing relative to its peers.

For example, let’s assume Company A has $10 million levered cash flow and its market capitalization (value of equity) is $200 million. Calculating the ratio reveals that its levered cash flow is 5% of the total market cap.

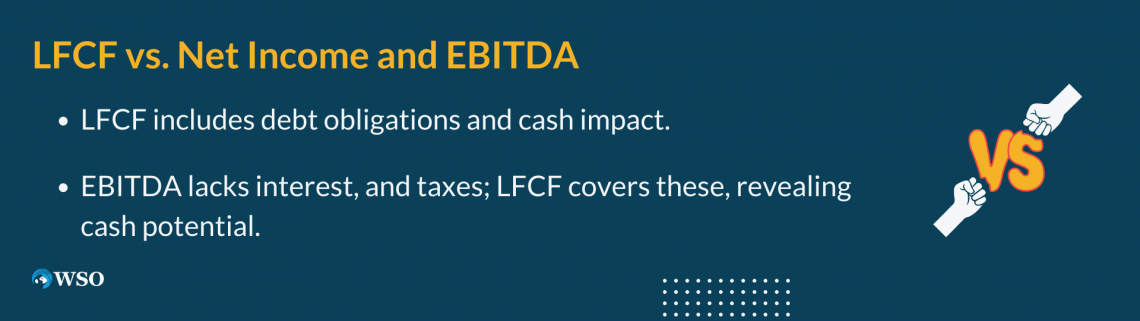

Levered free cash flow (LFCF) vs. net income and EBITDA

LFCF differs from net earnings, which are used to calculate popular metrics and ratios like earnings per share (EPS), price-to-earnings (P/E), and price-to-book.

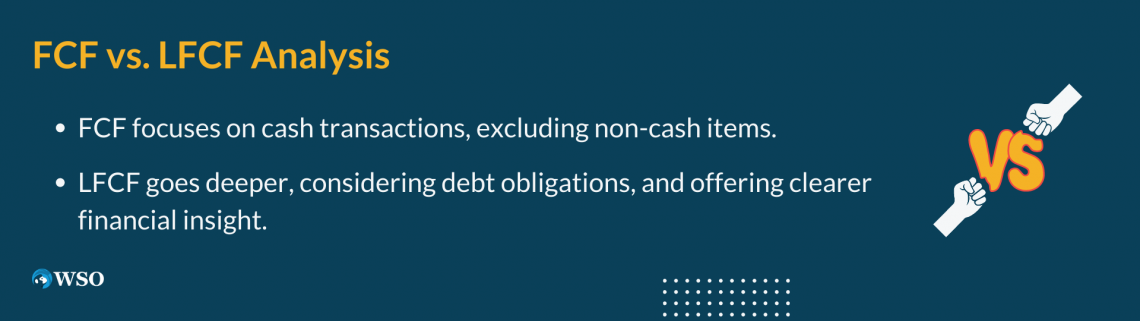

FCF ignores the impact of non-cash items like depreciation and amortization, so they are added back when computing FCF from net earnings.

In addition, FCF considers the changes in working capital requirements and capital expenditure, while LFCF goes further and considers all debt obligations that need to be settled.

Free cash flow gives a more straightforward overview of a company’s profitability because it focuses only on cash transactions.

FCF can also disclose when a company manipulates its earnings using non-cash measures. An example of such measures is making a large purchase (like buying a new property or investing in new intangible assets) to increase depreciation expense.

LFCF differs from earnings before interest, tax, depreciation, and amortization (EBITDA) because the latter does not account for interest payments on debt, depreciation, amortization, and taxes.

In contrast, LFCF accounts for interest payments and taxes, as well as for principal debt repayments.

Like net earnings, EBITDA also ignores capital expenditure and changes in working capital. Although EBITDA is not based on the cash system of accounting, it tells us more about a company’s potential to generate cash than net earnings by ignoring non-cash expenses like depreciation and amortization.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?