Fully Depreciated Asset

Assets whose book value has been reduced for the entire useful life of the asset, adding up all depreciation from all years.

What Is a Fully Depreciated Asset?

A fully depreciated asset is when its book value has been depreciated for the useful period after accumulating all years' depreciation.

If a corporation decides to take a full impairment charge against an asset, it immediately depreciates it, leaving just its salvage value—sometimes referred to as its terminal value or residual value—remaining.

Depreciation can be computed using a straight-line or an accelerated technique, such as double-declining balance or the sum-of-the-years' digits method. On the company's records, an asset is said to be fully depreciated when the total depreciation equals the asset's original cost.

Depreciation costs, therefore, act as a systematic allocation of how much an asset is depleted annually. Conservative accounting methods advise utilizing a quicker depreciation schedule when unclear to err on the side of prudence.

As a result, costs can be recognized sooner, protecting the business against unanticipated accounting losses if the asset doesn't last as long as projected.

Due to these uncertainties and conservative policies, it is normal for a fully depreciated asset to still be in good operating order and to produce value for the firm.

The term "depreciable base" is frequently used to describe the gap between an asset's initial cost and residual value.

A decrease in the amount of depreciation recorded on the income statement due to the lack of depreciation expenditure will increase the organization's non-cash earnings.

Retired assets that are no longer actively used are often listed at a lower net realizable or salvage value. The accounting records promptly reflect any profit or loss from the retirement of such assets.

Removing the asset's purchase price and accrued depreciation from the accounting records would be inappropriate if the fixed asset is still being used.

- A fully depreciated asset is an asset that has reached the end of its useful life for accounting purposes, meaning its book value has been reduced to zero through depreciation expenses.

- Depreciation is the allocation of a tangible asset's cost over its useful life, reflecting wear and tear, deterioration, or obsolescence. Common methods include straight-line, declining balance, and units of production depreciation.

- The book value of an asset is its original cost minus accumulated depreciation. For a fully depreciated asset, this value is zero, indicating that the asset's entire cost has been expensed over its useful life.

- Companies must decide whether to continue using fully depreciated assets or replace them. This decision is based on factors like maintenance costs, efficiency, and technological advancements.

Example of Fully Depreciated Asset

The expenses related to purchasing and maintaining tangible assets utilized in company operations are referred to as PP&E (Property, Plant, and Equipment) expenses.

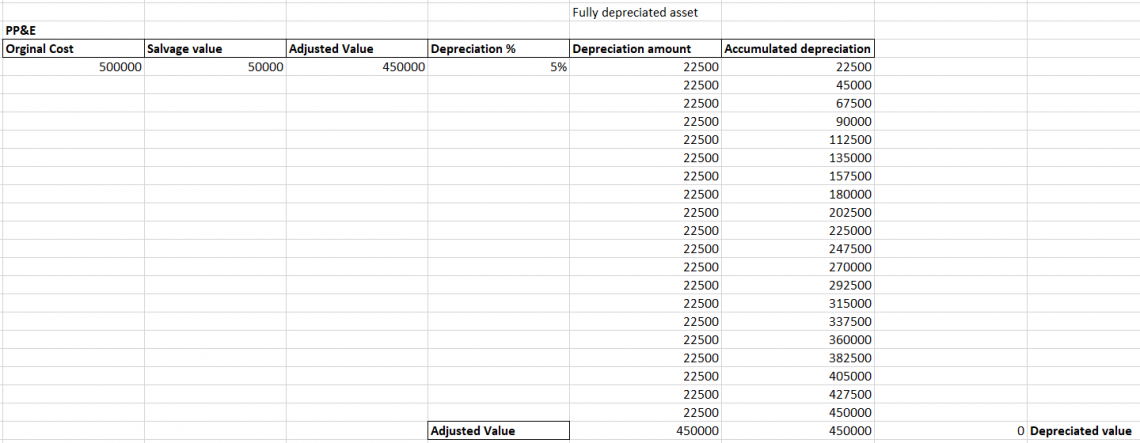

- The cost of the PP&E while buying is $500,000

- The salvage value is $50,000.

- The depreciation expense is projected to cost 5% over 20 years

The cost of an item is methodically distributed throughout its useful life through depreciation. The object will lose $22,500 [($500,000 - $50,000)/20 ] in value annually if the depreciation rate is 5%.

Depreciation costs will reach $500,000 over 20 years, nullifying the initial cost.

The asset's value falls as it is used and ages until it reaches its salvage value, which is the asset’s estimated value at the end of its useful life. Considering this example, the salvage value is $50,000, which is the residual value at the end of the PP&E.

At the end of the 20-year depreciation period, the asset's carrying amount in the books will be zero. This means that the asset's depreciation expenses have been paid and will not be incurred further.

Depreciated Asset Revaluation

Consider that a business has a fleet of automobiles that it paid $500,000 for in total some years ago.

The corporation has consistently depreciated automobiles over time, and its total accrued depreciation is now $500,000. This indicates that the fleet has no book value.

Accounting laws, such as the “Cost Principle”, preclude the corporation from revaluing the assets on the balance sheet, even though the vehicles are still in service and may have a market worth higher than their initial cost.

As a result, the corporation cannot change the completely depreciated automobiles' book values to reflect their actual market worth.

Therefore, notwithstanding its potential market worth, the fully depreciated fleet will continue to be reported with a zero book value on the company's balance sheet.

This is because revaluation is not permitted after an item has fully depreciated, and assets must be recorded at their original cost.

Accounting for Fully Depreciated Assets

Fully depreciated assets (FDA) greatly impact the balance sheet and the income statement. An asset's entire depreciation impacts the balance sheet items property, plant, and equipment (PP&E) and accumulated depreciation.

The financial accounts will affect whether an asset is still being used or sold. The balance sheet will continue to show the asset as fully depreciated even though it is still being used for business purposes.

However, at this time, the asset's value and total depreciation will be equal. A balance sheet entry is not necessary until the asset is sold. The income statement will no longer include depreciation expense, increasing operating profit.

This is so that no more depreciation expense is reported moving forward, as the full depreciation shows that the asset has been fully utilized.

Assets with accumulated depreciation are eliminated from the balance sheet when they are fully depreciated and sold. Any gains or losses from selling the asset will be reflected on the income statement, and the sale will be recorded separately.

| Assets | Amt (xxx) | Liability | Amt (xxx) |

|---|---|---|---|

| Current Asset | Current Liability | ||

| Cash | 500 | Accounts Payable | 300 |

| Accounts Receivable | 100 | ||

| Total Current Asset | 600 | Total Current Liability | 300 |

| Fixed Asset | Shareholder’s Equity | ||

| Machinery Less: Accumulated Depreciation |

2000 (2000) |

Equity | 300 |

| Total Assets | 600 | Total Liabilities | 600 |

An asset's reduced carrying value is shown on the balance sheet once it has been fully depreciated, but it may continue to be recorded together with accumulated depreciation up until disposal.

The absence of depreciation expense has an influence on the income statement and raises operating profit. Whether fully depreciated assets are still in use or have been sold affects how they are handled.

Impact of Fully Depreciated Asset

In the provided case, the corporation possesses a piece of equipment worth $100,000. The equipment has a five-year projected useful life and no salvage value.

The depreciation expense for the equipment is $20,000 per year over a 5-year period. If the equipment is used for another three years, no more depreciation expenditure will be recorded during that time.

As a result, the equipment will have a balance sheet book value of $0 while still representing its $100,000 initial cost and $100,000 accrued depreciation.

The idea that completely depreciated assets have book values of zero (or salvage value) emphasizes the idea that depreciation is a way to spread out the expense of an item throughout its useful life.

The current value or worth of the asset is calculated without using depreciation. The balance sheet shows the existence of an asset even after it is sold or is no longer in use.

Fully depreciated assets still in use are recorded at their original cost on the balance sheet, and their cumulative depreciation is added to the overall accumulated depreciation.

The equipment will be recorded on the balance sheet with a book value of zero, suggesting that its value has been entirely allocated during its useful life through depreciation.

Pros of Fully Depreciated Asset (FDA)

A fully Depreciated Asset has several advantages in evaluating and considering the ongoing asset value.

The following are the advantages:

- Cost Savings: The business is no longer required to record fully depreciated assets, and the depreciation cost is no longer recorded, resulting in cost savings.

- Increased Profit Margins: Since a fully depreciated asset has no book value left, it does not affect the company's net income or profit margin estimates. This may offer a more accurate picture of the business's profitability.

- Extended Use: Fully depreciated assets that may be used indefinitely by the business no longer have depreciation charges, but it's crucial to remember that they could still need regular maintenance in order to be used by the company.

- Asset Replacement Planning: Fully depreciated assets may be identified and tracked, which helps businesses better plan for asset replacements or improvements. Knowing which assets have outlived their usefulness aids in budgeting and strategic investment decision-making for the future.

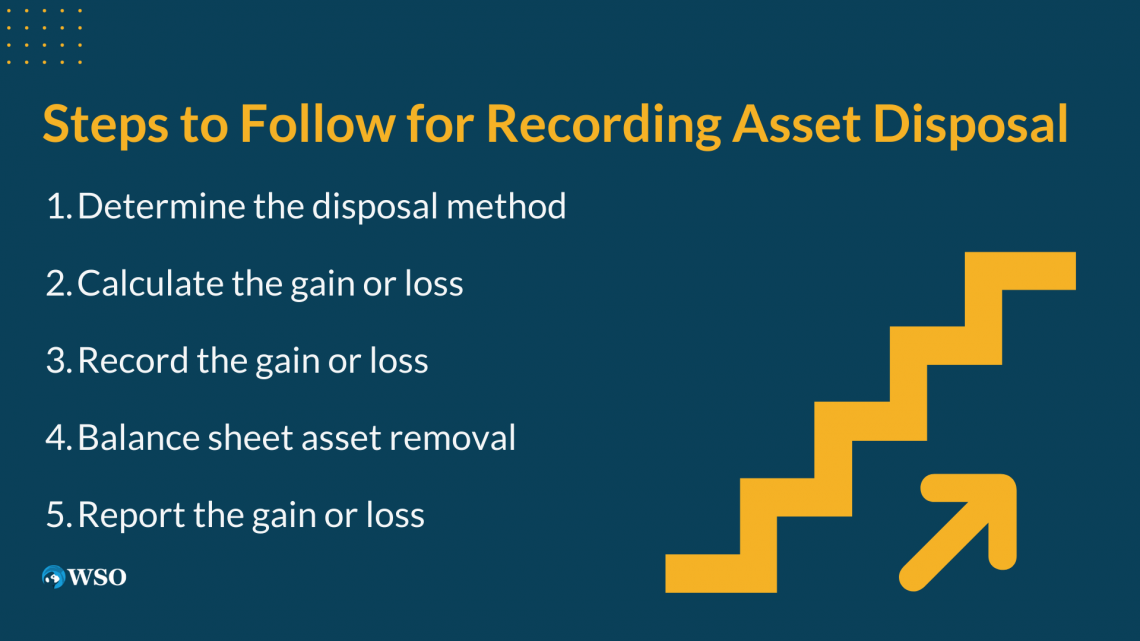

Steps to follow for Recording Asset Disposal

The process of disposing of assets requires deleting them from the accounting records, which essentially deletes them from the balance sheet.

The term for this is derecognition. The following are the steps to follow for recording asset disposal,

1. Determine the disposal method

Decide how the asset will be disposed of, whether through retirement, sale, salvage, or another method. This choice will impact how the disposal is recorded.

2. Calculate the gain or loss

Compare the proceeds from the disposal (e.g., sale price) with the asset's net book value. The net book value is the asset's original cost minus the accumulated depreciation. If the proceeds exceed the net book value, there is a gain. If the proceeds are lower, there is a loss.

Gain / Loss = Proceeds from Disposal - Net Book Value

3. Record the gain or loss

Create an entry to record the gain or loss on disposal. Debit the accumulated depreciation account to remove the accumulated depreciation from the books.

Credit the asset account to remove the asset from the books. Finally, credit or debit the gain or loss account to reflect the gain or loss from the disposal.

| Account | Debit ($) | Credit ($) |

|---|---|---|

| Accumulated Depreciation | xxx | |

| Asset | xxx | |

| Gain/Loss on Disposal | xxx |

4. Balance sheet asset removal

Remove the asset's initial purchase price and any accrued depreciation from the balance sheet, bringing the asset's value to zero.

This ensures that the asset is no longer included in the company's financial records.

5. Report the gain or loss

Include the gain or loss on disposal in the income statement for the reporting period when the removal occurred.

This helps provide a comprehensive view of the financial results and performance for that period.

Impact of Taxes on Fully Depreciated Assets

Factors include the complexities of tax regulations and making informed decisions regarding the disposal of fully depreciated assets.

The following is the impact of taxes on fully depreciated assets:

- Tax Basis: A property's tax basis is normally zero after fully depreciating. This indicates that the asset is treated as having no residual value for tax purposes. There could not be any further depreciation deductions available as a consequence.

- Capital Gains: A completely depreciated asset may generate a capital gain if it is sold for more than its tax basis. Taxes are typically levied on capital gains. The asset's holding time and local tax regulations are just two of the variables that will affect the relevant tax rate for capital gains.

- Regular Income: In some circumstances, the earnings from the sale of a wholly depreciated asset may be categorized as regular income rather than capital gains.

- This usually happens when an item, like inventory or stock in trade, is thought to be held mainly for sale to clients in the regular course of business. Ordinary income tax rates are typically applicable to regular income.

- Depreciation Recapture: If the completely depreciated asset is subject to depreciation recapture laws, the taxable gain from the sale can be regarded as ordinary income rather than capital gains. Recapture of depreciation deductions is the goal of depreciation recapture provisions.

- Tax Losses: If the sale price of a completely depreciated asset is less than its tax basis, a capital loss may occasionally occur. Depending on certain tax laws and restrictions, capital losses may be carried forward to offset future capital gains or utilized to offset capital gains in the same tax year.

- Tax reporting and compliance: The sale of completely depreciated assets must be disclosed accurately, and all applicable tax laws and regulations must be followed. Failure to do so may result in fines and other tax responsibilities.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?