Quantity Supplied

The volume of goods or services suppliers will make an offer for sale at a specific market price.

What Is Quantity Supplied?

Quantity Supplied in Economics refers to the volume of goods or services suppliers will make an offer for sale at a specific market price. Since price variations affect how much supply producers put on the market, the quantity supplied is different from the actual amount of supply (i.e., the total supply).

The price elasticity of supply describes how supply adjusts in response to price changes. The quantity produced and sold by enterprises at a specific market price is the amount supplied.

A change in the quantity that is supplied results from a difference in the price level. Price elasticity of supply is the term used to describe variation.

Therefore, the amount supplied relies on the price level. The price of a product can occasionally be controlled by a regulatory authority using price ceilings or floors.

A price cap requires vendors to set a maximum price at which they will sell their products or services. Rent regulations in New York are an illustration of a price cap. Suppliers will sell fewer of their goods after a price cap is in place since there will be no incentive to increase sales given the price cap.

There is a price floor when the supply cannot charge or pay below a specific price. The minimum wage is a prime illustration of a price floor.

The number of finished goods and services that suppliers are willing to manufacture and sell in the market at a specific price is known as the quantity provided in economics.

This amount fluctuates at various price points, but generally speaking, the higher the price, the more likely producers will be prepared to offer consumers goods and services.

The sole factor influencing the quantity offered is pricing. This means that a change in the price of a given commodity or service is the only thing that can lead suppliers to alter the quantity they produce of that good or service.

Because they will make more money, suppliers are prepared to supply more goods at a higher cost. As a result, supply—the sum of the quantities supplied at different prices—should not be confused with the amount provided.

Furthermore, the amount supplied, which depends on a specific price level typically set by the government or by market forces, is not affected by changes in supply; instead, it is the price elasticity of supply that changes in response to changes in the price of products and services.

- Quantity supplied is the total amount of a good or service that producers are willing and able to sell at a specific price over a given period, represented on the supply curve.

- The law of supply states that all else being equal, there is a direct relationship between the price of a good and the quantity supplied.

- The supply curve graphically represents the relationship between the price of a good and the quantity supplied. It typically slopes upward from left to right, reflecting the law of supply.

- Understanding the quantity supplied is crucial for businesses and policymakers as it helps in setting prices, planning production, managing inventory, and formulating economic policies.

Understanding Quantity Supplied

Prices are limited, and the quantity offered is price-sensitive. In a free market, higher prices typically result in higher doses being supplied, and vice versa.

However, the entire present supply of finished items serves as a restriction since there will come a time when prices rise to the degree that it encourages future producers to increase the quantity produced.

In situations like this, the continued demand for a product or service typically prompts additional investment in its expanding production.

Depending on the good or service, several distinct factors limit the capacity to lower the quantity given when prices are reduced. One is the supplier's operational cash demands.

Because of the need for cash flow, a supplier may frequently be forced to forgo profits or sell products at a loss.

This is frequently observed in the markets for commodities where oil barrels or pork bellies must be transported because production levels cannot be immediately reduced.

Additionally, there is a practical limit to how long and how much of an item may be kept on hand while awaiting a more favorable pricing climate.

The price level, which can be established by market forces or a regulating body employing price ceilings or floors, determines the quantity supplied.

Increasing earnings is the aim of suppliers. Suppliers generally control how many products are produced in the market at different price points, but they have little influence on how many are wanted.

When market forces are allowed to function naturally without any interference from the government, consumers will be able to purchase things at the best price.

The relationship between customers and suppliers is inverse because consumers seek to purchase things at the lowest feasible price while suppliers want to offer their goods for a high price.

Therefore, the optimal qty supplied is at the point where suppliers and consumers converge and where the supply and demand curves overlap. Therefore, the price point of equilibrium is where it is.

Customers are willing to pay for these things, and suppliers are eager to make and provide them at that price point. Therefore, suppliers are recommended not to alter their supply amount at a price equilibrium to ensure optimal earnings.

This is because, during price equilibrium, demand is constant because an increase in supply would increase the number of unsold items for the suppliers, and a decrease in supply would result in a reduction in revenue.

Quantity Supplied Under Regular Market Conditions

In the graph below, the supply and demand curves are shown. Quantity is on the y-axis, and the price is on the x-axis. The inverse relationship between supply and demand is demonstrated by the upward-sloping supply curve and the downward-sloping demand curve.

Because manufacturers are prepared to offer more products at a higher price, the supply curve is upward-sloping. Consumers will demand fewer units at higher prices and purchase fewer units at a higher price for a given good, which causes the demand curve to drop downward.

Quantity Supplied Under Normative Market Circumstances

The optimal quantity delivered is the amount that fully satisfies current demand at market prices. The known supply and demand curves are shown on the same graph to determine this quantity. Quantity is plotted on the x-axis, and demand is plotted on the y-axis in the supply and demand graphs.

Because manufacturers are eager to offer more of an item at a higher price, the supply curve is sloping upward. But conversely, the demand curve slopes downward because people buy fewer units of an item when the price increases.

The point at which the two curves converge is the equilibrium price and quantity. The price at which both the amount that producers are willing to supply and the portion that consumers are eager to buy is equal is the equilibrium point.

The amount to supply for market equilibrium is this. A supplier loses out on potential income if it provides a lower amount. Not all of the products it gives will sell if it delivers significantly.

Factors Affecting the Quantity Supplied

The factors affecting the quantity supplied are:

- Other product prices: The supply of an item whose price does not rise will become less alluring to suppliers if the price of other goods produced with the same resources increases. Therefore, they will switch to producing expensive commodities, such as yogurt, instead of fresh milk to increase earnings.

- Manufacturing costs: This depends on the production variables' cost, i.e., wages, interest rates, land rents, raw material costs, and expected profits. Supply typically decreases as prices rise and vice versa.

- On the other side, producers will switch from providing commodities whose manufacture is dependent on labor to providing goods where labor use is less significant due to an increase in the price of one factor, like labor.

- Technology Developments: Technological advancements and innovations lower production costs, boost productivity and improve the amount of a sound produced with the same or fewer inputs.

- Climate: A region's changing weather may impact a commodity's availability. The majority of this has to do with agricultural items (drought or good weather)

- New Findings: The output will inevitably rise if new raw materials, like oil, are discovered because the inputs will be less expensive.

- Governmental Rules: The quota system, embargo, tax, and subsidies are some of the ways the government might limit the quantity of an item produced or supplied.

Factors that Shift the Supply Curve

The price of other items, production costs, and technological advancements significantly impact the supply curve.

Technology

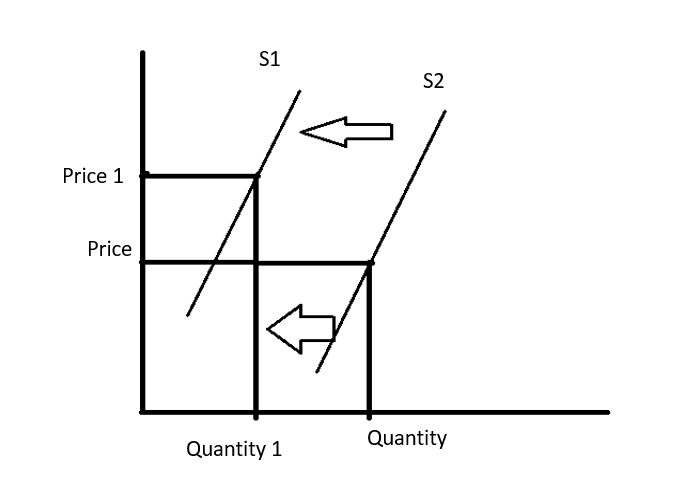

Technological advancements can increase supply and improve process efficiency. The amount that can be produced at a given price increases due to these advancements, which move the supply curve to the right.

Production may suffer if technology does not advance and degrades over time, forcing the supply curve to shift to the left. The supply curve moves to the right when production processes are improved by technology.

Price of Production

All other factors being equal, the supply curve will shift to the right when the cost of producing a commodity rises (less will be able to be produced profitably at a given price).

As a result, supply shifts the other way in response to changes in production costs and input prices. Supply declines as production costs rise and vice versa.

Payroll and manufacturing overhead are a few examples of production costs. The supply curve shifts to the right (increasing supply) when production costs fall as labor and overhead costs go down.

The supply curve has an inverse relationship between production costs and input prices. As a result, an increase in input and production costs will cause the supply curve to alter in the opposite direction and vice versa.

The supply curve will move to the right, for instance, if manufacturing overhead expenses decline because it is now less expensive to manufacture a good or service.

Cost of Other Items

The cost of other products or services may impact the supply curve. Other products can be divided into producer alternatives and joint developments.

Joint products are goods created in collaboration. Producer replacements are alternatives that can be made from the same raw materials.

For a business that raises steers, leather, and meat are common goods. These goods are created in tandem.

The cost of a product and the availability of its joint product are directly related. For example, ranchers grow more cattle when the price of leather rises, increasing the availability of beef (the result of leather joints).

The producer can now create one good or another for a producer substitution. For example, think of a farmer who has the option of growing maize or soybeans. Farmers will want to grow more corn if corn prices rise, reducing the availability of soybeans.

As a result, there is an inverse relationship between a good's price and its producer substitute's availability.

The items or services must be related, and customers must believe the relationship is essential for it to impact the supply curve. Joint products are distinct from product alternatives.

Corn and soybeans are two products that can be substituted since they share a common resource (farmland). Farmers will plant more soybeans if corn prices fall, and there will be more space for growing them. Therefore, it expands the soybean supply.

Market Forces and Quantity Supplied

Since all market participants can respond to price signals and modify their expectations, market forces are typically viewed as the most excellent means to guarantee that the quantity offered is optimal.

Nevertheless, the government or a government entity may specify or influence the quantity of some products or services given.

As long as the body that sets prices has a good understanding of the actual demand, this should, in principle, function as intended. Unfortunately, suppliers and consumers may suffer when price controls are not implemented at levels resembling a market equilibrium.

Suppliers are compelled to offer a good or service that may not cover production costs, including a typical margin if a price cap is too low.

This may result in losses and a decrease in producers. Consumers are compelled to use more of their income to cover their essential needs if a price floor is set too high, especially for basic commodities.

Most of the time, suppliers try to maximize earnings by charging high prices and selling many products. While suppliers typically have some influence over the number of commodities on the market, they have no such control over consumer demand for items at various price points.

Consumers share authority over how commodities are sold at set pricing as long as market forces are permitted to operate unhindered by legislation or monopolistic supplier control. Therefore, the ability to fulfill consumers' needs for goods at the most affordable price is essential.

Consumers might limit their purchases if a good is fungible or luxurious or look for alternatives. Because of this emotional conflict in a free market, most items are cleared at competitive rates.

According to economic theory, the goal of markets should be to reach equilibrium; however, several factors work against this goal. First, many markets are not free to operate because outside factors like government control influence supply.

The elasticity of supply and demand is a crucial additional component to consider. When supply or demand is elastic, they adjust to price changes, while when they are inelastic, they do not. It is the cause of the intermittent equilibrium of inelastic products and services.

Supply vs. Quantity Supplied

The phrases "supply" and "quantity supplied" are used in economics.

The term "supply" refers to the volume of goods or services a specific business will offer to a market.

The supply is represented in a supply curve and graph to simplify and more easily illustrate the relationship between prices and quantities. In addition, the entire range of potential costs and available quantities are included.

The term "quantity supplied" refers to a particular location on the supply curve. It depicts how much quantity is supplied or how much is prepared to be offered for a specific market price.

The two terms can be represented by graphs. The whole supply curve, including all possible prices, quantities, and crossings, can be represented graphically as "supply."

The supply curve shows the "quantity that is supplied." It is one special place where a specified quantity and price meet.

The supply curve moves to the right as the supply grows. If this occurs, both the quantity and the potential market price increase. Numerous factors influence the supply. The shift is to the left as an indicator of decreasing supplies.

A change in the supply can result from a variety of other factors:

- Changes in the prices of commodities.

- Production costs (which include changes in output, resources, labor, and other related items).

- Prices of related goods (about market competition and other sellers).

- Technology in use.

- Environmental events like natural disasters.

- Economic crises, taxes or subsidies, and indirect taxes.

These are just a few examples. The expectations of the market, together with the preferences, means, and interests of potential customers, should also be taken into account.

Moving from one point (of the quantity delivered) to another is how the quantity supplied is described.

The movement is frequently brought on by changes in the cost of a good or service. The potential market prices and the potential quantity are typically both impacted by the movement in the supply curve, whether a fall or an increase.

On the other hand, the supply curve as a whole may only be slightly affected by a change in the quantity delivered.

Comparison chart:

| Basis | Supply | Quantity Supplied |

|---|---|---|

| Meaning | The term "supply" refers to the overall relationship between various prices and the volume of goods sold at each price. | It is the total amount of a product made available for purchase over a specific period at a specific price. |

| Represents | What can the market provide? | Quantity of commodities made available by producers in exchange for a set price. |

| Indication | Availability calendar or supply curve | The point of the supply curve gave way. |

| The Cause of Change | Change in factors other than price | Price variations |

| Spotting the Change | A shift in the supply curve | The entire supply curve changes (Movement along the supply curve). |

Quantity Supplied Examples

Think about a company that sells cars, Green's Auto Sales. As summer approaches, the automaker's rivals have been hiking prices. So as opposed to the prior average selling price of $20,000, the average car in their market now sells for $25,000.

To maximize revenues, Green decides to increase its car supply. Before the summer, it was generating $2 million in revenue by selling 100 automobiles each month. Each car cost $15,000 to produce and sell, resulting in a $500k net profit for Green.

A $25,000 average selling price results in a $1 million monthly net profit. Thus, increasing the supply of cars will boost Green's revenue.

Let's take another example.

Jonathan is the owner of a modest grocery business. He offers things from the bakery, fresh veggies, and meat.

In addition, he offers frozen meat and tinned goods. Jonathan has seen that as the holiday season draws near, his rivals have increased the price of beef meat from $6.13 per pound to $6.62 per pound.

Jonathan believes that expanding the beef meat supply can increase his revenue.

Jonathan was making a gross profit of 50 x $6.13 = $306.5 a day before the price of beef meat increased by selling about 50 pounds each day. Jonathan's net profit was $6.13 - $3.20, or $2.93 per pound, given that the price of beef meat was $3.20 per pound.

With the beef meat price now at $6.62, Jonathan will make a net profit of $3.42 per pound ($6.62 - $3.20). He will make even more money if he increases the amount of beef flesh supplied.

Quantity Supplied FAQs

Quantity supplied is the precise amount supplied at a specific price, whereas supply is the overall supply curve. Supply, in general, describes all the various characteristics offered at all conceivable price points.

The precise quantity of an item or service desired at a specific price is known as the quantity demanded. Demand can also refer to a buyer's capacity or willingness to pay for a good or service at the quoted price. Demand graphs show the total quantity of demand for each price.

The price of the commodity, the buyer's income, the cost of associated commodities, consumer preferences, and the customer's expectations for future supply and price are the five main elements that influence the quantity demanded.

In a market economy, interactions between producers and consumers will establish the equilibrium price and quantity.

Similar to this, the law of supply states that manufacturers supply less as prices drop. The price and the amount that will be bought and sold in a market are determined by demand and supply working together.

The point where supply and demand converge determines equilibrium price and quantity. The equilibrium price, quantity, or both will inevitably change in response to changes in supply, demand, or both. A shortfall brought on by a rise in demand will raise both the equilibrium price and equilibrium quantity.

A market-clearing price, also known as an equilibrium price, is the cost of an item or service at which the quantity provided and demand are equal. According to the idea, markets typically gravitate toward this price.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?