Sector Rotation Analysis: Deep Dive into the DJCO Thesis

The narrative of Q1 2026 is increasingly defined by capital rotation—flows moving from high-beta technology names into value-weighted financials. For institutional allocators, this raises a question of durability: is this a temporary defensive move or a structural repricing of risk assets? Looking at the legacy holdings of the Daily Journal Corporation (DJCO), the portfolio offers a relevant case study on banking concentration in a "higher-for-longer" rate environment.

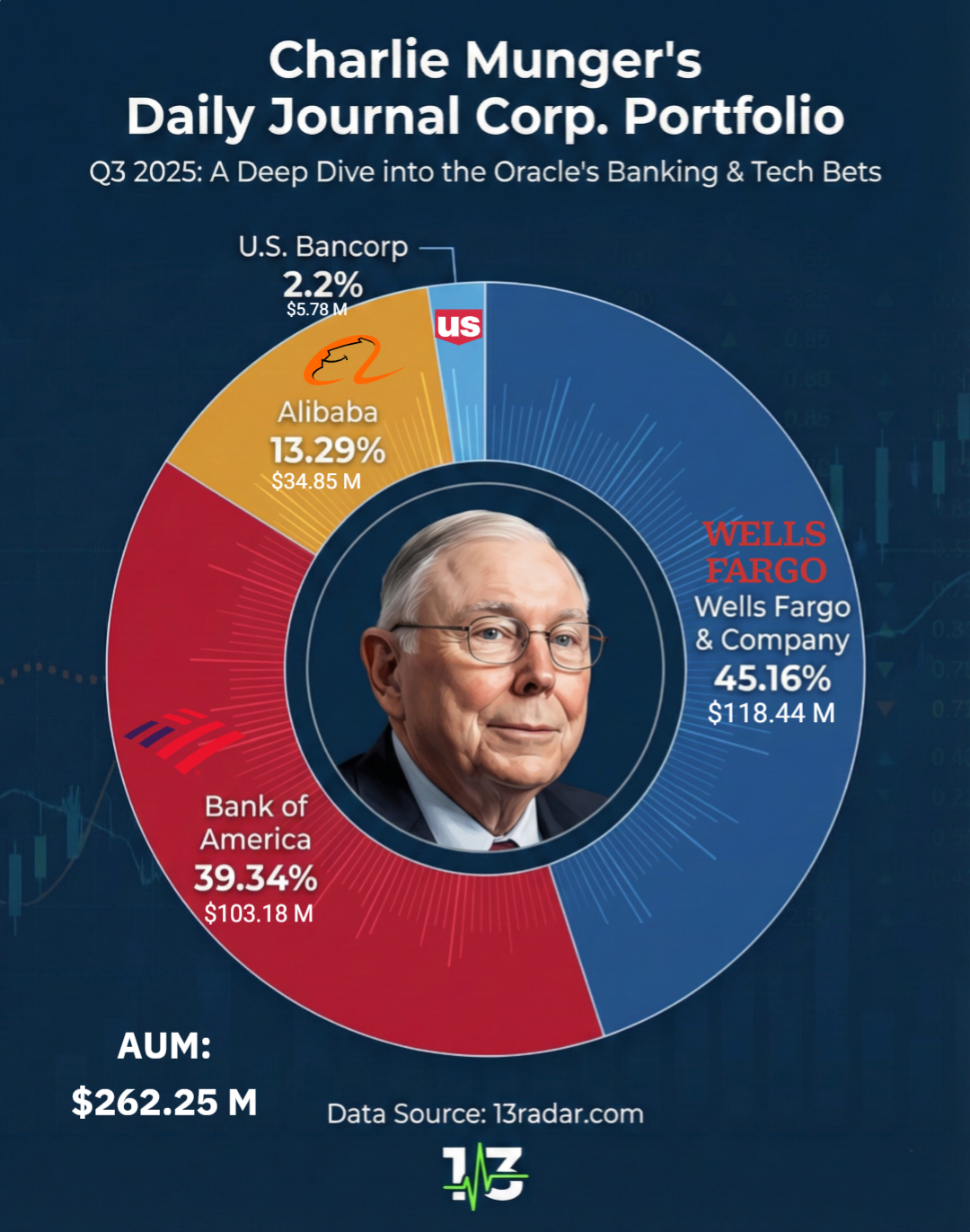

Unlike the diversified approach of typical index funds, the DJCO book remains an anomaly. It is heavily skewed towards US financials and Alibaba, representing a levered bet on systemic banking utility and Chinese e-commerce valuation compression. The thesis appears to rest not on growth projections, but on the disparity between price and tangible book value.

NIM Compression vs. Stabilization

The primary debate on Wall Street regarding bank stocks (specifically the "Big Four") centers on Net Interest Margins (NIM). Following the volatility of the past two years, the thesis for holding names like Wells Fargo (WFC) and Bank of America (BAC) relies on the normalization of the yield curve.

The DJCO allocation suggests a conviction that large-cap US banks have transitioned from "value traps" to capital return vehicles. With buybacks accelerating and balance sheets passing stress tests, the risk-reward profile of these equities offers a hedge against the multiple compression currently threatening the Nasdaq 100. It is effectively a short position on volatility.

Comparative Valuation: Tech vs. Financials

From a fundamental perspective, the divergence in valuation metrics between the top-heavy tech indices and the banking sector is reaching historical extremes. The following breakdown illustrates the implied expectations priced into both sectors (2026 Est.):

- Forward P/E

S&P 500 Tech Sector: > 25x (Priced for Perfection)

Major Money Center Banks: 8x - 10x (Priced for Stagnation) - Yield (Div + Buyback)

S&P 500 Tech Sector: ~1.5%

Major Money Center Banks: ~4.0% - 6.0% - Downside Buffer

S&P 500 Tech Sector: Minimal (High Multiple Contraction Risk)

Major Money Center Banks: High (Supported by Tangible Book Value)

This data highlights why the rotation is occurring. Allocators are moving down the risk curve. The banks do not need to innovate to justify their valuation; they simply need to remain solvent and return capital.

The "Inversion" Principle in Practice

The late Charlie Munger often referenced Jacobi's mathematical instruction: "Invert, always invert." Applied to the current market, this suggests avoiding the sectors with the highest probability of catastrophic multiple collapse.

Current 13F data regarding the charlie munger portfolio shows no capitulation on these positions, indicating that the original thesis remains intact despite external market noise. For analysts modeling these sectors, the key variable remains credit quality. If the US economy avoids a hard landing, the loan loss provisions taken by these banks may be released back into earnings, acting as a catalyst for a re-rating event.

The focus remains on whether the market is underestimating the earnings power of deposit franchises in a stabilized rate environment, relative to the speculative premiums currently assigned to AI infrastructure.

Iure cupiditate odio tempore deleniti dolorem. Impedit dolores labore non sint. Necessitatibus non et quibusdam at fugit delectus praesentium. Recusandae laudantium omnis nulla tenetur a non harum sunt. Non quasi voluptatem voluptatem praesentium unde aperiam blanditiis. Autem sit omnis commodi recusandae qui eius. Dolor nostrum porro deserunt.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...