Case Study: The Structural Pivot from "Activist" to "Quality" at Pershing Square

For those who remember the aggressive, headline-dominating Bill Ackman of the Herbalife or Valeant era, the current iteration of Pershing Square Capital Management feels like a completely different fund. The "wolf" has effectively become a sheepdog.

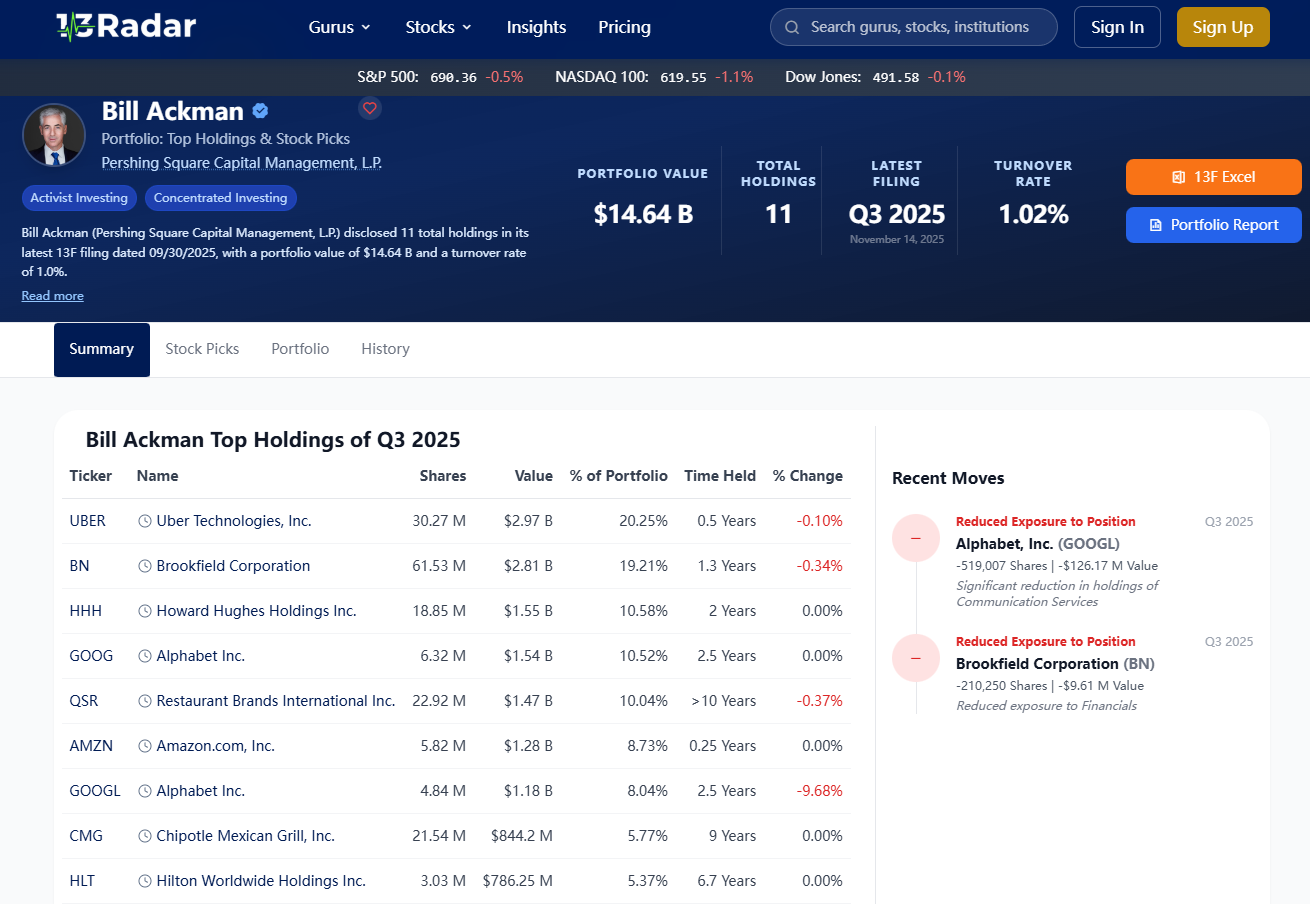

Analyzing the firm's recent capital allocation in Q3 2025 offers an interesting look into how a modern macro-aware fund is positioning itself late in the cycle. We are no longer seeing complex financial engineering or hostile proxy battles. Instead, we are seeing a portfolio that looks increasingly like a levered version of Berkshire Hathaway.

1. The Death of "Financial Engineering"?

In the past, Ackman’s alpha often came from forcing management changes or balance sheet restructuring. Today, the alpha seems to be derived purely from business selection rather than operational intervention.

The portfolio is heavily skewed towards high-FCF (Free Cash Flow) franchises—companies that possess pricing power independent of the Fed's dot plot. This shift suggests a broader realization among L/S equity managers: in a high-rate volatility regime, "turnaround stories" are too expensive to finance. The safest place to be is in businesses that don't need external capital to grow.

🔎 Analyst Note: The "Zero-Capex" Growth Model

A recurring theme in the portfolio is the "franchise model" (Hotels, QSRs). The appeal here for an institutional allocator is the separation of revenue from capital expenditure.

- Inflation Hedge: Royalties are based on top-line revenue, capturing price increases immediately.

- Margin Expansion: As franchisees scale, the parent company's margins expand non-linearly.

2. Portfolio Construction: Concentration as a Risk Factor

From a risk management perspective, Pershing Square remains an outlier. While the standard deviation of a 50-stock portfolio is generally accepted as "safe," Ackman continues to run with fewer than 10 core positions.

A review of the underlying data in the pershing square q3 2025 13f holdings indicates that the fund is comfortable tolerating significant idiosyncratic risk. This is a stark contrast to the "closet indexing" seen in many multi-manager pods today.

For junior analysts, this structure raises a valid debate: Is this true conviction, or simply a lack of scalable ideas? When a fund manages billions but refuses to diversify, it implies that the manager believes the marginal utility of the "11th best idea" is practically zero compared to adding to the top 3.

3. Tech Exposure: Utility vs. Speculation

It is worth noting the fund's approach to Technology. Unlike the Momentum/Growth funds that chased AI hardware, Pershing Square's exposure remains rooted in what can be best described as "Digital Utilities."

The thesis appears to treat large-cap tech not as innovation plays, but as essential infrastructure. Just as railroads were the monopoly plays of the 20th century, certain tech platforms are viewed as the unavoidable toll roads of the 21st. This aligns with the "Quality" factor—buying growth at a reasonable price (GARP) rather than paying peak multiples for future promises.

Whether this defensive positioning will outperform in a risk-on rally remains the open question for the next fiscal year.

Ad aut nulla autem velit non commodi rerum. Adipisci architecto dolorem consequuntur ipsum distinctio quaerat. Laudantium sint animi rerum. Aut cumque dolor est voluptatibus esse.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...