Calendarization

A process that encompasses the consolidation, organizing, and adjustments in financial records along with operational performance to make it in line with the standard calendar year-end date.

What Is Calendarization?

Calendarization is a process that encompasses the consolidation, organizing, and adjustments in financial records along with operational performance to make it in line with the standard calendar year-end date, 31st December.

Incomparable companies' financial statements are compared over the same period. However, some companies have different financial year-end dates, so this comparison will be unfair to some companies.

Hence, calendarization spreads the recognition of a company's expenses over more than one period. This is done over a fixed period.

A financial examination is usually used in the creation of a budget. Income and expenses are distributed during all the periods used within a budget. In real life, these allocations will vary from the actual income and expenses, but expectations are that they will match the budget.

The difference between a fiscal and a calendar year helps one understand calendarization better. Unlike some companies, some base their fiscal year on the normal calendar year in the respective country.

A fiscal year is a period when the company readies its financial statements. Every firm prepares three main financial statements for its budgetary or calendar year: the balance sheet, the cash flow statement, and the profit and loss account.

Companies usually follow the common fiscal years (Jan to Dec, April to March, July to June, Oct to Sep). However, companies are free to choose their fiscal year in many places.

For example, most firms have an FY from Jan to Dec in the United States. The US Federal government is open from Oct to Sep, while the state governments can follow different FYs. India has an FY from April to March; hence, almost all companies there have the same calendar.

- Calendarization is the process of aligning financial records and operational performance with the standard calendar year-end date, which is December 31st.

- The main aim of calendarization is to ensure consistency and comparability in financial reporting by standardizing the fiscal year-end.

- Calendarization facilitates easier comparison of financial performance across different periods and entities, aids in regulatory compliance, and improves transparency for stakeholders.

- Calendarization helps companies meet regulatory requirements that mandate financial reporting aligned with the calendar year, ensuring timely and accurate submissions.

The Need For Calendarization

Comparing two companies' financial data reports during the same period is important. This ensures consistency for the data. However, comparing company reports for different periods may produce meaningless interpretations.

Many companies have their financial years starting and ending on different dates. For instance, some might have a financial year that starts in March or April. Comparing them will be improper, inadequate, and misleading.

Calendarization is the standard period report process for companies' financial statements, and this method is helpful in horizontal analysis.

In other words, calendarization is the accounting process of systematizing the full financial statements of different companies. This procedure aims to facilitate comparisons of these companies' financial statements.

Thus, it is right that it is the operation of the following companies' financial statements for the same period.

Calendarization Calculations

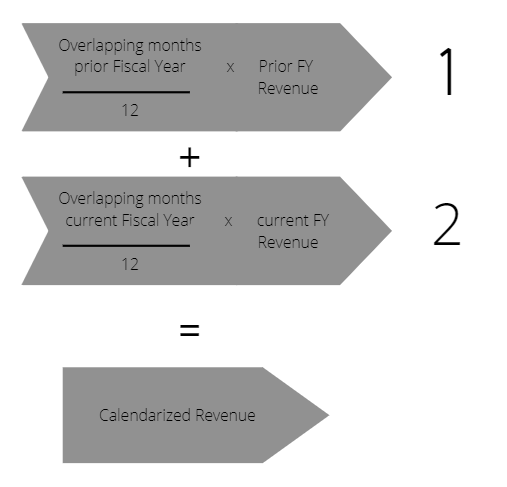

There are two steps to calculate calendarization:

1) Find Percentage Overlap from Prior FY and Multiply by Prior FY Revenue:

First, you find the number of months where the previous FY(Fiscal Year) overlaps with the aligned year-end and divide by twelve.

Then, you find the company's PFS(Previous Fiscal Year) revenue. This can be found in the company's public financial filings.

With Numbers provided by the accounting department or the client, divide the number of months by 12 and multiply the percentage overlap by the prior Fiscal Year's Revenue.

2) Find Percentage Overlap from Current FY and Multiply by Current FY Revenue:

Find the overlapped number of months of the current FY and aligned year-end. Then, find the current FY's revenue where you will use the same data sources for the numbers as in step 1. Then, divide the months by 12 and multiply the percentage overlap by the current FYR.

Example Of Calenderization

Let's assume your company's fiscal year ends on March 31, and you are responsible for calendarizing its profits.

Your company generated $60 million in revenue, which is expected to reach $70 million by the following year.

- 2022A Revenue: $60 million

- 2023E Revenue: $80 million

Year 1 Calendarized Revenue is calculated such that 75% of the data is provided by 2022A, and the remaining arises from 2023E.

- 2022A (%): 9 ÷ 12 = 75%

- 2023E (%): (12 – 9) ÷ 12 = 25%

According to these change factors(%), we multiply the percentage by the respective revenue amount.

- FYA: $60m × 75% = $45 million

- NFY: $80m × 25% = $20 million

The calendarized revenue for FYA (first adjusted year) is $65 million, the sum of the two numbers above.

Calendarization And Last Twelve Months (LTM)

The Last Twelve Months and Calendarization are both used in analyzing comparisons. Comparable company analysis compares the functioning measurements of public firms in an industry's peer group.

Size, leverage, industry, and growth attributes categorize companies into peer groups. Therefore, company assessments need a comparable analysis to accompany the overall analysis.

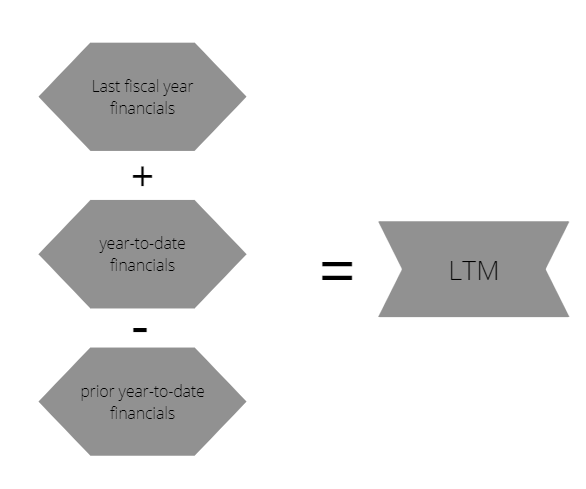

Calendarization analyzes financial statement data for a fiscal year. However, LTM analyzes the last twelve months precisely when calculating financial metrics (profits, revenue, EBITDA).

Even though one year might be a short time to test a company's performance, it is worthwhile to know its latest performance and production.

LTM figures are more "up-to-date" than annual financial reports, so they are considered a helping tool. In addition, LTM eliminates small, potentially misleading measurements, such as quarterly reports.

Investors must differentiate LTM figures coexisting with the company's latest fiscal year reports. Calendarization adjusts the fiscal year to the company or the parent, providing a fair and clear basis for the comparison.

LTM shows the preceding twelve months from the issued date of the financial statement. For example, if the financial statement date is September 2021, the LTM shows the period from October 1, 2021, to September 30, 2022.

Financial Statement and FY Consolidation

Financial statement calendarization happens when a parent company presents combined financial statements to its collaborators.

This company has to merge all financial statements, including those of its subordinate companies. These companies must follow the same fiscal year as one of the parent companies; if they follow their own FY, they will be adjusted to the pareparent's

If the FYs are different, these consolidating financial statements will not make sense and will lead to false and inaccurate financial statistics.

Example:

Suppose that WSO owns two subsidiaries, A and B. WSO'WSO's (fiscal year) starts September 1 to August 31, A has a fiscal year that begins on March 1, and B has one on May 1.

When consolidating the financial statements of WSO, A, and B, the first step is to adjust the reports of A and B to the fiscal year running from September 1 to August 31.

Also, WSO will have to note that A and B prepared their financial statements for the fiscal year for merging.

What Is Financial Consolidation?

Financial consolidation is the process of merging the financial data of a company's subsidiaries and segments, such as the entity controls, into one set of financial statements.

Logically, the assets, income, expenses, and all financial data of the controlling company and its subsidiaries are presented in a single financial statement as if they are a single entity.

Consolidated financial statements give a company's stakeholders a general view of the overall performance through several factors.

- Regulators and auditing entities depend on it to ensure the company follows the rules and regulations.

- It gives investors access to a company's financial situation, its profit or loss in the marketplace, and how it is operated and managed.

Calendarization FAQs

Some companies don't report based on the same fiscal year-end, hence we calendarize their finances. It allows companies to become fairly comparable based on the same FY comparisons.

It is a one-year time span that relates to a company's financial reporting periods. It can differ from a calendar year and they are essential to accounting.

Companies usually pick periods different from the calendar year when they have huge intra-year jumps in their business.

As an example, retailers profit significantly during the holiday season. Hence, they usually set their FYE (fiscal year end) to the end of February. This provides them with enough time to ready their numbers after the huge mess of the holiday season.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?