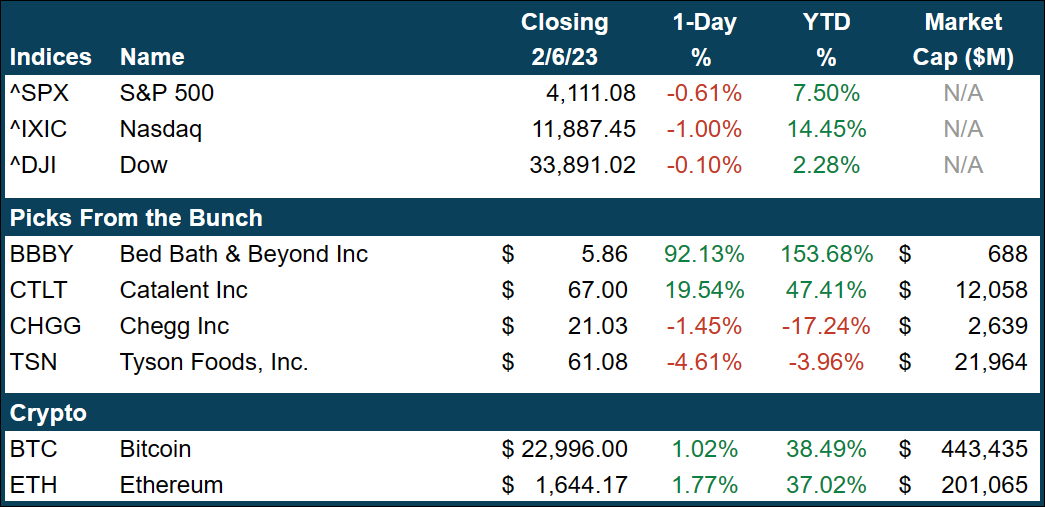

|

How’s Your Housing?

Here’s a nice “Would You Rather” to use with your friends: Would you rather be stranded alone on a desert island with absolutely nothing for the rest of your life, or would you rather be a first-time homebuyer in the United States in 2023?

It’s a tough one, I know, and the thing is those two scenarios aren’t that different from each other. The only difference is that in the first scenario, at least you don’t have your parents, kids, friends, or all of the above pressuring you to fix your situation.

Buying a home in the US right now is right around the least amount of fun that it’s ever been. In 2021, housing and housing-related activities accounted for ~16.7% of the US GDP, meaning right around $1 out of every $6 spent in the US that year was related to our homes. Spoiler alert: that will almost definitely not be the case in 2023.

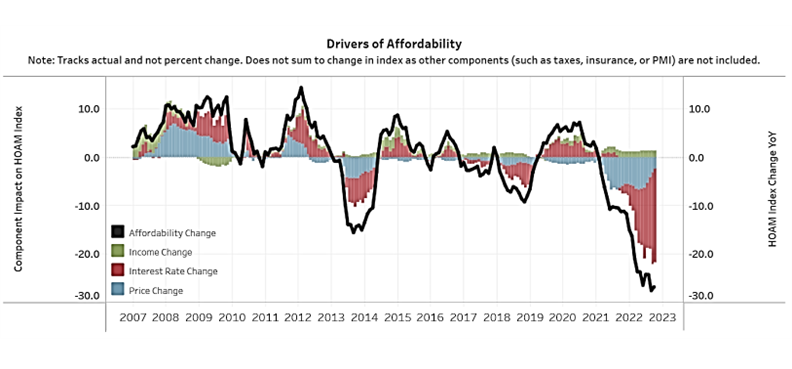

Take a quick peek at today’s Data Peel. See what I mean? Maybe not, as it took me a solid 20 minutes of research to learn WTF that chart was even trying to say. Apparently, the black line going down means the affordability of housing is falling. And as you can see, it’s doing a whole lot more than just falling lately.

That other sh*t you see on the chart essentially summarizes the biggest factors impacting home affordability: price, rates, and income. While income has gained significantly during the pandemic, particularly on the lower levels, it has not been able to keep up with the explosion (implosions?) in one’s ability to buy a home.

It all started when home prices soared 40% in little more than 2 years following C-19 washing up on our shores. This brought rates back down to zero while the velocity of home sales skyrocketed as everyone, everywhere, moved somewhere better to WFH. Naturally, falling rates and sky-high demand led to an explosion in prices.

Now, rates have mooned like $GME in early 2021 while income growth is slowing alongside demand to move into a new home. What does this mean? Well, we’re glad you asked.

This means that the housing market is following in the footsteps of a hyper-popular Disney movie and becoming Frozen. Although falling, recent changes in home prices haven’t fallen nearly enough to meet the demand of the next marginal buyer for the most part. This is largely due to the following:

- Less supply as builders have slowed home building and permitting in both long- and short-term trends

- Mortgage handcuffs, as no one wants to trade a 3% rate for a 6.5% rate

- Recession worries don’t exactly inspire shoveling an a**load of debt onto your plate in the form of a new mortgage (especially at 6.5%)

American home builders effectively have PTSD from 2008. They’re terrified of building to meet outsize demand, as the last time that happened, well, let’s just say Michael Burry made a lot of money (and a movie).

Moreover, many homeowners didn’t mind selling and taking on a new mortgage in recent years because they could do so at roughly the same mortgage rate as their existing place. Now, with average 30-year fixed rates sitting around 6.46%, it’s not exactly easy to convince someone who bought during ZIRP or C-19 to relinquish their 2.5% rate for something almost 3x that.

Usually, the concern is the marginal buyer. As the chart below and info above suggest, right now, there isn’t even a marginal seller, let alone someone to buy the thing. Buyers don’t wanna pay absurd prices, sellers don’t wanna take a loss on their goddamn house, and JPow wants us all to suffer the pain of high rates. Place your bets now!

|

Sit atque ipsa autem autem debitis commodi. In consectetur ullam et maiores similique omnis. Totam sint quod tenetur necessitatibus. Maxime id facere laudantium suscipit laudantium dolorem a.

Alias animi quam praesentium rerum autem eaque et. Magni cum quas ad expedita. In laboriosam illum et porro omnis nihil quaerat. Ipsum magni necessitatibus nostrum cum et tenetur voluptas ratione. Ipsum nihil aut et rerum dolores amet minima cumque. Temporibus dolor harum eaque est.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...