Diluted Shares Outstanding

The total amount of a firm's outstanding shares if all convertible financial assets were converted into common stock.

What are Fully Diluted Shares?

Diluted shares refer to the total amount of a firm's outstanding shares if all convertible financial assets were converted or changed into common stock.

These instruments encompass stock options, warrants, convertible bonds, and other financial tools that may be transformed into or swapped for common stock.

Diluted shares accurately represent a corporation's capital structure and potential effect on earnings per share (EPS) and other financial metrics.

In determining diluted EPS, analysts and investors substitute the basic count of outstanding shares with the number of diluted shares, as this accounts for potential dilution that might arise if all convertible instruments were converted or altered.

Consequently, the organization's fiscal performance and worth are assessed with increased prudence and practicality.

In essence, diluted shares consider the potential increase in outstanding shares due to converting or utilizing convertible securities, which can influence a company's earnings per share and other financial parameters.

- Fully diluted shares refer to the total number of outstanding shares of a company, including all potential shares that could be issued through the conversion of convertible securities, stock options, and other equity-related instruments.

- To determine fully diluted shares, add the number of existing outstanding shares to the shares that could be created from convertible securities, stock options, warrants, and any other convertible instruments.

- Calculating fully diluted shares provides a comprehensive view of a company’s potential equity structure, helping investors assess the impact of potential dilution on their ownership percentage and EPS.

- In mergers and acquisitions, fully diluted shares are used to determine the value of a company and to calculate the impact on share ownership and valuation in potential transactions.

Risks Associated With Diluted Shares

When an organization opts to release additional shares, it can lead to an occurrence referred to as dilution. This event often raises concerns among investors, as it could lower the worth of their existing shares and diminish their relative stake in the company.

Shareholders need to grasp the concept of dilution, its possible impact on their investments, and the rationale behind a company's choice to release new stock. Consequently, an in-depth exploration of the topic is crucial for making knowledgeable decisions.

Let's examine an example of dilution outcome: Many shareholders often perceive dilution unfavorably, as it reduces their ownership percentage in the corporation by bringing additional investors on board.

This can cause shareholders to experience a decrease in their significance and sway within the organization, which might be unsettling for some.

Additionally, there may be instances where investors with a large shareholding exploit those with a smaller stake in the company by leveraging their greater influence to push decisions that primarily benefit them.

Nonetheless, it's worth mentioning that issuing new stock is beneficial. On the contrary, under specific circumstances, it may prove advantageous to the corporation and its investors if the objective is to obtain financing for growth or a novel initiative.

For instance, a company might release new shares to amass funds to invest in groundbreaking products or technology, form strategic alliances, enter new markets, or acquire competitors.

During these situations, the benefits derived from the inflow of funds might offset the negative consequences of dilution, leading to an overall enhancement in the worth of shareholders' investments.

It is essential for investors to closely examine the reasons underlying a company's decision to release additional shares and assess if the expected gains from the introduction of fresh capital surpass the potential drawbacks of dilution.

These steps allow shareholders to make well-informed choices and safeguard their interests over time.

Signs of Dilution to be Cautious of

Individual investors need to be watchful for red flags that may hint at possible share dilution, as this can lessen the worth of their investment.

One such indication is when a corporation requires more funding to meet expenses but cannot assume additional debt due to existing agreements, resulting in a new share equity offering.

Expansion possibilities can also signal potential share dilution, as businesses might utilize secondary offerings to acquire investment capital for substantial projects or fresh ventures.

Furthermore, investors should exercise caution with companies that distribute considerable optionable securities to their staff, as these options usually have a vesting period attached.

Misjudging vested options can cause considerable dilution when employees decide to exercise their options. In addition, contracts of key personnel mandate the disclosure of their anticipated optionable holdings exercise.

Note

Diluted shares can influence EPS and additional financial indicators, potentially causing significant repercussions on a corporation's financial reports. If the diluted EPS is smaller than the basic EPS, it could suggest that the enterprise has a considerable quantity of convertible securities in circulation.

The Role of Convertible Securities in Share Dilution

Transformable monetary tools, which include various investment instruments like equity options, financial guarantees, and convertible debt securities, play a vital role in the share dilution process within organizations.

These unique investment instruments enable companies to effectively raise capital, attract and retain talented employees by offering incentives, and adaptively manage their financial structure.

Employee compensation packages frequently incorporate equity options, allowing personnel to purchase shares in the organization at a predetermined cost during a specified period.

On the other hand, financial guarantees function as extended-duration instruments that provide the possessor with the non-compulsory entitlement to purchase or dispose of a specific quantity of shares at a fixed rate.

As debt securities, convertible bonds enable bondholders to exchange their bonds for a predetermined quantity of shares, typically at a fixed conversion ratio.

Although transformable monetary tools offer numerous advantages for the entities issuing them and the investors, these instruments can also significantly influence the total count of existing shares if utilized or altered.

The exercising or conversion of convertible securities boosts the total number of shares in circulation, leading to the dilution of current shareholders' ownership stakes.

This dilution can subsequently affect the company's overall value, decreasing earnings per share and potentially influencing stock prices.

Let's consider the influence of diluted shares on stock value: Dilution could have an adverse effect on a company's stock price, especially if investors interpret it as a sign of financial vulnerability or inadequate management.

However, dilution could also positively influence the stock price if it contributes to increased revenue or expansion opportunities.

How to Calculate Diluted Shares

Computing rephrased shares can be complex and elaborate, requiring accounting for various financial instruments.

These include stock options, warrants, convertible bonds, and contemplating various situations that might emerge during the conversion or exercise of these securities.

Analysts and investors typically use two main techniques to determine rephrased shares:

- Treasury stock technique

- If-converted approach

Each has its own benefits and particular uses.

The treasury stock technique is a popular method for assessing the impact of stock options and warrants on the total number of diluted shares.

This method assumes that the company uses the proceeds generated from exercising these options and warrants to buy back its shares in the open market, effectively lowering the number of outstanding shares.

The treasury stock method involves the following steps:

- Ascertain the number of shares issued when stock options and warrants are exercised.

- Compute the proceeds resulting from the exercise of these securities, generally utilizing the exercise price of the options or warrants.

- Estimate the number of shares the company would repurchase using the proceeds calculated in step 2, considering the average market price of the stock during the relevant period.

- Calculate the net increase in outstanding shares by subtracting the repurchased (step 3) from the newly issued shares (step 1).

In contrast, the if-converted approach concentrates on convertible financial instruments such as bonds and preferred shares.

The if-converted technique presumes that all convertible securities transform into common stock at the commencement of the reporting period or upon issuance, depending on which occurs later.

To calculate diluted shares using the if-converted method, follow these steps:

- Step 1: Determine the number of shares that would be issued upon converting the convertible securities, utilizing the conversion proportion outlined in the conditions of the securities.

- Step 2: Add these newly issued shares to the number of outstanding shares at the start of the reporting period or when the securities were issued.

- Step 3: It is essential to acknowledge that, in certain instances, the treasury stock technique and the if-converted approach might be employed concurrently to compute rephrased shares, particularly when a corporation has issued various convertible financial instruments.

- Step 4: In these situations, the analyst or investor must meticulously evaluate the influence of each security on share dilution and merge the findings to thoroughly comprehend the possible dilutive impact on the enterprise's outstanding shares.

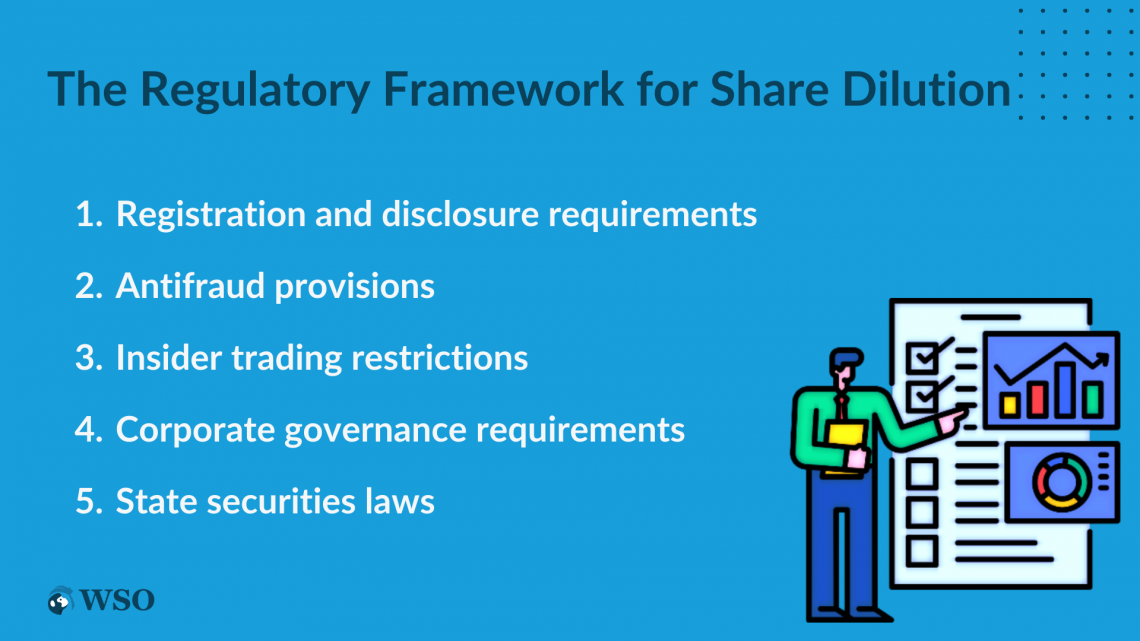

The Regulatory Framework for Diluted Shares

The legal framework around share dilution is critical to corporate governance, ensuring businesses adhere to the proper guidelines and rules when issuing new shares or convertible financial instruments.

Following these rules helps maintain clarity and fairness in financial markets, safeguarding the company's and its shareholders' interests.

In the United States, the Securities and Exchange Commission (SEC) is a primary regulator overseeing such concerns, necessitating that firms file registration statements for public security

offerings and reveal essential information about the terms, risks, and potential impact of the offering on existing shareholders.

Besides the SEC, other regulatory organizations and guidelines at federal and state levels dictate share dilution and the issuance of convertible securities. Key regulatory aspects connected to share dilution involve the following.

Registration and Disclosure Requirements

The SEC mandates that corporations register the release of new securities by submitting a registration statement for initial public offerings (IPOs) or Form S-3 for experienced issuers.

These statements require detailed data about the firm's financial condition, management, business functions, and the particular terms of the securities being issued.

This data is essential for enabling investors to make knowledgeable choices concerning the possible hazards and advantages of the offering.

Antifraud Provisions

Securities laws, such as the Securities Act of 1933 and the Securities Exchange Act of 1934, include antifraud provisions that disallow companies from making incorrect or deceptive statements concerning the issuance of securities.

Insider Trading Restrictions

Laws and regulations on insider trading prevent individuals with access to non-public, critical information from trading the company's securities.

This is especially relevant regarding share dilution, as insiders may possess information about upcoming convertible security offerings, which could significantly influence the stock price. Adhering to these regulations ensures equal chances for all investors.

Corporate Governance Requirements

Companies listed on stock exchanges, like the New York Stock Exchange (NYSE) or NASDAQ, need to comply with corporate governance standards set by these exchanges.

These standards entail requirements for board composition, shareholder approval for specific actions, and other measures designed to protect shareholder interests.

In the context of share dilution, these rules guarantee that companies act in the best interests of all shareholders when issuing convertible securities or undertaking actions that may lead to dilution.

State Securities Laws

Apart from following federal guidelines, businesses are also obliged to abide by state-level securities regulations.

These laws aim to safeguard investors by enforcing registration and disclosure of securities offerings within the state and by supervising the actions of brokers, dealers, and financial advisors.

Adhering to these state-specific rules is vital for companies to preserve their capacity to obtain financing and distribute securities across various jurisdictions.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?