The Twitter IPO moved into its final phase, with the announcement last week of the preliminary pricing estimates per share and details of the offering. The company surprised many investors by setting an offering price of $17 to $20 per share, at the low end of market expectations, and pairing it with a plan to sell 70 million shares. Having posted on my estimate of Twitter’s price when the IPO was first announced and following up with my estimate of value, when the company filed its prospectus (S-1) with Twitter, I thought it would make sense to both update my valuation, with the new information that has emerged since, and to try to make sense of the pricing game that Twitter and its bankers are playing.

Updated valuation

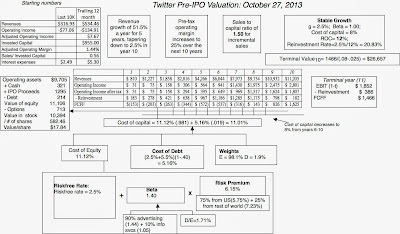

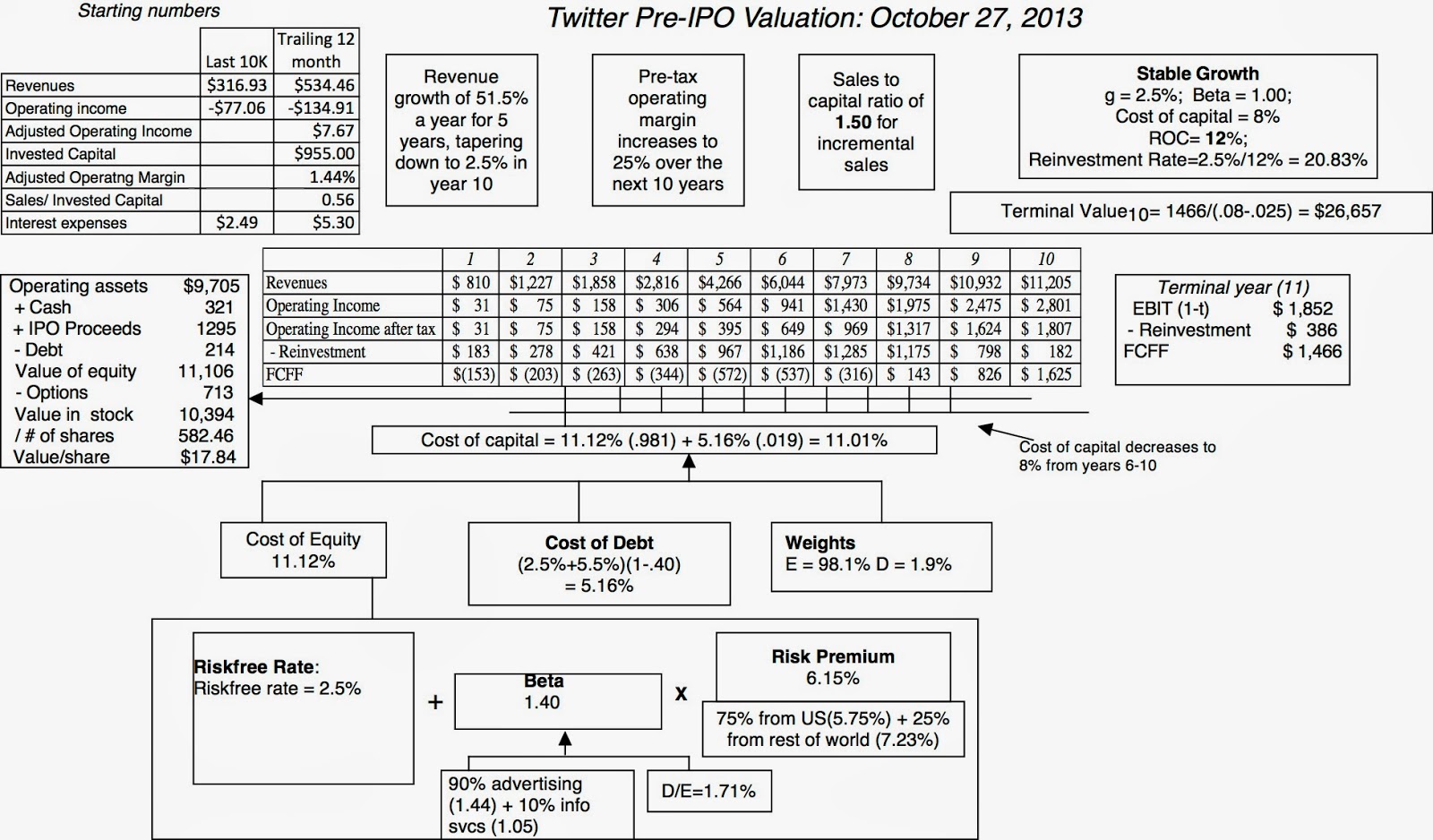

In my

original valuation of Twitter, just over a month ago, I used the Twitter's initial S-1 filing which contained information through the first two quarters of 2013 (ending June 30, 2013) and the rough details of what investors expected the

IPO proceeds to be. Since then, Twitter has released three amended filings with

the most recent one containing third quarter operating details and share numbers that reflect changes since June 30. Incorporating the information in this filing as well as the offering details contained in the report leads me to a (mostly minor) reassessment of my estimate of Twitter’s value.

Operating Results: Twitter’s third quarter report contained both good news and bad news. The good news was that revenue growth continued to accelerate, with revenues more than doubling relative to revenues in the same quarter in 2012, but it was accompanied by losses, which also surged. The table below compares the trailing 12-month values of key operating metrics from June 2013 (that I used in my prior valuation) with the updated values using the September 2013 reports:

As with prior periods, the R&D expense was a major reason for the reported losses and capitalizing that value does make the company very mildly profitable. Note that while the numbers have shifted significantly, there is little in the report that would lead me to reassess my narrative for the company: it remains a young company with significant growth potential in a competitive market. Consequently, my targeted revenues in 2023 ($11.2 billion) and the operating margin estimates (25%) for the company remain close to my initial estimates (October 5).

IPO proceeds: In the most recent filing, the company announced its intent to issue 70 million shares, with the option to increase that number by 10.5 million shares. In conjunction with the price range of $17-$20 that is also specified, that implies that the proceeds from the offering will range anywhere from $1.19 billion (70 million shares at $17/share) at the low end to $1.61 billion (80.5 million shares at $20/share) at the high end. In my valuation, I will assume that the offering will happen at the mid-range price ($18.50) and that the option to expand the offering will not be utilized, leading to an expected proceeds of $1.295 billion.

Share number: As with most young companies, the share number is a moving target as options get exercised and new shares are issued to employees and to fund acquisitions. In the table below, I compare the share numbers (actual, RSU and options) from the first S-1 filing with those in the most recent filing:

The share count has increased by about 8.02 million shares, since the last filing, while there has been a slight drop off in options outstanding. (Note: The most recent filing also references 80.3 million shares for future issuance to cover equity incentive & ESOP plans that I have not counted.)

The final valuation is contained

in this spreadsheet, but it has changed little from my original estimate, with the value per share increasing to $17.84/share from my original estimate of $17.36/share. The picture is below:

Reading the pricing tea leaves

Now that the company (and its bankers) have announced a price range ($17-$20) that is close to my estimate of value, my ego, of course, wants me to believe that this is a testimonial to my valuation skills but I know better. There is a fairy tale scenario, where my value is right,

Goldman Sachs has come up with a value very close to mine and the market price happens to reflect that value. It is a fantasy for a simple reason. As I noted in my price versus value post, the

IPO process has little to do with value and everything to do with price, and given how the market is pricing other social media companies, I find it difficult to believe that price and value have magically converged, with Twitter.

Accepting that the closeness of Goldman’s pricing of Twitter to my estimate of value is pure coincidence frees me to think about what it does tell me about the bankers' (and the company’s) view of what they see as a “fair price” for Twitter. If Goldman and the banking syndicate are pricing Twitter at $17-$20, I am inclined to believe that they think that the “fair price” today is higher for the following reasons:

- The underwriting skew: The Twitter IPO, like most public offerings, is backed by an underwriting guarantee from bankers that they will deliver the agreed upon offering price. If the offering price is set too high, relative to the fair price, that creates a substantial cost to the bankers, whereas if it is set too low, the cost is much smaller. Not surprisingly, IPOs tend to be underpriced, on average, by about 10-15% as I noted in this prior post.

- The PR twist: There is a public relations and marketing component to what happens on the offering date that cannot be under estimated. To provide a contrast, look at the reactions to the Facebook and Linkedin offerings in both the immediate aftermath of and in the weeks after the offering. While both IPOs were mispriced by the same lead banker (Morgan Stanley), with Facebook being over priced and Linkedin being under priced, Morgan Stanley was bashed for doing the former and emerged relatively unscathed from the latter. In the months after the offering, Facebook saw its shares lose more ground, as institutional investors abandoned it, while LinkedIn shares were carried higher, at least partly because of the opening day momentum.

- The feedback loop: I know that the bankers have been testing out the level of enthusiasm among investors for the Twitter offering and I find it difficult to believe that they are not incorporating that into their pricing. In other words, if they want excitement at the road show, it will come from investors thinking that they are getting a bargain and not from being offered a fair deal.

My completely uninformed guess is that the bankers think that Twitter’s fair price is closer to $25/share and that they have set the range at roughly 20% below those estimates. If the offering goes as choreographed, here is how it should unfold.

- The road show will be well received and the bankers will announce (reluctantly) that the high enthusiasm shown by investors has pushed them to set the offering price at $20/share.

- Institutional investors will start lining up for their preferred allotments at that offering price and the enthusiasm bubble will grow.

- On the offering date, the stock will jump about 20%-25%, leading to headlines the next day about the riches endowed on those who were lucky or privileged enough to get the shares in the offering.

- Some of the rest of us, who were not lucky or privileged enough to be part of the offering, will be drawn by these news stories into the stock, pushing the price higher, and keeping the momentum game going.

- In a few months or perhaps a year, some of the owners of Twitter (big investors and venture capitalists) will be able to sell their shares and cash out.

So, what can go wrong with this script? The biggest actor in this play is Mr. Market, a notoriously moody, unpredictable and perhaps bipolar (though that may require a clinical judgment) character. As was the case in Facebook, a last minute tantrum by Mr. Market can lay waste the best laid plans of banks and analysts.

Winners and Losers

Some of you may take issue with my cynical view of the

IPO process, arguing that this is not a play or a game and that there are real winners and losers in the process. While this is generally true for any investing process, who are the losers in this process? By under pricing

IPOs, the existing owners of the company going public are leaving money on the table. In the aftermath of the Linkedin offering, where

the offering price doubled on the opening day, there were stories that the company

had been scammed by bankers. Before you feel too sorry for Evan Williams and the venture capitalists, who are the primary owners of Twitter, you should take into account two facts:

- Only a small fraction of the equity is being offered to the public on the offering date: If all of Twitter being offered for sale on the offering date, an underpricing of 20% (selling the shares at $20, when the fair price is $25) would cost investors almost $3 billion in value (since the company would be priced at $12 billion instead of $15 billion). However, as noted earlier, only $1.2 to $1.6 billion will be offered to investors in the IPP. Even if you take the upper end of this amount ($1.6 billion), a 20% under pricing would translate into a loss of $400 million to the owners. While that may be a lot of money to most of us, it would work out to about 3% of overall value for the existing owners.

- The existing investors in Twitter are neither babes in the wood nor naïve fools: The current owners in Twitter are a who's who of venture capital investing, entirely capable of watching out for their own interests and just as likely to use bankers as they are to be used by them. Rather than being victims here of the under pricing, they are willing accomplices in this pricing process, who view the loss on the opening day as a small cost to pay for a more lucrative later exit.

There are some winners, though none of them emerge unscathed from the process. The first are the

bankers, who by under pricing the offering enough, render the underwriting guarantee moot and get paid for it anyway. Here again, though, issuers are not entirely helpless and Twitter

managed to get a discount on the underwriting fees. The second are those

investors who are allotted shares at the offering price, many of whom are preferred clientele for the banks. They generally tend to be wealthier investors (institutions and individuals) who bring in revenues in other ways to the banks (as

private banking clients or

through trading). Since banks are not altruistic, I am not sure that these preferred clients end up with a bargain if you count the other fees they fork out to banks. The third is the

financial media (and that includes bloggers) that can use the

IPO as grist for the mill, churning out endless stories (and blog posts) about the

IPO.

Cut out the bankers?

If you buy into my cynical view of the Twitter

IPO, it does make the whole process seem like a charade and raises questions about whether it is needed. What if we could skip the bankers, the offering price, the road shows and the endless debate about what will happen on the offering date and just go directly to the offering? It is true that bankers play other roles in the process that may be difficult to replace in some

IPOs, but I am not sure that can be said about their role in Twitter.

Hello Mr Damodaran,

First of all thank you very much for sharing with us the different steps of your valuation methodology.

Do you have any opinion about the business model of Twitter or of its closest competitors for that matter? I have started a post about that subject. I can't post the link here but the title of it is "Bird is the word"

Since your name and valuation poped up in the conversation, maybe you would like to share with us your opinion.

Thanks a lot.

Eum eos ea voluptate aut. Officia ex dolorem magni molestiae dolores qui ut. Pariatur quia consequatur accusamus. Soluta error veniam harum aut. Esse vero aut fugiat et fugiat. Molestias fugiat reiciendis dignissimos alias architecto.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...