Amortization Vs. Depreciation

Understand the key differences between these accounting methods for allocating asset costs over time. Learn how amortization applies to intangible assets and depreciation to tangible assets, and why each is essential for accurate financial reporting.

Amortization Vs. Depreciation

Amortization and Depreciation are accounting concepts where the costs of assets are spread throughout multiple years for the decrease in value due to wear and tear and usage. This spreading of costs throughout the life of the asset is to represent the consumption and decrease in the value of the asset over time.

Both methods are presented differently in the financial reports as there are different methods to calculate.

Depreciation refers to systematically allocating the cost of tangible fixed assets—such as machinery, vehicles, and buildings—over their useful lives. On the other hand, amortization applies to intangible assets, which lack physical substance but still hold value for a business. Examples include patents, copyrights, trademarks, and software licenses.

Depreciation is the process of accounting for the physical wear and tear that assets experience as they are used in business operations. The Depreciation is recorded on the income statement as an expenses, and reducing the asset's carrying value on the balance sheet.

Like depreciation, in amortization the cost of an asset is spread out over the useful life. However, amortization is calculated using the straight-line method, where the same amount is expensed across the period.

- Amortization and Depreciation refer to methods of spreading out the cost of assets over time, with amortization applying to intangible assets and Depreciation to tangible assets.

- These methods provide a realistic view of asset values on financial statements, helping companies better manage cash flow, budget planning, and tax liabilities.

- Companies use amortization and depreciation to allocate asset costs gradually, preventing large one-time expenses and aligning costs with revenue generation over an asset’s useful life.

- Amortization typically uses a straight-line method, while Depreciation offers multiple methods, such as straight-line, declining balance, or production units, to fit different asset types and usage.

What is Amortization?

Amortization is a systematic process where an intangible asset is reduced in value over its useful life. Intangible assets are nonphysical assets that provide value to a business but lack tangible structure. Some examples of intangible assets include patents, goodwill, trademarks, and copyrights.

Amortization involves systematically reducing the value of an intangible asset on the balance sheet and recognizing an expense on the income statement. This practice spreads out the asset's cost over its expected life, avoiding a large expense in a single period and matching the expense with the revenue the asset helps generate.

Typically, straight-line amortization is used, where an equal expense amount is recognized each year over the asset’s useful life. For instance, if a company spends $100,000 on a patent with a 10-year life, it will record an annual amortization expense of $10,000.

What is Depreciation?

Depreciation is an accounting method that is utilized to allocate the cost of a physical asset over its useful life. Physical or tangible assets include buildings, machinery, computers, and vehicles that lose value over time due to wear and tear or even obsolescence.

Unlike amortization, which applies to intangible assets, depreciation spreads out the cost of physical assets. The value of these assets decreases as they age, which is reflected in financial records to give a more accurate picture of a company’s true value over time.

Several methods are used in depreciation accounting:

- Straight-Line Depreciation: Similar to straight-line amortization, this method allocates an equal yearly expense.

- Declining Balance Method: This accelerated method expenses more in the asset's earlier years.

- Units of Production: Calculates Depreciation based on an asset’s usage or output.

Amortization Vs. Depreciation: Key Differences

We have learned the definitions, meanings, and applications of the concepts above. Below is a table that highlights key differences between them.

| Aspect | Amortization | Depreciation |

|---|---|---|

| Asset Type | Intangible assets (e.g., patents, trademarks, goodwill) | Tangible assets (e.g., buildings, machinery, vehicles) |

| Purpose | Reflects the decreasing value of non-physical assets | Reflects the decreasing value of physical assets |

| Tax Deductibility | Often subject to specific rules depending on asset type and location | Generally tax-deductible and often more flexible |

| Expense Classification | Shown as an operating expense on the income statement | Shown as a non-operating expense on the income statement |

| Impact on Financial Statements | Reduces the value of intangible assets on the balance sheet | Reduces the value of tangible assets on the balance sheet |

| Useful Life | Based on the legal or expected life of the intangible asset | Based on physical lifespan, wear, and obsolescence of the asset |

Amortization vs. Depreciation: Real-World Example

To highlight the impact, let’s explore a couple of scenarios.

Example of Amortization in Microsoft

We can take the example of Microsoft (MSFT) where we can find amortization at different stages in the 10-K document.

Amortization first appears in Part II, Item 7, where the report explains the R&D costs are included in the cost of revenue of the estimated life of the product.

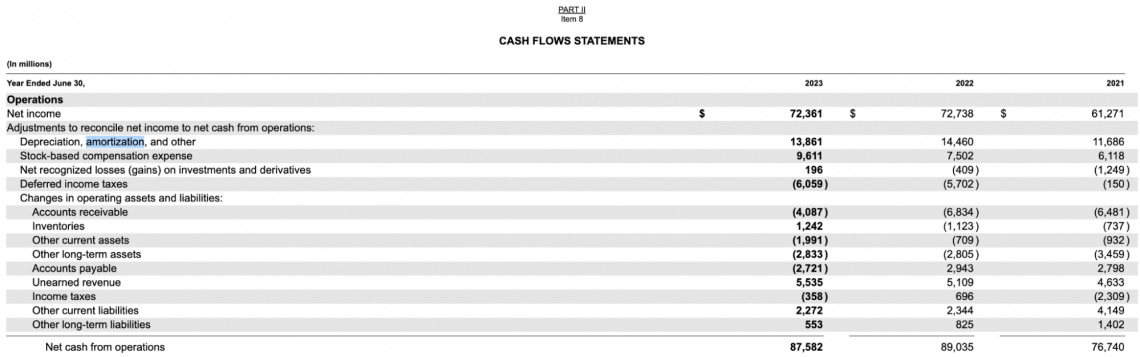

Then later it appears with depreciation on the Cash Flows Statements under Part II, Item 8.

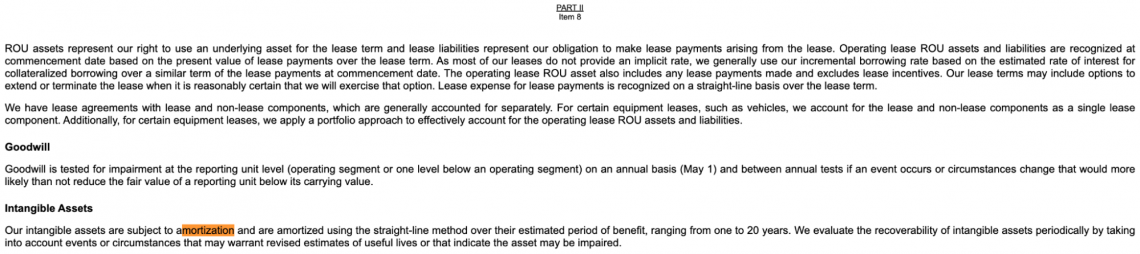

Once again, in Part II, Item 8 amortization appears in the Note 1 of accounting policies, under Intangible Assets, where it explains that these assets are amortized using the Straight-Line method over estimated period of benefit.

In Note 10, pertaining to Intangible Assets, the company filing exhibits a Schedule where the intangible assets related to technology, customer, marketing, and contract-based are amortized. And, the total amount of amortization has reached $2.5bn in the year 2023.

Example of Depreciation in Microsoft

Depreciation first appears on the Balance Sheet in Part II, Item 8.

Then, it appears under the same section where the document highlights how plant-property-and-equipment (PPE) is depreciated.

Then there is a separate section in Part II, Item 8, where it shows different tangible/fixed assets and their accumulated depreciation.

There are other places where amortization and depreciation are mentioned, but, for the sake of brevity, we have mentioned only the places where they are relevant to the article.

Conclusion

While amortization and depreciation serve similar functions, they are applied to different asset types that are classified based on their tangibility. They are calculated using different methods and techniques to reflect an asset's life precisely on financial statements.

Understanding these concepts is integral in accounting and finance, as they aid in record-keeping, financial reporting, cash flow analysis, and income tax implications.

By grasping these differences and the explanation behind approaches, financial professionals can make informed decision-making on asset valuation and better support their financial health.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?