Analyzing Aged Delinquencies in Multifamily

I've got a couple questions for the multifamily people out there:

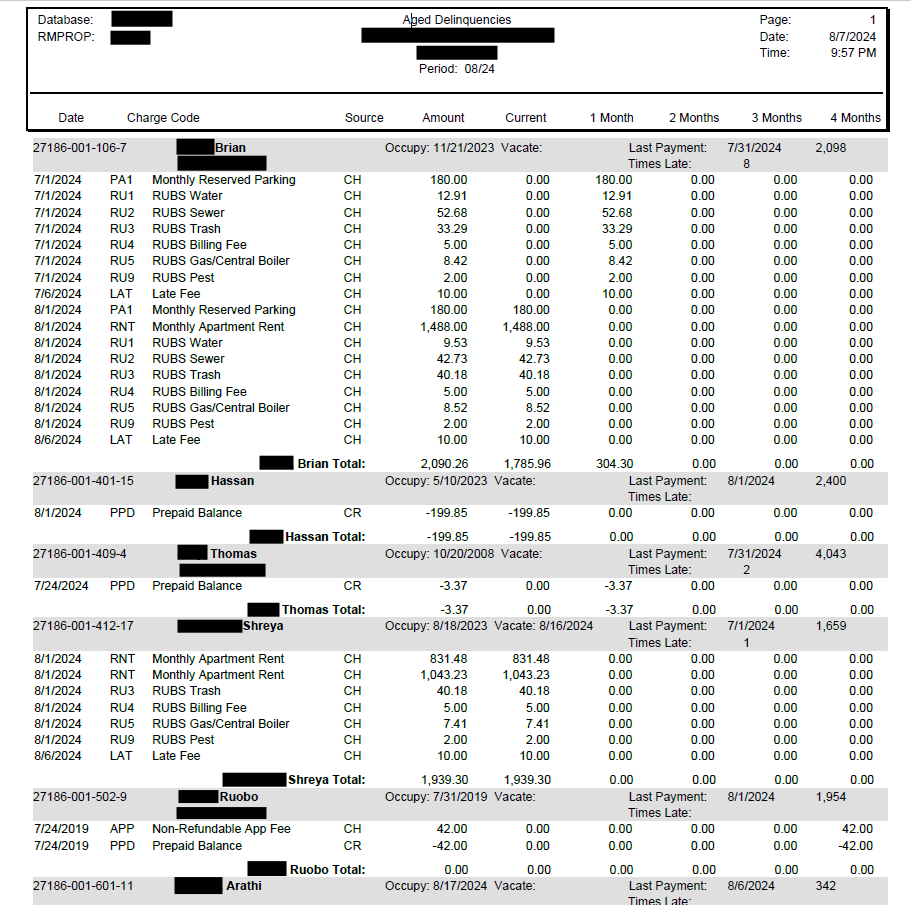

1) How do you read a delinquency report like the one below? There are columns labeled Amount, followed by Current, 1, 2, 3, & 4 Months. I'm assuming that any charge listed is an outstanding delinquency, and that Current = the charge is less that 30 days delinquent, 1 Month = 30-60 days, 2 Months = 61-90 days, etc. Is this correct? At the very bottom of my example, there is a $42 charge that nets out to $0. Is that tracked like that to show the history of tenants?

2) How do you tie this into your risk analysis? Obviously the more delinquency the higher the risk, but are there any ratios/rules of thumbs you can use to help classify the level of delinquency? (i.e. anything over 1.5% of tenants or as a percentage of rent income is a concerning.) I don't see a lot of MF so I'm not sure what is normal. My example is an early 2000's build, probably a B+ building, with an A+ location in the CBD, and most tenants are young professionals.

I've attached a screenshot of the report I'm trying to analyze. Redacted full names and property info for obvious reasons.

Thanks! I appreciate any help I can get.

1) That is correct. The importance of the current / 0-30 column is going to highly depend on the date of the report and the corresponding 31-60 balances. If the report is dated the 3rd of the month, it's pretty immaterial. Shit, I just had my automatic payment go out for September rent today on the 4th since a late fee isn't assessed until the 5th. Anyone greater than 1 month delinquent should raise concerns, and there are hopefully notes in the AR report tracking the onsite team's communication with the tenant. I'm not entirely sure what the netted out charge at the bottom is, but my guess is it's a new applicant that wrote a check for their app fee and the office hasn't cleared the check yet to eliminate the charge on their account.

2) There really is no one-size-fits-all approach to MF AR. Balances can be high because of shit management. They can also be high today if a property is located in a city that still has strong COVID protections for past balances or is still back logged with processing evictions (see this a lot still in the Seattle MSA). But yes, a high AR balance is a risk and does say something about the tenant profile of the general area. One thing I will note - if you see a property carrying a lot of AR, be sure to ask the owner if the report is including past tenant balances. I've seen some shady shit on that front.

Thank you! Can you clarify what do you mean by asking owners if their reports including past tenant balances? Don't all delinquency reports inherently only show past balances? (if they weren't past due, then they would not be delinquent)

Past in regards to tenancy. It's common for AR to be written off as bad debt on the P&L once a tenant w/ an outstanding balance moves out.

AR Reports will sometimes have a column specifying that the resident is a current occupant. I'm not suggesting you should look out for this on every deal you underwrite, but if there's a lot of noise in the AR and very little bad debt written off on the T12, it's just something to be aware of (since we're on this specific topic).

On this note, what does “prepays” mean? I have often seen that in a AR report and it is usually a negative number.

It's exactly how it sounds - prepaid rent showing up as a negative balance on their receivable account. Often shows up on end of month reports when people that pay by check drop off a few days early.

It’s someone who paid early for whatever that charge is. The report shows delinquency balances, so those are positive numbers even though we think of delinquency as a “bad” thing and positive numbers as a “good” thing. An example of a prepay is someone who overpaid rent by $200 on 9/1. If you receive an A/R on 9/28 showing a -$200 prepay, it’s a credit - they will only be billed for their full rent less $200 on 10/1. But in the meantime the credit has to be carried somewhere, and would ultimately reduce the total balance of rent due and thus is showed as a negative.

Depends where the asset is.

If it’s in a relatively tenant friendly city.. you can likely just kiss anything 30+ days goodbye.

Et non iusto corrupti quia distinctio rem. Doloremque necessitatibus ipsam est. Officia voluptatem tempora ab dolor quis.

Sed id dolore voluptatem enim voluptas. Nostrum voluptas distinctio quis et. Cum harum quia distinctio reprehenderit eos quia eum. Fugit laborum ut culpa asperiores nulla inventore sed.

Dolorem dolorem nostrum placeat sunt deserunt voluptas et. Velit aliquid ut fugiat eveniet eaque porro iste. Adipisci et velit tenetur omnis cumque ut quibusdam. Esse quo eius porro asperiores. Quos corrupti quis ex. Repudiandae occaecati sunt impedit maiores aliquid et. Ut et iste voluptatem vel ipsa culpa culpa.

Quia eaque at quas eveniet similique. Quas inventore temporibus ipsa est aliquam recusandae. Cum quia accusamus sunt voluptatibus. Eos doloremque dignissimos neque est asperiores earum itaque. Voluptas nostrum quam recusandae architecto sed. Voluptatem quis esse vero et sapiente molestiae dolorem. Qui laborum ut eveniet qui iusto aut nesciunt.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...