Not a Downturn — A Transition: Vietnam’s Market Reset

Vietnam is growing at 8%.

Trade is approaching $930B.

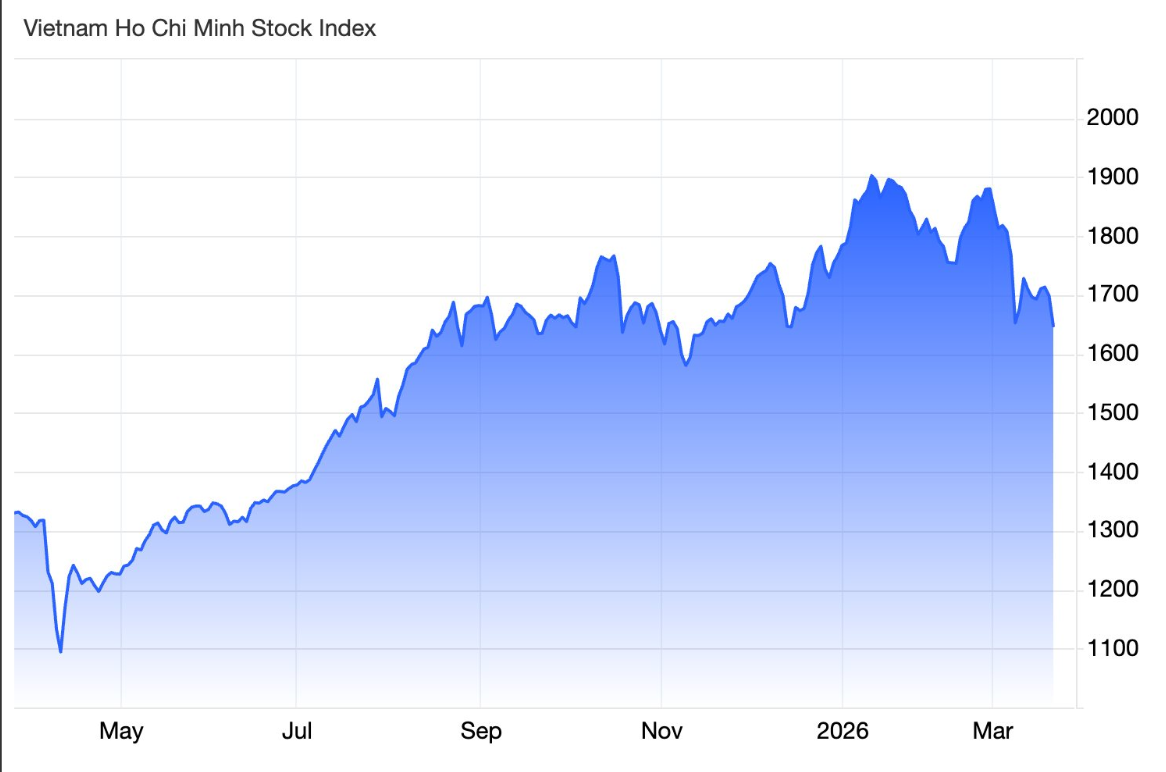

Yet, the VN-Index is pulling back — with no clear signal of a hard bottom in the short to medium term.

At first glance, this looks like a contradiction.

But in reality, it may be something more important: 𝐚 𝐭𝐫𝐚𝐧𝐬𝐢𝐭𝐢𝐨𝐧.

𝐅𝐨𝐫 𝐭𝐡𝐞 𝐩𝐚𝐬𝐭 𝐝𝐞𝐜𝐚𝐝𝐞, 𝐕𝐢𝐞𝐭𝐧𝐚𝐦’𝐬 𝐠𝐫𝐨𝐰𝐭𝐡 𝐡𝐚𝐬 𝐛𝐞𝐞𝐧 𝐥𝐚𝐫𝐠𝐞𝐥𝐲 𝐞𝐱𝐭𝐞𝐫𝐧𝐚𝐥𝐥𝐲 𝐝𝐫𝐢𝐯𝐞𝐧:

FDI-led manufacturing

Export expansion

Integration into global supply chains — particularly linked to China and Western demand

That model worked — and delivered remarkable numbers.

But it also created a structural dependency:

Vietnam grows fast when the world is stable.

And slows when the world becomes uncertain.

𝐓𝐨𝐝𝐚𝐲, 𝐭𝐡𝐞 𝐠𝐥𝐨𝐛𝐚𝐥 𝐛𝐚𝐜𝐤𝐝𝐫𝐨𝐩 𝐢𝐬 𝐟𝐚𝐫 𝐟𝐫𝐨𝐦 𝐬𝐭𝐚𝐛𝐥𝐞.

Geopolitical risks remain elevated

Supply chains are still being reconfigured

Capital flows are selective — and Emerging Markets are no longer the default destination

In that context, market corrections are not surprising.

They are necessary.

What we are seeing now may not be a downturn.

It may be a 𝐫𝐞𝐬𝐞𝐭 𝐭𝐨𝐰𝐚𝐫𝐝 𝐢𝐧𝐭𝐞𝐫𝐧𝐚𝐥 𝐬𝐭𝐫𝐞𝐧𝐠𝐭𝐡.

Vietnam is gradually shifting:

from export reliance → domestic consumption

from FDI dominance → stronger local participation

from rapid expansion → more sustainable, quality-driven growth

This is not a negative signal.

It is the foundation of a more resilient economy.

𝐅𝐨𝐫 𝐢𝐧𝐬𝐭𝐢𝐭𝐮𝐭𝐢𝐨𝐧𝐚𝐥 𝐜𝐚𝐩𝐢𝐭𝐚𝐥, 𝐭𝐡𝐢𝐬 𝐩𝐡𝐚𝐬𝐞 𝐦𝐚𝐭𝐭𝐞𝐫𝐬.

Markets rarely bottom when the narrative is strong.

They bottom when expectations are reset —

and when uncertainty forces discipline.

That is when long-term positions begin to form.

Vietnam may not offer immediate clarity.

The market may remain volatile.

But beneath that noise, a different story is taking shape:

Not just growth —

but the ability to 𝐜𝐨𝐦𝐩𝐨𝐮𝐧𝐝 𝐟𝐫𝐨𝐦 𝐰𝐢𝐭𝐡𝐢𝐧.

And that is a story long-term capital cannot ignore.

Et quibusdam omnis officia tempore libero quas. Aut eum porro quis assumenda et dolorum deleniti unde. Aliquid nobis quo aut.

Aut dolor nihil dolor incidunt perferendis. Incidunt nisi eligendi adipisci aperiam consequatur. Enim vero in dolorem et ipsum exercitationem nam maxime. Ea nisi iusto rem rem eos fuga. Impedit tempore rem aut nulla. Tempora ex voluptas nesciunt eos non vitae.

Architecto totam nobis vero est aliquid repudiandae. Quia iste ab impedit voluptas eveniet animi nemo.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...