FX Earning/paying carry

How can you tell if someone is earning or paying carry just by looking at forward points. Don’t completely grab concept other than earning carry with higher yielding currency and vise versa. See some forward pts are negative ajd some are positive Random Examples Eur/usd Gbp/usd Usd/cad

What are you even asking?

Unlike the guy above, I know what you’re asking; the question makes sense.

Think about it like this: If forward points are negative (ie F S so F - S 0) then we can think about the lower forward level as a reflection of positive carry. Consider a trade where we enter a long forward (we will deliver CCY2 and get paid CCY1 in the future) and we choose to hedge spot movements by shorting spot as to receive the CCY2 that we will deliver in the future for our long forward. The advantage of buying in the future at a lower (strike) price than spot should be offset by the negative carry from short spot. Hence, long spot is positive carry.

Another way to think about it is that spot should theoretically drift down to the forward level because inflation in the country of CCY1 > inflation in country of CCY2 (which is why rCCY1 > rCCY2). If this convergence fully happens, carry profits offset the negative drift in spot. Empirically, this doesn’t happen, which is why carry strategies are profitable.

Yet another more mathy way to think about it: For a general CCY1CCY2 pair, F = S[1+(rCCY2 - rCCY1)t]. Thus, F S implies that rCCY1 > rCCY2. This means that when we buy the FX pair (ie we buy CCY1 by selling CCY2) we are borrowing at rCCY2 to sell that ccy and receive rCCY1. This is positive carry since rCCY1 > rCCY2 as stated above.

eg rEUR rUSD, so forward points F - S are positive. This reflects negative carry of EUR vs the USD.

ty for write-up - expected to know this level for S&T FX/rates SA?

If you want to get a good seat, yes imo. I didn’t end up in FX but knowing these things made me stand out in the FX vol desk which caught the attention of the USD rates group, where I ultimately ended. The more you know as an SA, the more optionality you’ll have in choosing a good desk. Of course, learning all this is also optional

Can I just clear some doubt with you that i have @WinSomeLoseMost.

Supposedly:

Spot AUDUSD is at 0.6484

1M AUDUSD is at 0.648657

this is a "positive forward point", this means that this is a negative carry?

can't i think of it as me buying AUD and selling USD at 0.6484

and selling AUD and buying back USD at 0.648657 1 month later.

which is this case i bought AUD cheaper than i am going to sell it for in 1month time. and thus it is a positive carry.

Or what i am referring to is a total different concept that focuses more on "Hedged Pick Up".

FX hedged pickup refers to bonds (can be either rolling or maturity matched). Have a read of "Random Walks in Fixed Income and Foreign Exchange" (pdf is on libgen) - it is a great explainer for the cross currency basis + FX hedged pickup

So what I have explained earlier isn't an FX Carry Trade, but rather a Hedged pick up yea..

Thank you, I am actually currently starting on that book, boy did it gave me nightmares.

(sidenote: have you read the book, were there any discrepancies you found in the book?

For example: it was mentioned that Xccybasis = rd-theoretical – rd-market, in the first part and

subsequently it stated that "Negative basis: the difference between the actual interest rate for a currency and

the theoretical interest rate calculated using the FX forward rate, FX spot rate

and (usually) the USD interest rate. When the actual rate is less than the theoretical

rate, the basis is negative."

Hi. You’re confusing the capital gain of the position with carry. You are correct that buying AUDUSD at current spot and selling it later at a higher strike would create a gain. This would happen if everything was held constant and spot slowly drifted up because rUSD > rAUD (since inflation in US expected to be higher, so USD will depreciate faster hence AUDUSD would go up).

However, think about what’s going on when you enter the spot transaction. You start with nothing and need to borrow USD at a higher rate, sell those to buy AUD, and lend those AUD at a lower rate. This is the carry component of the trade, which is negative.

If the upward drift mentioned above happens (remember the gap of F - S is proportional to the rate differential as shown in original post) then the negative carry is offset by that positive PnL you mentioned of buying low today, selling high later. But if rates remain constant and the FX rate doesn’t drift up to the current 1m forward level of 0.648657 then your capital gains are not enough to offset the negative carry.

Let me know if you have any more questions

First of all thank you for taking the time out to answer my questions, i do really appreciate it.

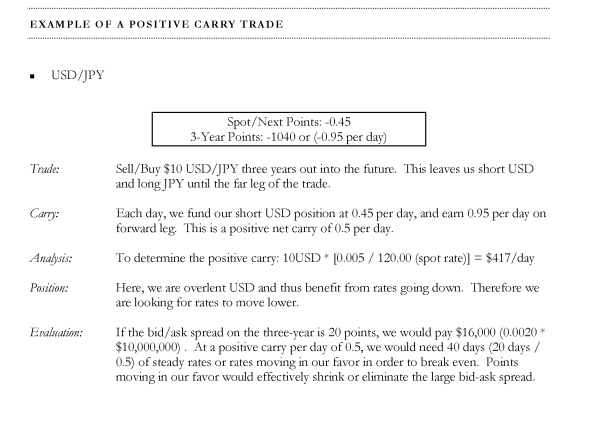

I have found this in one of the Lehman brother's manual, will this be a good representation of a FX carry trade?

in this particular example, the trade was to sell USD and Buy JPY @ spot and buy USD and Sell JPY 3 years later at a negative forward rate -1040. (Done using an FX SWAP).

in this trade we are long the lower interest rate currency which is the JPY and short USD which is the higher rate currency. But this is still considered a Carry trade?

FX guy here... i can help...

lets say EURUSD spot at 1.0500 right now...

"forward points" to 1 month is +15.00 (written mathematically as 0.0015), this means that if you want to enter into a forward contract to buy, or sell EURUSD, your rate will be 1.0500+0.0015.

Now, we see in this case, since the forward points are POSITIVE, that means that if you bought EURUSD in the future, that will be MORE expensive than buying it now. Similarly, if you SOLD EURUSD in the future, you would get a better price, than if you sold EURUSD now.

If this was the case, why would anyone want to ever sell EURUSD today?

The real answer is since US bonds/OIS/yields are yielding higher returns than EU fixed income assets, if USD holders just held US bonds for a month, and then sold their USD for EUR later... that would then always be a better decision.

So to prevent the above conditions, and as per no-arbitrage rules, you must be penalized if you wanted to hold USD and not EUR, and vice-versa, be compensated if you wanted to hold EUR and not USD.

A practical example of this is in swap markets, aka funding markets. if you wanted to hold USD for whatever needs, and had EUR funding, you would need to sell EURUSD in spot markets, and buy EURUSD in the future (lets say 1 month for our example). This means you sell EURUSD at 1.05 and buy EURUSD at 1.0515. You are paying 0.0015 effectively, (you have no fx spot risk btw), but the reaosn you are paying this is because once you hold USD, you theoretically receive a higher yield than if you held EUR (if you just bought bonds / or other FI assets).

hope that helps. its nmuch easier to think about it from a funding/carry perspective, dont get caught up by FX spot, theres no fx spot risk here.

Voluptas ut magnam ut et totam. In id occaecati cupiditate vel.

Inventore qui alias quam quibusdam. Odio ullam asperiores quis id. Voluptas quia tenetur facilis non in. Ut ab dicta velit eaque. Commodi rerum impedit est minus. Quod aut hic earum autem natus praesentium est odit.

Perferendis consequatur nihil impedit sapiente saepe quo et. Qui qui provident non. Numquam et vero omnis aut. Quisquam ipsam magni reprehenderit odit nesciunt. Rerum dolorum ad distinctio vero vel impedit consequatur. Et quae voluptas voluptas dolore.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...