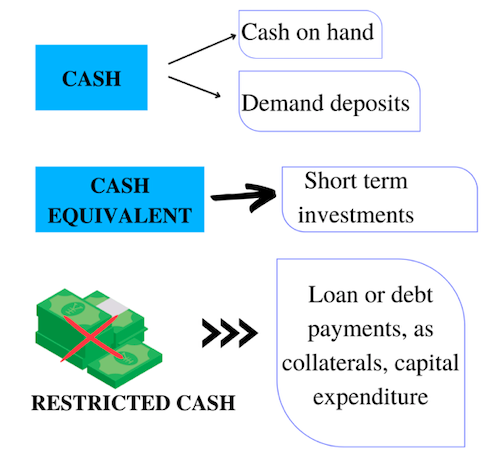

Restricted Cash

Cash set aside for a specific purpose, making it unavailable to the company for immediate or general corporate use.

What is Restricted Cash?

The term restricted cash refers to cash set aside for a specific purpose, making it unavailable to the company for immediate or general corporate use. Conversely, unrestricted cash is readily available for general business use on an immediate basis.

The cash is held in a special account and therefore remains separate from the rest of the business's cash and cash equivalents.

Since it is not considered a part of the liquidity source, it is excluded when calculating various liquidity ratios. Therefore, it appears as a separate entity from the cash and cash equivalents on the company’s balance sheet.

Restricted cash can be classified as either a current or non-current asset, depending on the period of restriction:

- When the cash is expected to be used within the current accounting year, it falls under the current asset.

- However, if the cash is anticipated to remain unavailable for more than a year, it is classified as a non-current asset.

Key Takeaways

- Restricted cash is earmarked for specific purposes, not for immediate use, unlike unrestricted cash.

- It can be either a current or non-current asset, depending on how long the money is restricted.

- Companies use restricted cash for securing loans, ensuring service delivery, collateral, and funding specific expenses.

- It's displayed separately on the balance sheet with details about the restriction.

- Accounting standards (IFRS and GAAP) handle restricted cash differently, and it's excluded from liquidity ratios like the quick ratio. Compensating balances are a type of restricted cash reported on financial statements.

why do companies Use Restricted Cash?

The restriction may exist for a specific period or until a certain event occurs. These limitations might apply to money saved in escrow accounts, which can only be used for a specific function.

Below we enlist the reasons of why companies use restricted cash:

1. Loan payments

A company receiving a bank loan may be required to maintain a certain amount of cash as restricted cash. This is done to ensure partial security for a certain time.

The company then holds this money under a new account, where it maintains the percentage of the loan (specified by the bank) as restricted cash.

2. To ensure services are met

Customers who deal with services delivered only after full payment may request through a contract that the firm not utilize the funds until the service is delivered.

3. As collaterals

An insurance provider may demand that a business put up a specific sum of money as risk-reduction collateral.

4. Debt payments and Capital expenditure

A company is not always legally obligated to restrict cash. Sometimes a firm may reserve a specific sum of money to pay off long-term debt or start a new project such as setting up a new plant or buying equipment.

Capital expenditure = Current assets - Current liabilities

The capital expenditure is calculated as the difference between the current assets and the current liabilities.

Restricted Cash Examples

Restricted cash serves as a financial safeguard and compliance tool for businesses, encompassing various scenarios where funds are legally bound for specific purposes, from securing credit lines to fulfilling customer contracts and meeting regulatory requirements.

Some examples are:

- Let us say company X is a large rubber manufacturer. The bank requests that the company open a limited cash account (which can be a separate account) and maintain a balance of $18,000, or 8% of the entire amount borrowed, to draw a $300,000 line of credit. This minimum reserve must be maintained throughout the stipulated period. So restricted cash is legally binding in this case.

- Now say the same manufacturing company receives an order and is paid half by the customer. The customer may state in their contract that the manufacturer deposits this amount to a separate account and does not use it until the order is fulfilled. The company then accounts for this payment as restricted cash.

- When buying a house, a portion of the purchase price may be placed in an escrow account until all conditions of the sale are met, such as inspections or repairs. This amount is considered restricted cash until the sale is finalized.

- Certain industries, like healthcare or insurance, may have regulations requiring companies to set aside funds in a restricted account to cover future claims or liabilities.

Restricted Cash On The Balance Sheet

When accounting for financing restricted cash, it is important to note that it is presented distinctly on a company's balance sheet, separate from regular cash and cash equivalents.

To ensure clarity regarding the distinction, between cash and regular cash and cash equivalents companies list restricted cash separately on their balance sheets under the designated category of "Restricted Cash."

Additionally, depending on how long the cash is restricted for, the line item may appear under current assets or non-current assets. Cash that is restricted for one year or less is categorized under current assets, while cash restricted for more than a year is categorized as a non-current asset.

These restricted cash amounts are typically recorded on the right-hand side of the balance sheet, in the balance column.

Moreover, the rationale behind the cash being restricted is disclosed in detail within the accompanying financial statement notes, providing transparency and clarity about its purpose and limitations

Certainly, here's a bullet list summarizing the key points about accounting for financing restricted cash:

- It appears as a separate item from the cash and cash equivalents on the company’s balance sheet.

- It is then classified as a current or non-current asset depending on its period of restriction.

- The amount of cash that accounts for the restricted money is added on the right-hand side of the balance sheet (the balance column).

- The reason for the cash being restricted is revealed in the accompanying financial statement notes.

Source: Wikipedia

The total must reconcile to the same amounts on the statement of assets and liabilities.

Consequently, direct third-party cash receipts and restricted cash payments are categorized as cash flows from operating, investing, or financing activities.

However, the transfers between unrestricted and restricted cash and equivalents are not presented as cash flows from operating, investing, or financing activities.

The purchase price is obtained by deducting the company’s net debt from the enterprise value (EV) at the date of closing. While calculating the net debt, the cash and bank balances shall always consider unrestricted cash (free cash).

IFRS and GAAP

IFRS and GAAP accounting standards handle restricted cash differently. IFRS lacks a precise definition, raising placement questions in the statement of cash flows. Under IFRS, 'cash equivalents' must be readily accessible, but disclosure is required for significant restrictions.

In contrast, GAAP combines restricted funds with cash and cash equivalents on the statement of cash flows, reconciling the two totals

1. Under IFRS (International Financial Reporting Standards)

There is no definition of "restricted cash" in the IFRS Standards, and it is unclear whether restricted sums should be included in the beginning or ending balances of a company's cash and cash equivalents in the statement of cash flows.

However, among other requirements, the quantities must either be held in hand, quickly convertible into known amounts of cash, or accessible for withdrawal at any time without penalty to fit the definition of cash and cash equivalents.

The primary need for "cash equivalents" is that they are held for short-term cash needs rather than long-term planning or other uses.

IAS 7 mandates disclosure of the quantity and a description of the restriction in cases where considerable amounts are not readily usable by the group.

2. Under GAAP (Generally Accepted Accounting Principles)

According to US GAAP, restricted funds are included in total cash and cash equivalents in the statement of cash flows even if they are shown separately from cash and cash equivalents on the balance sheet. The company then compares the two totals for cash and cash equivalents.

Calculating Liquidity Ratios with Restricted Cash

When calculating liquidity ratios, such as the current ratio and the quick ratio, with restricted cash, it's essential to consider the impact of restricted cash on these ratios.

Here's how you can calculate these ratios and make adjustments for restricted cash:

-

Current Ratio (CR):

Current Assets / Current Liabilities

- Include Restricted Cash: If restricted cash is not readily available for general use, it should be excluded from current assets when calculating the current ratio. This is because restricted cash cannot be used to meet current obligations.

-

Quick Ratio (QR) or Acid-Test Ratio:

(Cash + Cash Equivalents + Marketable Securities) / Current Liabilities

- Exclude Restricted Cash: Restricted cash should not be included in the quick ratio calculation since it is not part of the company's readily available liquid assets.

Keep in mind that the adjustment for restricted cash can affect these ratios significantly. If a company has a substantial amount of restricted cash, the adjusted ratios may be lower than the unadjusted ones, suggesting a tighter liquidity position.

While liquidity ratios primarily assess short-term liquidity, it's essential to consider a company's overall financial health and long-term liquidity needs, especially if restricted cash represents a significant portion of total assets.

Special case of Compensating balance

A compensating balance is a minimum deposit a borrower must maintain in a bank account. The purpose of this balance is to reduce the lending cost for the lender since the lender can further give this money as a loan. Compensating balances are mostly reported on financial statements as restricted cash.

Small startups generally don't have a credit history and are forced to accept the compensating balance as a borrower.

It can be calculated in two ways:

- As an average balance arrangement common with installment loans

- A minimum fixed balance arrangement used with lines of credit.

The example of a rubber manufacturer company is a case of compensating balance where company X needs to maintain a minimum balance which is generally a percentage of the total loan.

or Want to Sign up with your social account?