Marginal Cost of Production

The cost incurred on each additional unit of output produced.

What Is The Marginal Cost Of Production?

The Marginal Cost of Production is the cost incurred on each additional unit of output produced. It can be defined as the change in the total cost of production upon the change in total output.

That is, at any given level of output y, we can ask how costs will change if we change output by some amount Δy.

Marginal Cost of production = Change in Total cost / Change in output = ΔCost / Δy

Since we frequently take the change in output to represent one unit of output, the marginal cost shows how much more expensive it would be to produce an additional discrete unit of product.

Marginal Cost measures a rate of change: the change in costs divided by a change in output. It appears to be a straightforward rise in costs when the output changes by a single unit, whereas it is a rate of change as that single unit increases the output.

The company may return a profit if the marginal Cost of production is lower than the product's unit price.

- The marginal cost of production refers to the additional cost incurred by producing one more unit of a good or service.

- The marginal cost of production is a key concept in economics and cost accounting, representing the change in total production costs resulting from a change in production quantity.

- On a cost curve, the marginal cost curve typically has a U-shape, initially decreasing due to economies of scale and then increasing as diseconomies of scale set in.

- When production increases, marginal costs are lower due to efficiencies gained from higher production volumes, such as bulk purchasing of materials or more efficient use of labor and machinery.

Examples of Marginal Cost of production

To understand the marginal Cost, we first need to understand what the total Cost represents.

The total Cost comprises two types of Cost:

1. Fixed Cost

Fixed costs are the costs that do not change with a change in output produced, i.e., remain constant. An example of a fixed cost is the rent that a factory pays, independent of the output produced.

A fixed amount of rent is paid each month irrespective of whether the production increases or decreases.

2. Variable Cost

Variable costs are those that vary with the change in output produced. Examples include the Cost of raw materials, labor wages, delivery costs, etc.

NOTE

Marginal costs are not affected by a firm’s fixed Costs, and we know that fixed costs do not vary with changes in the output level. MC can also be expressed as ∆VC/∆Q instead of ∆C/∆Q.

Marginal Cost can be categorized into two types depending on time-

1. Short-run Marginal Cost

In the short run, firms incur a fixed cost of production. Therefore, short-run marginal Cost is defined as the additional cost of producing an extra unit of output when all inputs are fixed.

This happens because, in the short run, firms own a fixed asset. For example, they are not allowed to buy new machinery.

2. Long-run Marginal Cost

In the long run, firms can change their input, for example, by buying new machinery. Therefore, a Long-run marginal cost is defined as the additional cost of producing an extra unit of output when all inputs are variable.

Because of this, even if short-run marginal Cost increases due to capacity limitations, long-run marginal Cost can remain constant.

Marginal Cost and economies of scale

The producers generate more output as long as their profit is maximized, i.e., the point where marginal revenue equals their marginal Cost of production.

Once the firm knows its marginal Cost, it's easier for them to create an optimal marginal revenue to increase profits.

Economies of scale happen when output is very small, and labor specialization is impossible. As output increases, labor can specialize, leading to more efficiency and a fall in the average cost of production. For this to happen, the marginal cost must remain below the average total Cost.

Most companies strive for economies of scale. Expanding while maintaining or increasing profits is ideal for a business. It allows the company to grow and generate higher profits for the organization.

Diseconomies of scale occur when output increases significantly and management becomes overstretched, causing inefficiency. In this case, a firm’s marginal Cost of production increases because it might now have to incur an additional cost of expansion.

NOTE

If a company increases production at diseconomies of scale, it risks average total Cost becoming greater than its average profits. This would mean the company is losing money and cannot meet demand without going bankrupt.

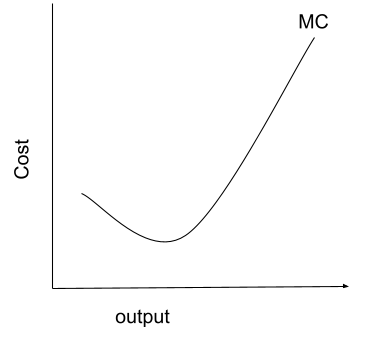

Marginal Cost curve

The marginal cost curve illustrates the relationship between a firm's marginal Cost of producing a good or service and the volume of output the firm produces.

To understand the shape of the cost curve for MC, let us see a small derivation for the relation between the marginal product of labor and marginal Cost.

VC = w.L(Q)

Marginal Cost = dVC / dQ = w.dL(Q) / dQ = w / MP

Where,

- VC = Variable Cost

- W = Wage

- L = Labor

- MP = marginal product of labor = dQ/dL

Thus, MC = w / MP

Marginal Cost and the marginal product of labor have an inverse relation. When marginal product increases (labor becoming more productive), marginal cost decreases (the additional Cost of employing labor decreases).

Thus, the marginal cost curve is a U-shaped curve with Cost on its y-axis and output on the x-axis. The marginal cost curve can also be referred to as a firm’s supply curve in a perfectly competitive market.

Increasing production capacity will be costly if the marginal Cost per unit is high. On the other hand, a corporation may obtain economies of scale by using reduced fixed costs in particular production lines if its marginal cost of production is low.

Marginal Cost of Production Vs. Average Cost of Production

The average cost of production is the total Cost divided by the total number of goods. In contrast, marginal cost gives us the change in total Cost relative to the change in total output.

The average Cost is used when firms have to minimize their costs, whereas the marginal Cost is used when firms want to maximize their profits.

Just like total costs, average costs comprise two kinds of costs-

- Average fixed Cost

- Average variable Cost

Similar to marginal costs, average costs can be categorized into two

- Short-run average Cost

- Long-run average Cost

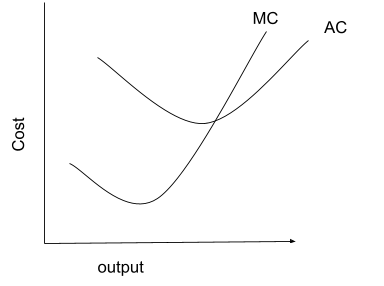

The average cost and marginal cost are closely related. Below is the diagram that illustrates the relationship between the two-

When the average cost increases, the marginal Cost is always greater than the average Cost. Since the marginal Cost is the value of the additional Cost added to the average, it tends to raise the average Cost's value if it is larger than the marginal Cost.

Similarly, when the average cost decreases, the marginal Cost is always lower than the average.

Average Cost typically exceeds marginal Cost at low production volumes because fixed costs are included in the average Cost and not in marginal Cost.

An analogy to better understand the concept is that suppose you scored 80 in your economics exam, and on the next exam, you scored 75. Now, this score will pull your average down. Your new average score in the economics exam is less than 80.

Suppose you scored 85 in your economics exam and 90 in the next exam, which will increase your average. Your new average score in the economics exam is greater than 85.

In both cases, the current average score is the average Cost, and the score in the next exam is the marginal Cost.

MC < AC => AC is decreasing

MC > AC => AC is increasing

Marginal Cost and Average Variable Cost

In economics, the average variable Cost is the Cost per unit. It is calculated by dividing the entire variable Cost by the output.

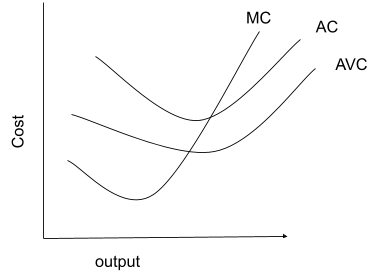

Businesses use the average variable Cost to decide when to stop short-term production. Below is a graphical representation of MC, AC, and AVC.

The Marginal Cost and average variable Cost have a similar connection. The average variable Cost falls when the marginal Cost is lower than the average variable Cost. The average variable Cost rises when the marginal Cost exceeds the average variable Cost.

When MC exceeds AVC, AVC rises as output increases. Following that, both AVC and MC rise, but MC rises more quickly than AVC. Because of this, the MC curve is steeper than the AVC curve.

Since neither average variable Cost nor marginal Cost has a fixed cost component, in some circumstances, this also means that average variable Cost assumes a U-shape.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?