Treasury Stock Method

A method to calculate the number of new shares that could be generated by unexercised in-the-money warrants and options

What Is The Treasury Stock Method?

The Treasury Stock Method is a way of calculating the diluted earnings per share (EPS) of a company when it has outstanding stock options, warrants, or other convertible securities. This method is used to understand the potential dilution effect on existing shareholders if all convertible securities were exercised.

Companies use the Treasury Stock Method (TSM) to calculate the number of new shares that could be generated by unexercised in-the-money warrants and options when the strike price is less than the current share price.

The TSM calculation would estimate the hypothetical effect if all in-the-money securities were exercised. Therefore, all in-the-money warrants and options that can be exercised are included in the share count computation.

To get to its diluted earnings per share (EPS), a company has to factor in the additional shares gained through the treasury stock method.

The TSM assumes that when a company receives proceeds from exercising an in-the-money option or warrant, it uses those gains to buy back common stocks.

The shares repurchased by the company are called treasury stock, hence the name of this method. Repurchasing shares aims to minimize the dilutive effect of in-the-money securities.

Outstanding in-the-money options and warrants dilute a company's EPS, as investors who own these securities can purchase common shares at a lower price than the current market price, thereby increasing the number of shares.

According to the Generally Accepted Accounting Principles (GAAP), companies must report details on their diluted EPS using the TSM.

Understanding The Treasury Stock Method

According to the TSM, the primary share count used in computing a company's basic EPS must increase due to the company's in-the-money options and warrants. These securities give holders the right to buy common shares cheaper than the current market price.

Companies must use the TSM to compute their diluted EPS to abide by GAAP rules.

A few assumptions of the TSM include:

- Companies exercise options and warrants at the beginning of each reporting period.

- Companies use the proceeds from these securities to buy back common shares (at the average market price) during that reporting period.

- To account for a company's dilutive securities, metrics are based on diluted shares outstanding rather than the primary share count and basic EPS.

- This fully diluted shares outstanding metric more accurately represents a company's actual equity ownership and equity value per share.

- Not including dilutive securities into common equity inaccurately inflates a company's EPS calculation.

Effect on Diluted EPS

Exercising in-the-money options and warrants is one of the most dilutive practices a company could undertake. To summarize, EPS is calculated by dividing net income by the weighted average outstanding shares.

With the TSM, net income has no impact because all proceeds are used to buy back treasury stock in the market. However, the number of shares outstanding is affected (it increases).

There is a guaranteed decrease in diluted EPS because there is no change in net income, but the denominator (shares outstanding) increases.

Treasury Stock Method Formula

The TSM formula is as follows:

Additional Shares Outstanding = [Gross “In-the-Money” Dilutive Securities] - [Repurchased Shares]

Additional shares outstanding = n - (n x K / P)

Additional shares outstanding = n x (1 - K / P)

Where:

- Repurchased Shares = option proceeds

- n = shares from exercised options and warrants

- K = average exercise share price (strike price)

- P = Average share price for the reporting period

The ultimate goal of the TSM is to calculate a company's diluted EPS, so an additional formula is required once we have the additional shares outstanding:

Diluted EPS = Net Income / [Basic Shares Outstanding + Additional Shares Outstanding]

Below are some different types of dilutive securities:

1. Options

Options are financial instruments that allow two parties to transact an asset before a set date at a specified price.

In other words, they are contracts that give owners the right (not an obligation) to buy or sell an underlying asset (like stocks). Usually, they are acquired by purchase, either as compensation or as a portion of a significant financial transaction.

Private parties trade options in over-the-counter transactions. They can also be exchange-traded in markets.

2. Warrants

Warrants are financial instruments similar to options, but new shares are issued if warrants are exercised.

3. Restricted stock units (RSUs)

These securities are issued to a company's management team with an attached convertible feature. The purpose of an RSU is to grant employees shares of a company as compensation.

Additionally, it is essential to be familiar with the different phrases used to describe options:

- "In-the-money" options: strike price < current market price

- "At-the-money" options: strike price = current market price

- "Out-of-the-money" options: strike price > current market price

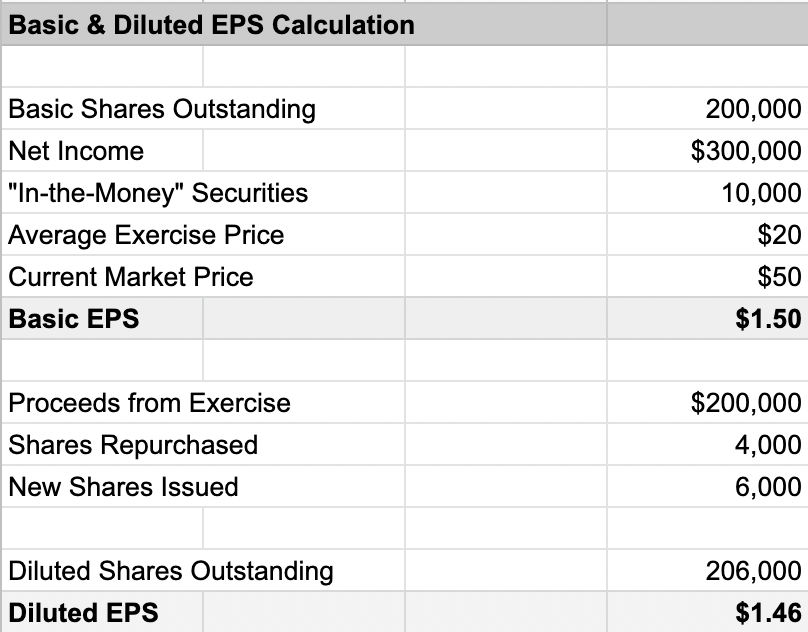

Treasury Stock Method Example

Company X has 200,000 common shares and $300,000 in net income in the last twelve months (LTM).

To calculate the basic EPS, which does not include the impact of dilutive securities, the EPS would be $1.50 ($300,000 net income / 200,000 shares).

Company X wants to account for their in-the-money securities that have not yet been exercised. To do this, Company X must multiply the potential shares issued by the average exercise price to calculate the total proceeds assuming the holder exercises them.

Given that Company X has 10,000 in-the-money options and the average exercise price is $20, this calculation would give Company X $200,000 (10,000 multiplied by the average exercise price of $20).

Next, Company X must divide its exercise proceeds of $200,000 by the current market share price of $50, which results in $4,000. This is the number of shares repurchased.

Then Company X will subtract the 4,000 repurchased shares from the 10,000 newly exercised securities to get 6,000 shares as the net dilution. Net dilution is the number of new shares of repurchasing).

Then dividing Company X's net income of $300,000 by the diluted share count of 206,000, we get approximately $1.46 for the diluted EPS. This is about $0.04 less than the basic EPS of $1.50.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?