Breakup Value

The value of the different components of a business if they were sold off or spun off from their parent company

What Is Breakup Value?

The breakup value of a corporation would be the value of the different components of the business if they were sold off or spun off from the parent company. It is calculated by taking the total assets of each business segment and deducting the total liabilities.

We could define it as the market value of a business if its various components were to be separated from its parent company and run independently.

The value of the subsidiaries/components is calculated on a relative valuation basis by taking the multiples of a comparable firm or on an absolute valuation basis using the free cash flows generated by the business segment.

If the calculated value exceeds the company's market value, then it would be beneficial to the parent company to separate this segment as it would increase shareholder value.

Investors use a company's breakup value to assess its financial health and determine the most valuable business segment, after which they evaluate when and how to invest in the company.

The proceeds from selling a business component get distributed to shareholders as stock dividends.

It is crucial to understand that dividing the segments of a firm can lead to the loss of any synergies from having the entire business run as part of the parent company.

- Breakup value represents the worth of individual components of a business if separated from the parent company, calculated by subtracting total liabilities from the total assets of each segment.

- Companies may break up due to reasons like bad management, liquidity problems, slow growth, or persistent undervaluation relative to breakup value.

- Investors use breakup value to evaluate the attractiveness of a company’s stock and determine entry or exit points in their investments.

- Calculation methods include relative valuation (comparing segments to competitors) and the discounted cash flow model, along with other approaches like market capitalization and time revenue analysis.

Causes of a Company Breakup

Companies often break up due to four key reasons: bad management, liquidity problems, slow growth rate, and shareholder value.

1. Bad management

A prominent reason for companies to break up is poor management. This is because poor management and failure to achieve the company's goals and objectives prompt the board of directors to split it from the parent company and sell its assets for cash.

Instead of selling its assets for cash, the company may also choose to sell the subsidiary to another company. In return, the parent company receives compensation in the form of cash or shares of stock in the acquiring company

2. Liquidity problems

When a subsidiary runs short of financing for operations or is not profitable, the parent company is responsible for helping the subsidiary until it gets back on its feet.

This is an opportunity cost for the parent company as it affects its operations and allocation of funds.

Instead of investing the money in revenue-generating activities, the company bails out the subsidiary, which may or may not benefit them.

Where the subsidiary cannot recover even after funding, the parent company can choose to sell the whole subsidiary to another business and regain the cash foregone because of the costs.

3. Slow Growth

A company that is experiencing a strong growth rate may sell off one of its slowest growing divisions to focus all the company's capital on its more successful segments.

Selling off the division will also provide additional funds to finance the rapid growth of the successful segments and allow the company to experience an even faster growth rate than its competitors.

4. Shareholder Value

Suppose a company has a market capitalization that is less than its breakup value for a prolonged period. In that case, major investors may press for the company to be split to maximize shareholder profits.

How the Breakup Value is Used

It mainly applies to large-cap stocks that operate in several distinct markets or diversified industries.

Investors may demand that a firm be split up if the value of the stock has not increased, with the proceeds going back to investors in the form of new shares in the spinoff companies.

Investors can calculate a completely healthy company's breakup value to estimate a potential floor for its stock price or a possible entry point for a potential stock buyer.

A couple of reasons include:

1. Assessing the financial strength

Investors can calculate the value to decide whether the company is worth having in its portfolio or not.

If they discover that the company's shares are trading at a discount to the breakup value, it means that the stock is undervalued and has potential for long-term growth.

As a result, they should keep onto their shares and perhaps purchase more unless other factors indicate a poor outlook or the company is overvalued, in which case it would be wise to sell.

If the subsidiary is performing poorly, the investors may call for the subsidiaries to be sold or spun off, allowing them to increase their shares' value.

2. Evaluating when to invest

Investors can calculate the value to determine the best entry point for their investment.

To determine the value of the firm and determine whether they are about to sell or spin off a specific area of their business to expand, they can then utilize the relative values approach or discounted cash flow method.

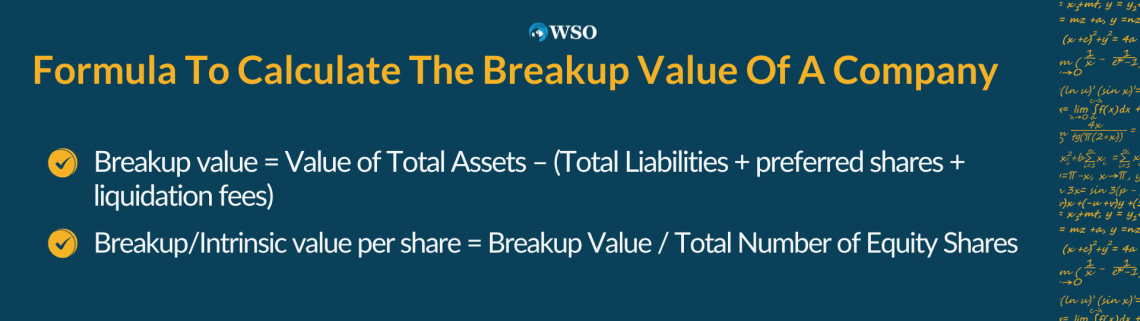

How to Calculate the Breakup Value of a Company

Formula to calculate:

Breakup value = Value of Total Assets – (Total Liabilities + preferred shares + liquidation fees)

Breakup/Intrinsic value per share = Breakup Value / Total Number of Equity Shares

Breakup valuation methods:

1. Relative valuation

Relative valuation looks into the value of various business segments comparable to their competitors within the industry. One looks into the multiple comparable companies to determine how business segments are performing relative to the industry.

The price-to-earnings ratio is the most common valuation multiple when calculating the value as a low P/E means that the company is trading under its actual price and therefore is considered undervalued and a good price to buy at.

Using multiples such as price-to-earnings (P/E), forward P/E, price-to-sales (P/S), price-to-book (P/B), and price-to-free cash flow, analysts evaluate how the business segment is performing compared to its peers.

2. Discounted Cash flow Model

This valuation method uses future expected cash flows to determine the value of an investment. The future cash flows are discounted to get the present value of the investment opportunity.

If the present value is higher than the current market value, it may point to an investment with a positive future outlook.

3. Other valuation methods

Some other business valuation methods include market capitalization, which is the share price multiplied by the total number of shares outstanding.

The time revenue approach is based on a stream of revenues produced over a period, to which an analyst applies a particular multiplier derived from the sector and overall economic climate.

Example of transactions and their breakup values

Companies and investors often conduct breakup value analyses to make investment and acquisition decisions. The higher the value, the more credible the number of assets of the company.

As an example, if Company A is sold to Company B, Company A shareholders may receive a certain cash and equity mix from Company B.

Stock transactions for Company B would work in the following way: the shareholders of company A would receive one share of stock in B for every ten shares they have of stock A.

An example of a potentially valuable separation is Amazon spinning off Amazon Web Services from the parent company.

AWS has seen immense growth and has been a stronghold for Amazon for the past few years, posting an operating margin of over 22% in the last 12 months versus low single digits at Amazon's online retailing arm.

In November 2019, Amazon's market capitalization was close to $1.9 trillion, though spinning off the AWS arm could increase its market capitalization by 50%, making it an exciting prospect.

Amazon also faces antitrust scrutiny from regulators in the U.S. and overseas pertaining to the size and monopolistic effect of its e-commerce space.

By breaking off AWS, Amazon could potentially appease regulators by making AWS more appealing to Amazon's retail competitors and allowing Amazon to expand its advertising business in both U.S. and overseas markets without the same antitrust issues.

Breakup Value FAQs

Private Market Value, Sum-of-the-Parts Value, Intrinsic Value, Net Assets Value, Net Worth per Share, Gone Concern Value, Liquidation Value.

A corporation's book value could be thought of as its break-up value or the sum that the business would be worth if it were liquidated.

The formula is:

Breakup value = Value of Total Assets – (Total Liabilities + preferred shares + liquidation fees)

Some reasons include bad management, liquidity problems for the parent company, slower growth rate from a subsidiary as compared to the business as a whole.

Scrap value is the value of a physical asset's components when the asset itself is no longer usable.

Long-term assets, such as machinery or vehicles, have gone through their useful life, they can be disposed of and sold at a lower price. The scrap value is the estimated cost that a fixed asset can be sold for after factoring in depreciation.

or Want to Sign up with your social account?