This PE case study sample is brought to you by Value Add, the leading research journal for the operating side of private equity. Join thousands of buyside professionals who subscribe to Value Add for weekly news and insights about private equity buyouts, turnarounds, and exits.

Private Equity Case Study: Dell Technologies

Introduction

In the early 2010s, Dell Technologies, once a leader in the personal computing industry, was facing numerous challenges. The company was struggling with declining PC sales, intense competition from rivals like Lenovo, Samsung, and Apple, and a rapidly changing technology landscape favoring mobile devices and cloud computing. Dell's stock price was underperforming, reflecting its stagnating growth and poor market positioning.

In 2013, Silver Lake partnered with Michael Dell, the company's founder, to take Dell Technologies private in a $24.9 billion deal. It was one of the largest leveraged buyouts since the financial crisis and marked the beginning of a significant transformation for Dell Technologies. Michael Dell invested $4.2 billion in the deal, while Silver Lake invested $1.4 billion, and the rest of the transaction was financed by debt and cash from Dell Technologies.

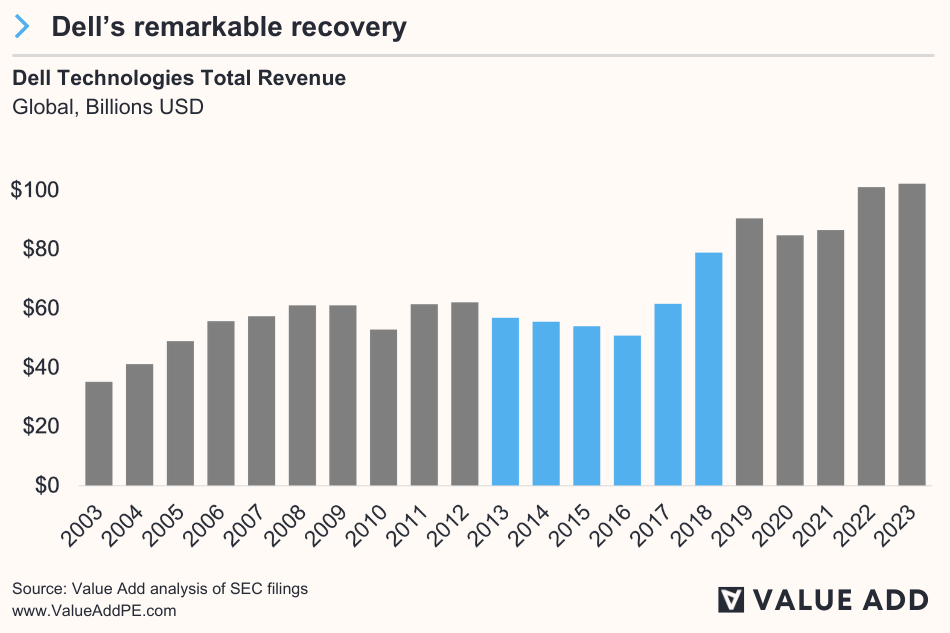

Silver Lake, one of the more technology-focused private equity firms, saw an opportunity to work with Dell’s namesake founder and turnaround the company from being a declining PC-maker to a fast-growing IT solutions provider. The value creation plan ultimately proved fruitful, as Silver Lake and Michael Dell earned an estimated $70 billion from the deal by 2023, making it one of the most-successful private equity turnarounds of all-time.

Pre-Buyout

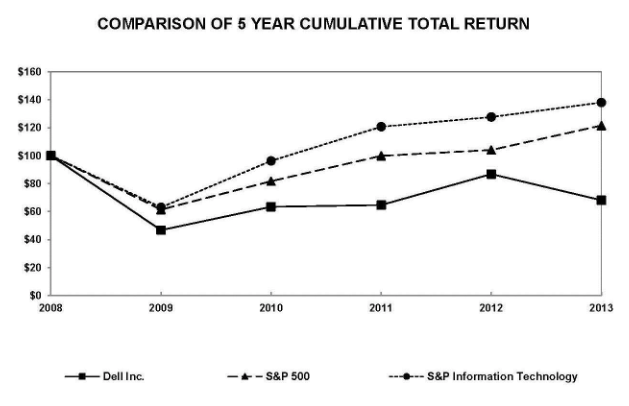

In 2013, the global financial crisis was firmly behind market participants, but Dell Technologies’ stock continued to struggle. $100 invested in Dell’s stock in 2008 would have been worth just $68 in 2013; for comparison, $100 invested in the broader S&P Information Technology index in 2008 would have been worth $138 by 2013. It showed how Dell, once a pioneer of the technology industry, was underperforming relative to its peers.

Dell's stock price underperformed competitors in the years leading up to being taken private by Michael Dell and Silver Lake.

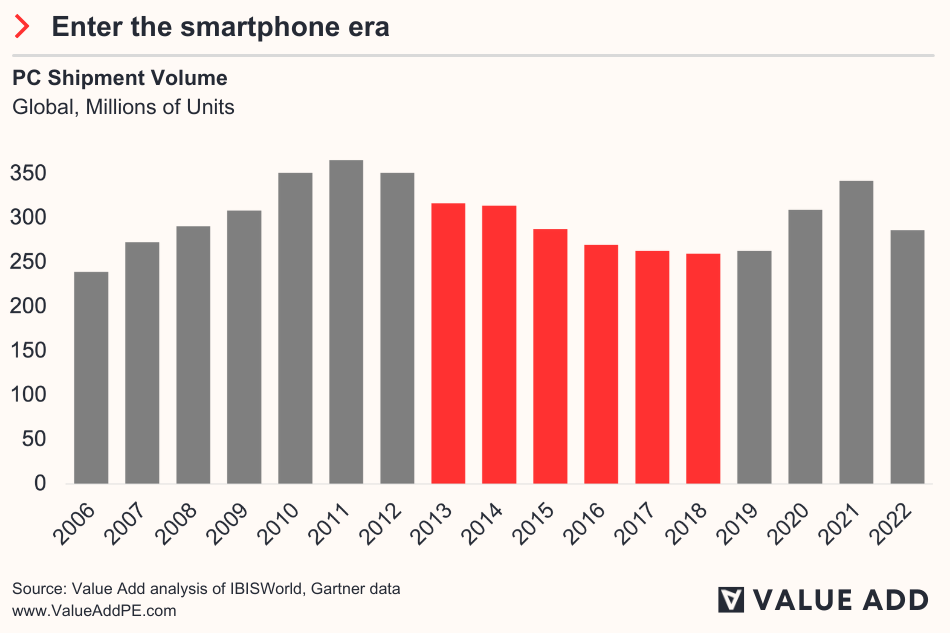

The problem for Dell was that the PC market, its main source of revenue, was falling-out from under the company. “PC sales slump enters sixth quarter with no end in sight. Research firms Gartner and IDC offer gloomy prognostication as consumers stay away,” wrote The Guardian in an October 2013 article. Mobile devices, such as the iPhone, iPad, and Samsung Galaxy, had started to cannibalize the PC market. In fairness to Dell, the company did launch a smartphone in 2010, but much like Microsoft’s early attempts at mobile devices, it failed to gain traction.

It was a horrible turn of events for Dell Technologies. The company was overexposed to the PC market and had little diversification in its business model. In 2013, 77% of Dell’s total revenue came from “product” sales, which included PCs and other devices, and total revenue declined by -8% in just one year.

Michael Dell knew as far back as the early-2000s that the company had to transform itself if it wanted to survive in a post-PC era. “We’re doing a lot of reinventing of the business model and the strategies of the company,” he said in a rare interview in 2010. “Here’s the way I think about it. The IT industry, depending on how you define it, is somewhere in the vicinity of $1.8 trillion. It’s a pretty big industry. Within that are all sorts of opportunities to provide products and services, and all of that goes into what we call the modern world today in terms of how businesses operate and are productive.”

With a radical transformation in mind, Michael Dell partnered with Silver Lake to take the company private. As we’ll learn later, Michael Dell and his chief lieutenants felt that they could operate much more effectively as a private company. “We can go faster on the transformation journey in a private setting,” said Dell’s former-CFO Tom Sweet.

Buyout and Value Creation Plan

In late-2013, Dell Technologies announced that it would be taken private by Michael Dell and Silver Lake for $24.9 billion. The company’s namesake founder would invest $4.2 billion for a 75% stake and Silver Lake would invest $1.4 billion for a 25% stake. The remainder of the deal was financed by Dell Technologies’ own debt and cash, a move that angered many of the company’s existing shareholders.

“This feels like the ultimate insider trade,” remarked Frederick Rowe, a general partner of Greenbrier Partners, at the time of the deal. Carl Icahn said the deal undervalued the company and likened Michael Dell to a “corporate dictator.” Forbes called it the “nastiest tech buyout ever.”

But Michael Dell and Silver Lake survived the criticism and were able to get to work on turning around Dell as a private company. Silver Lake co-CEO Egon Durban, who helped architect the turnaround of Skype between 2009-2011, joined Dell’s Board. The first order of business was solidifying the company’s value creation plan which focused on four key areas:

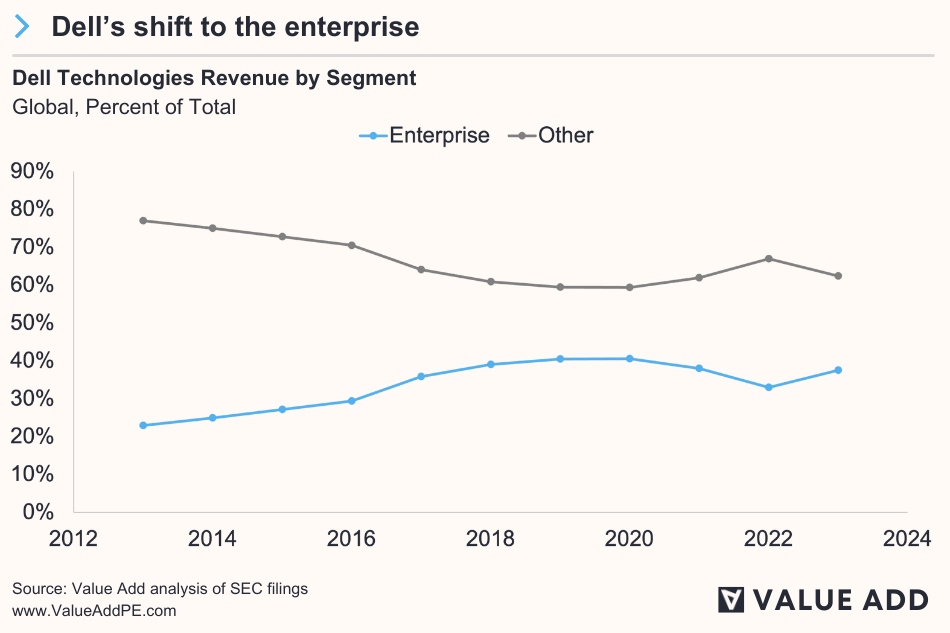

- Strategic Restructuring and Focus on Higher Margin Businesses. One of the key strategies Michael Dell and Silver Lake employed was the restructuring of Dell's business model. Under its private ownership, Dell shifted from being predominantly a PC manufacturer to focusing on higher-margin segments such as enterprise solutions, software, and services. This pivot was essential in repositioning Dell in the rapidly evolving tech landscape, where traditional hardware was becoming less profitable due to intense competition and thinning margins. By concentrating on areas like data storage, network security, and cloud computing, Dell could offer integrated solutions, enhancing its value proposition to enterprise customers.

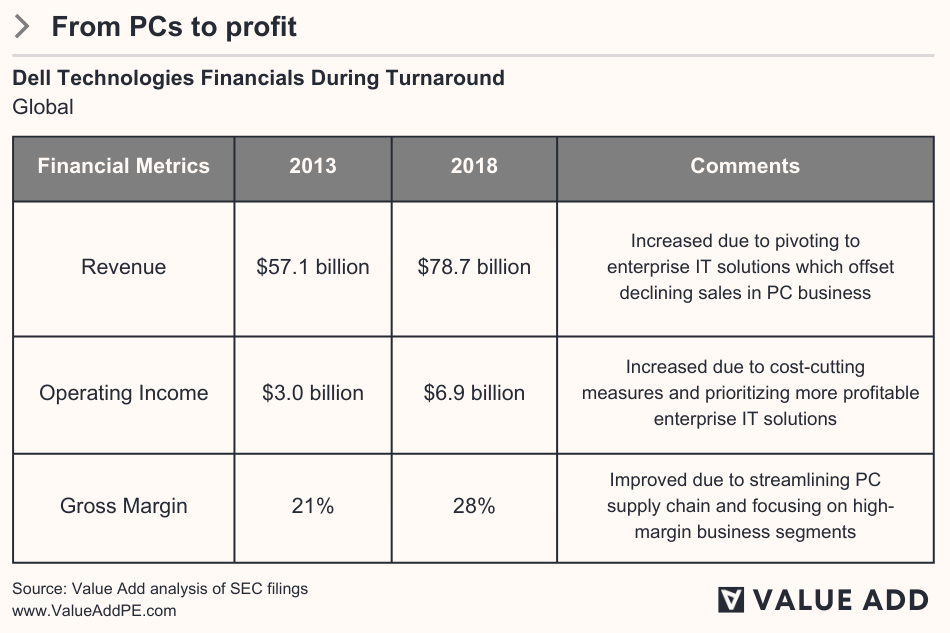

- Operational Improvements and Cost Efficiency. Dell began cutting costs associated with its PC business as early as 2012, with the goal of taking $2 billion of expenses out by 2015 and an additional $1 billion out in 2016. These measures ramped-up once the company was taken private. In 2014, more than 2,000 people (2% of Dell’s workforce) were laid off. Dell also streamlined the supply chain for manufacturing PCs by standardizing system configurations, moving operations to more affordable geographic areas, and making the supply chain more efficient. The company also sold-off several low-margin, non-core businesses in 2016, including NTT Data for $3 billion, as well as Quest Software and SonicWALL for a combined $2 billion. These efforts were part of a broader shift in Dell's business strategy to focus on higher-margin services, which helped the company improve gross margin from 21% in 2013 to 25% in 2018.

- Investment in Research and Development. Increasing investment in R&D was a key pillar of Dell’s revitalization as a private company. By increasing the budget allocated to R&D, Dell was able to innovate and develop new products and services, especially in emerging technology areas like cloud infrastructure and cybersecurity. This focus on innovation helped Dell stay ahead in a technology market where continuous evolution is the key to survival – a reality it learned all too well when it was late to diversify away from PCs in the early-2000s. Between 2013 and 2018, Dell increased R&D spending from $1.1 billion to $4.4 billion.

- Expansion through Strategic Acquisitions. Michael Dell and Silver Lake also guided Dell Technologies through a series of strategic acquisitions. These acquisitions were targeted to bolster Dell's presence in its new margin accretive business segments such as enterprise solutions, software, and services. For instance, the acquisition of EMC Corporation in 2016, a massive deal valued at approximately $67 billion, significantly enhanced Dell's capabilities in data storage and cloud computing, making it a powerhouse in the IT infrastructure domain.

To execute the value creation plan, Dell’s Board brought in a slew of new high-ranking executives. In 2014, Tom Sweet was promoted to company CFO and Priceline’s former-CIO Ron Rose was hired as SVP of online operations in 2013. The following year, AMD’s former-CEO Rory Read was named Dell’s COO, and former-Cisco VP Paul Perez was brought in to be CTO of Dell’s new enterprise group.

To continue reading this case study and for more private equity insights, subscribe to Value Add.

You guys should try to get a discount for WSO users

6 month free trial for any of our paying students... goal was to get our students access to some great content (+ value to our courses + programs) in exchange for a lot of exposure for them.

Does that include those who have bought PE course?

Commercial Due Diligence (Dell 2013 LBO)

Source:

Hyperlink:

Note - reformatted from original images/slides to fit better in the space provided. Hope this helps add to the OP's post on Dell above

Source: Dell (Project Denali) Presentation of The Boston Consulting Group to the Special Committee of the Company, dated December 5, 2012. Via SEC Filing: Dell - SC 13E3/A (Going private transaction) (3.29.2013); (EX-99.(C)(19).

Hyperlink: https://www.sec.gov/Archives/edgar/data/826083/000119312513134621/d5054…https://www.sec.gov/Archives/edgar/data/826083/000119312513134621/d505474dex99c19.htm

I don’t like computer so no

Dell is community computer at library

Necessitatibus ut sunt ex vel. Rerum suscipit atque eveniet dolor. Ut et ut est aliquam. Consectetur laborum vero molestiae vitae. Veniam id natus voluptatibus quaerat perspiciatis.

Enim eius accusamus nemo unde tempora est praesentium. Saepe doloribus repellendus dolores ipsum enim ipsum eos maxime.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...