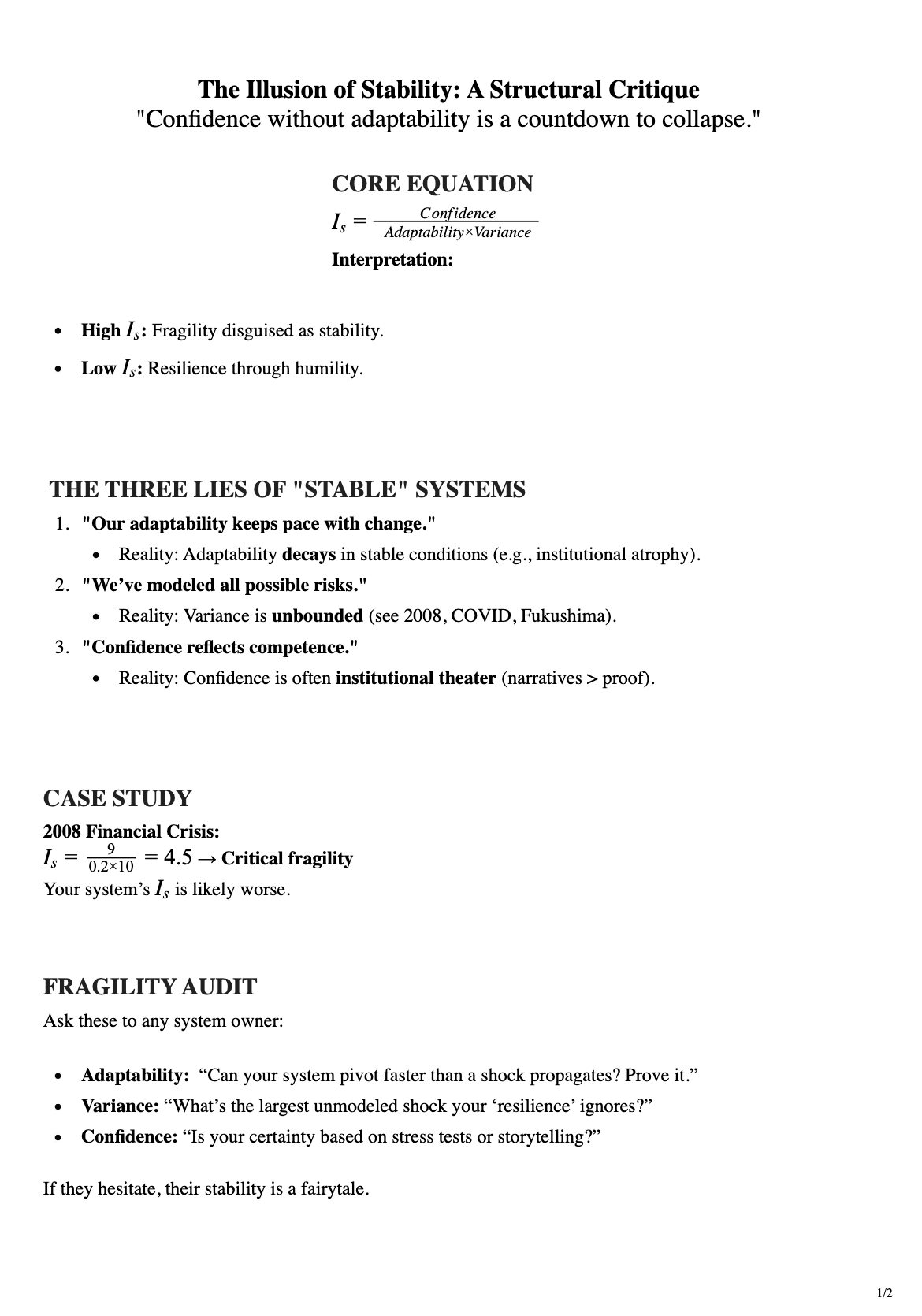

When Confidence ÷ (Adaptability × Variance) > 1, collapse is inevitable.

When Confidence ÷ (Adaptability × Variance) > 1, collapse is inevitable.

Modern systems—financial institutions, tech platforms, and even decentralized protocols—often mistake confidence for stability, leading to catastrophic failures when reality deviates from their narrow models. The Fragility Equation (Is=ConfidenceAdaptability×VarianceIs=Adaptability×VarianceConfidence) exposes this delusion by quantifying how quickly rigid structures collapse under stress. A high IsIs score (e.g., 4.5 for pre-2008 banks) reveals dangerous overconfidence: systems with low adaptability and unaccounted variance inevitably fail when shocks exceed their insulated assumptions. This pattern repeats in tech ("five nines" uptime shattered by correlated failures), pandemic preparedness (slow adaptation to exponential threats), and crypto (protocols crumbling under unmodeled governance attacks). True resilience requires humility over hubris—reducing IsIs by prioritizing dynamic adaptation and stress-testing against unbounded variance. Until leaders confront this math, their "stability" is just a countdown to collapse.

Key Takeaways:

- Confidence ≠ Stability – High confidence with low adaptability guarantees fragility.

- Variance is the Test – If a system hasn’t modeled extreme shocks, it’s already vulnerable.

- Survival = Is<1Is<1 – Adaptability must outpace both confidence and uncertainty.

Example:

- 2008 Banks: Is=4.5Is=4.5 → Collapse (slow adaptation, unmodeled mortgage risk).

- Robust Systems: Keep Is<1Is<1 via continuous stress tests and rapid pivots.

Question for Any System:

"When was your last proven adaptation to a crisis faster than the crisis itself?" (If the answer is unclear, IsIs is likely lethal.)

Nihil iste quod animi labore magni. Aut aut tenetur libero. Voluptas voluptatibus dolorum vel soluta aspernatur qui quo id.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...