The Burry Paradox: Why 13F Tracking Fails for High-Velocity Macro Strategies

There is a fundamental misunderstanding in the retail market regarding how to interpret Scion Asset Management's filings. While the media treats Michael Burry’s 13Fs as actionable "buy signals," those of us on the buy-side understand the structural limitations of these disclosures. Burry is not a long-term compounder like the Berkshire model; he operates a high-velocity, macro-tactical strategy. In the current environment (Jan 2026), analyzing Scion’s activity offers a fascinating case study in liquidity management and regime identification, rather than a simple stock-picking list.

The core issue is the Duration Mismatch. Burry often enters positions to exploit short-term dislocations—technical oversold conditions or specific catalyst plays—and exits once the mean reversion occurs. By the time the public sees the filing, the "alpha" has often already been extracted. The 13F, in this specific case, is not a map of where he is going, but a forensic record of where volatility was mispriced.

The "Rent vs. Own" Execution Style

Unlike many long-only funds that are forced to be closet indexers, Scion’s turnover rate is exceptionally high. This suggests a strategy focused on gamma trading and convexity rather than fundamental business ownership. Recent portfolio adjustments indicate a distinct move to monetize volatility.

For analysts modeling his performance, the challenge is separating the "core thesis" positions (which he holds for quarters) from the "tactical hedges" (which may be closed in weeks). The recent rotation out of consumer discretionary beta and into defensive real assets suggests a macro view that stagflation is the dominant risk premium moving forward.

⚡ THE LAG ARBITRAGE PROBLEM

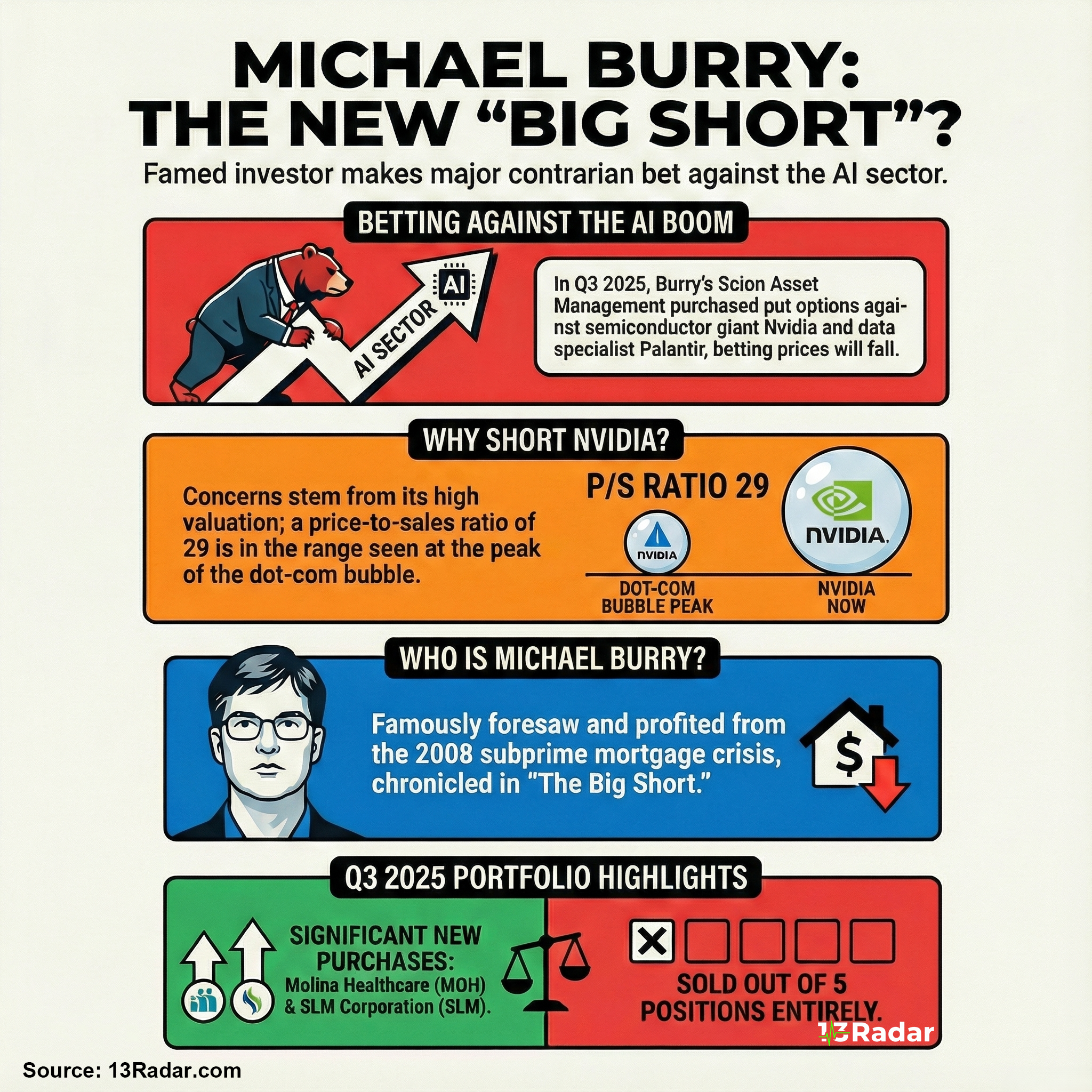

The 45-day reporting delay is the killer for copycat strategies. When we examine the scion asset management 13f filing date q3 2025, we are essentially looking at a "lagged indicator." Historical analysis of his filing cadence shows that Burry frequently uses the liquidity of earnings season to exit positions before the filing even hits EDGAR. For professionals, the value here isn't the ticker symbols, but the sectoral flows—identifying which industries a sharp contrarian mind believes are overcrowded.

Derivatives and the "Invisible" Portfolio

Another layer of complexity often overlooked is the notional value of option overlays. Burry’s extensive use of puts (often on semi-conductors or broad indices) acts as a portfolio dampener. In a professional context, these shouldn't necessarily be viewed as outright "shorts" in isolation, but as cost-effective insurance that allows the fund to run higher gross exposure in its long book (e.g., Chinese tech or deep value energy) without exceeding risk limits (VaR).

Conclusion: Alpha is in the Structure, Not the Ticker

For the WSO community, the takeaway from Scion's latest activity is about regime change. The aggressive rotation suggests that the "easy money" era of passive multiple expansion is over. Burry is positioning for a market where returns are generated by trading dispersion and volatility, not by holding beta. It serves as a reminder that in 2026, agility and the willingness to cut risk rapidly are becoming the primary differentiators for active managers.

Based on the most insightful WSO content, here's the breakdown of why tracking Michael Burry's 13F filings is a flawed strategy for retail investors, especially given his high-velocity macro-tactical approach:

1. Duration Mismatch: The Alpha is Already Gone

2. "Rent vs. Own" Execution Style

3. Sectoral Flows Over Tickers

4. Derivatives and the "Invisible" Portfolio

5. Key Takeaway for 2026: Agility Over Beta

Conclusion

For the WSO community, the lesson is clear: don't copy Burry's trades; study his strategy. His filings are a forensic record of where volatility was mispriced, not a roadmap for future gains. Instead, focus on understanding the macro themes and sectoral flows he identifies, as these insights can guide your own investment strategies in a market increasingly driven by dispersion and volatility.

Sources: Long term, concentrated, deep fundamental investing, Idea Generation... and Why Wall Street Sucks at It, Michael Burry sounds warning bell on ETFs

Molestiae occaecati enim rem voluptatibus quasi. Repudiandae dolore doloremque aspernatur iure pariatur et officiis.

Natus impedit explicabo quibusdam. Commodi eum maiores perferendis minima. Ut pariatur architecto rerum earum qui. Qui repudiandae quaerat repellat dolorum.

Qui maxime corrupti rerum voluptatem aut. Maiores minima dicta odit earum distinctio earum magni molestias. Alias mollitia qui consequatur numquam assumenda voluptatibus saepe consequatur. Repellat cupiditate consequuntur natus nobis aut totam dolorem vitae.

Animi non nesciunt ipsam accusantium dolores. Omnis qui doloremque odio quo ut porro. Qui impedit similique rerum vel modi odio et. Laudantium harum nihil incidunt dolorum omnis pariatur aut. Voluptatem et totam dolores mollitia libero omnis ea.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...